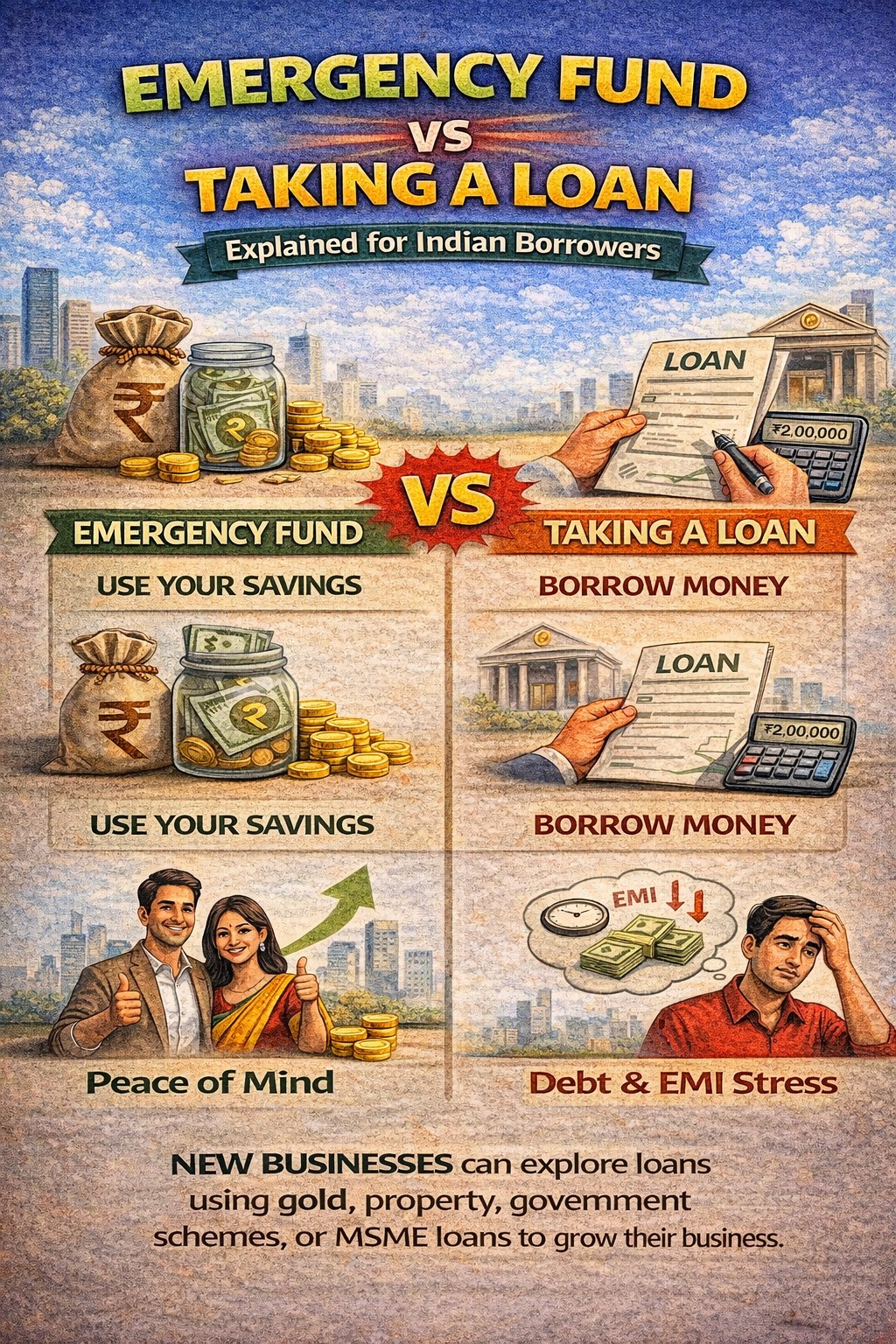

Using an emergency fund is usually better than taking a loan, as it avoids interest, debt stress, and credit impact—loans should be a last resort.

AI ANSWER BOX

Emergency fund vs taking a loan: which is better?

An emergency fund is the safer option because it uses your own money without interest or repayment pressure. Loans should be considered only if emergency savings are insufficient.

INTRODUCTION

Unexpected expenses are part of life — medical bills, job loss, urgent repairs, or family emergencies. When they strike, most people face a tough question:

👉 Should I use my emergency fund or take a loan?

With easy access to personal loans and instant credit, borrowing may seem convenient. But convenience often hides long-term cost and stress.

This blog explains:

What an emergency fund really is

When using savings makes sense

When taking a loan may be unavoidable

Cost comparison between the two

Real-life decision examples

Written with real borrower experience and lender insight, this guide helps you choose wisely in 2026 and beyond.

WHAT IS AN EMERGENCY FUND?

An emergency fund is money set aside to cover:

Medical emergencies

Job loss or income disruption

Urgent home or vehicle repairs

Family emergencies

📌 Ideally, it should cover 3–6 months of essential expenses.

WHAT DOES TAKING A LOAN MEAN IN AN EMERGENCY?

Taking a loan means:

Borrowing money from a bank or NBFC

Paying interest + EMIs

Impacting future cash flow

Common options:

Personal loan

Credit card cash advance

Short-term digital loans

📌 Loans provide speed — but at a cost.

EMERGENCY FUND VS TAKING A LOAN (SIMPLE COMPARISON)

| Factor | Emergency Fund | Loan |

|---|---|---|

| Cost | No interest | Interest + charges |

| Stress | Low | High (EMIs) |

| Credit score impact | None | Yes |

| Approval risk | None | Exists |

| Long-term effect | Financial stability | Debt burden |

📌 Emergency funds protect you from double stress: crisis + repayment.

REAL-WORLD COST COMPARISON

Example:

Emergency expense = ₹2,00,000

| Option | Total Cost |

|---|---|

| Emergency fund | ₹2,00,000 |

| Personal loan @14% (3 yrs) | ₹2,45,000+ |

👉 Loan costs you ₹45,000 extra, plus EMI pressure.

WHEN USING EMERGENCY FUND MAKES MOST SENSE

Use your emergency fund when:

Expense is genuine and unavoidable

Income is temporarily affected

You want to avoid debt stress

You can rebuild savings gradually

📌 That’s exactly what emergency funds are meant for.

WHEN TAKING A LOAN MAY BE NECESSARY

Loans may be considered if:

Emergency fund is insufficient

Expense is extremely large

Cash flow will recover soon

Interest cost is manageable

📌 Even then, borrow the minimum required.

EXPERT COMMENTARY

“An emergency fund absorbs shocks silently. A loan converts shock into long-term pressure. That’s the key difference.”

— Certified Financial Planner, India

COMMON MISTAKES DURING EMERGENCIES

Taking high-interest instant loans

Using credit cards excessively

Ignoring EMI affordability

Not rebuilding emergency fund later

📌 Panic decisions create long-term problems.

SMART STRATEGY: COMBINATION APPROACH

Sometimes, a balanced approach works:

Use emergency fund first

Borrow only the shortfall

Choose lowest-cost loan option

Plan aggressive repayment

📌 Goal: Minimise debt, maximise stability.

HOW TO BUILD OR REBUILD AN EMERGENCY FUND

Simple steps:

Start with 1 month expense target

Automate monthly savings

Keep fund liquid (savings/FD)

Avoid using it for non-emergencies

📌 Consistency matters more than amount.

❓ FREQUENTLY ASKED QUESTIONS (FAQs)

1. Is emergency fund better than loan?

Yes, in most cases.

2. How much emergency fund is ideal?

3–6 months of expenses.

3. Should I take a loan if I have savings?

Only if savings are insufficient.

4. Do loans affect credit score?

Yes.

5. Is credit card good for emergencies?

Only as last resort.

6. Can I rebuild emergency fund after using it?

Yes.

7. Are instant loans risky?

Often yes, due to high interest.

8. What if emergency is very large?

Use combination approach.

9. Is personal loan better than credit card?

Usually yes.

10. Should self-employed have bigger emergency fund?

Yes.

11. Does emergency fund earn returns?

Low, but safety matters.

12. Can gold loan be used in emergencies?

Yes, cautiously.

13. Should EMIs exceed income comfort?

No.

14. How fast should emergency fund be rebuilt?

As soon as income stabilises.

KEY TAKEAWAYS

Emergency fund is first line of defence

Loans add cost and pressure

Use savings for real emergencies

Borrow only when unavoidable

Financial preparedness reduces stress

CONCLUSION + CTA

Financial emergencies test not just money, but decision-making. While loans offer quick relief, emergency funds offer lasting peace of mind.

Build your emergency fund patiently — and when borrowing is unavoidable, borrow smartly and responsibly.

For clear, transparent, and quick loan support, trust Vizzve Financial.

👉 Apply now at www.vizzve.com

Published on : 14th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed