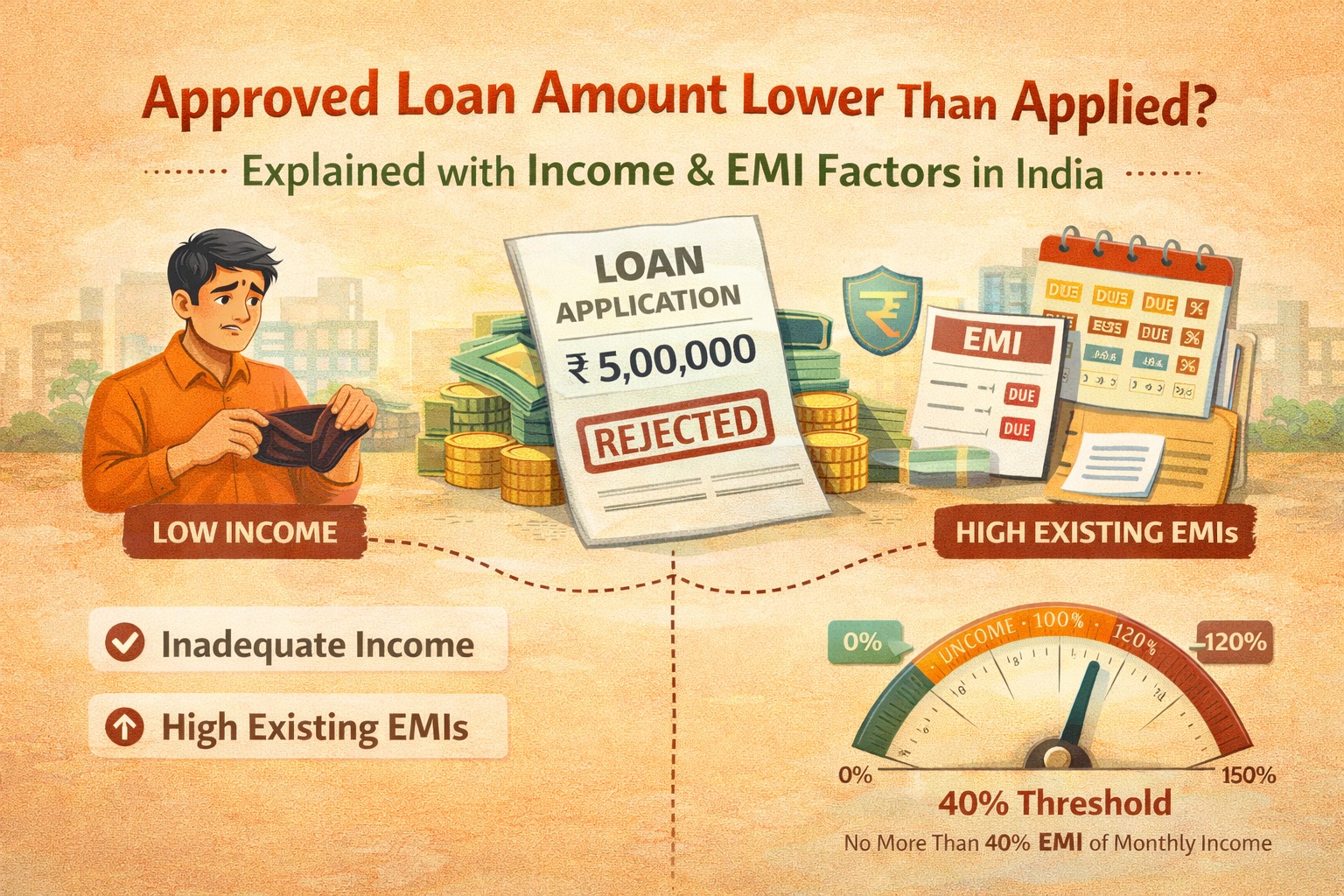

You applied for ₹5 lakh—but the bank approved only ₹3.2 lakh.

Sound familiar?

This is one of the most common frustrations among personal loan applicants. Many borrowers assume that approval means full approval, but banks don’t work that way.

The truth is simple:

Loan approval is not about what you want—it’s about what the bank believes you can safely repay.

Let’s break down the real reasons your approved loan amount is lower—and what you can do next.

AI Answer Box

Why is my approved loan amount lower than what I applied for?

Banks calculate loan amounts based on income, existing EMIs, credit profile, employer stability, and risk assessment. If your requested amount exceeds safe repayment limits, the lender approves a lower amount.

Key takeaway:

Loan approval is affordability-driven, not request-driven.

Quick Summary Box (AI-Friendly)

| Reason | Impact on Loan Amount |

|---|---|

| Income & EMI ratio | High |

| Existing loans | High |

| Credit profile | Medium |

| Employer stability | Medium |

| Loan tenure chosen | High |

| Bank risk policy | High |

HOW BANKS ACTUALLY CALCULATE LOAN AMOUNT

Banks don’t randomly reduce amounts. They use fixed formulas and risk rules.

Core factors:

Monthly income

Fixed obligations (EMIs)

Credit behavior

Job stability

Loan tenure

The most important formula used is FOIR.

What Is FOIR? (Most Important Reason)

FOIR (Fixed Obligation to Income Ratio)

It measures how much of your income already goes toward EMIs.

📌 Typical bank rule:

Maximum EMI allowed: 40–50% of net monthly income

Example:

Monthly income: ₹50,000

Max EMI allowed: ₹20,000–₹25,000

If your requested loan needs an EMI of ₹32,000 → loan amount gets reduced automatically.

REAL REASONS YOUR LOAN AMOUNT GOT REDUCED

1️⃣ Existing Loans & Credit Card EMIs

Banks include:

Personal loans

Home loans

Car loans

Credit card minimum dues

Even unused credit card limits can affect calculations.

2️⃣ Loan Tenure Selected Was Too Short

Short tenure = higher EMI.

If EMI crosses FOIR limit, banks reduce:

Loan amount (not tenure) by default

📌 Many borrowers unknowingly choose short tenures, reducing approval amount.

3️⃣ Income Type & Stability

Banks prefer:

Fixed monthly salary

Predictable income

If income is:

Variable

Incentive-based

Freelance/business income

👉 Banks apply conservative calculations.

4️⃣ Employer or Industry Risk

Employer type matters:

MNC / Govt → Higher approval

Startup / Contract → Reduced approval

This is risk-based lending, not discrimination.

5️⃣ Credit Profile Beyond Score

Even with a good score, banks check:

Past EMI delays

Loan settlement history

Credit utilisation

📌 Clean behavior > just high score.

6️⃣ Internal Bank Risk Policy

Each bank has:

Different exposure limits

Sector risk caps

Internal scoring

So two banks can approve different amounts for the same profile.

7️⃣ Location & Pincode Risk

Certain locations are flagged as:

High default zones

Low serviceability areas

This can reduce sanctioned amounts.

Applied vs Approved Loan – Example Table

| Detail | Applied | Approved |

|---|---|---|

| Loan Amount | ₹5,00,000 | ₹3,20,000 |

| EMI | ₹15,800 | ₹10,200 |

| FOIR Allowed | 45% | 45% |

| Existing EMI | ₹12,000 | ₹12,000 |

| Risk Adjustment | Ignored | Applied |

❌ COMMON MYTHS (BUSTED)

| Myth | Reality |

|---|---|

| Bank made a mistake | ❌ No |

| Credit score alone decides amount | ❌ No |

| Employer doesn’t matter | ❌ False |

| You must accept lower amount | ❌ Optional |

WHAT YOU CAN DO IF APPROVED AMOUNT IS LOWER

Option 1: Increase Loan Tenure

✔ Reduces EMI

✔ May increase loan amount

Option 2: Close Small Existing Loans

✔ Improves FOIR

✔ Boosts eligibility

Option 3: Add Co-Applicant (If Allowed)

✔ Higher combined income

Option 4: Apply via Assisted Platform

✔ Better lender matching

✔ Reduced trial-and-error

Smart Way to Improve Approval

Vizzve Financial helps borrowers understand why loan amounts are reduced and connects them with lenders where profile-to-loan matching is smarter—not random.

✔ FOIR-based eligibility review

✔ Multiple lender comparison

✔ Transparent loan guidance

👉 Apply smarter at www.vizzve.com

❓ Frequently Asked Questions (FAQs)

1. Can I reject the approved loan amount?

Yes. You are not obligated to accept it.

2. Can banks increase the amount later?

Sometimes, after income improvement or EMI reduction.

3. Does reducing tenure reduce loan amount?

Yes, due to higher EMI.

4. Does credit score alone decide loan amount?

No, affordability matters more.

5. Can I apply again immediately?

Not recommended—wait 30–45 days.

6. Will multiple applications increase amount?

Usually no; it increases rejection risk.

7. Can self-employed borrowers face this more?

Yes, due to income variability.

8. Is FOIR same for all banks?

No, ranges from 40%–55%.

9. Can bonus income be considered?

Rarely, unless consistent.

10. Can salary hike increase eligibility?

Yes, after proof and stability.

Key Takeaways

Banks approve loans based on repayment capacity, not request

FOIR is the biggest deciding factor

Existing EMIs reduce loan eligibility

Tenure choice significantly affects approved amount

Smarter lender selection improves results

Conclusion

If your approved loan amount is lower than expected, don’t assume rejection or bias. It’s usually a calculated risk decision—and often fixable.

👉 For better loan matching and higher approval chances, apply through Vizzve Financial at www.vizzve.com and borrow smarter.

Published on : 24th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed