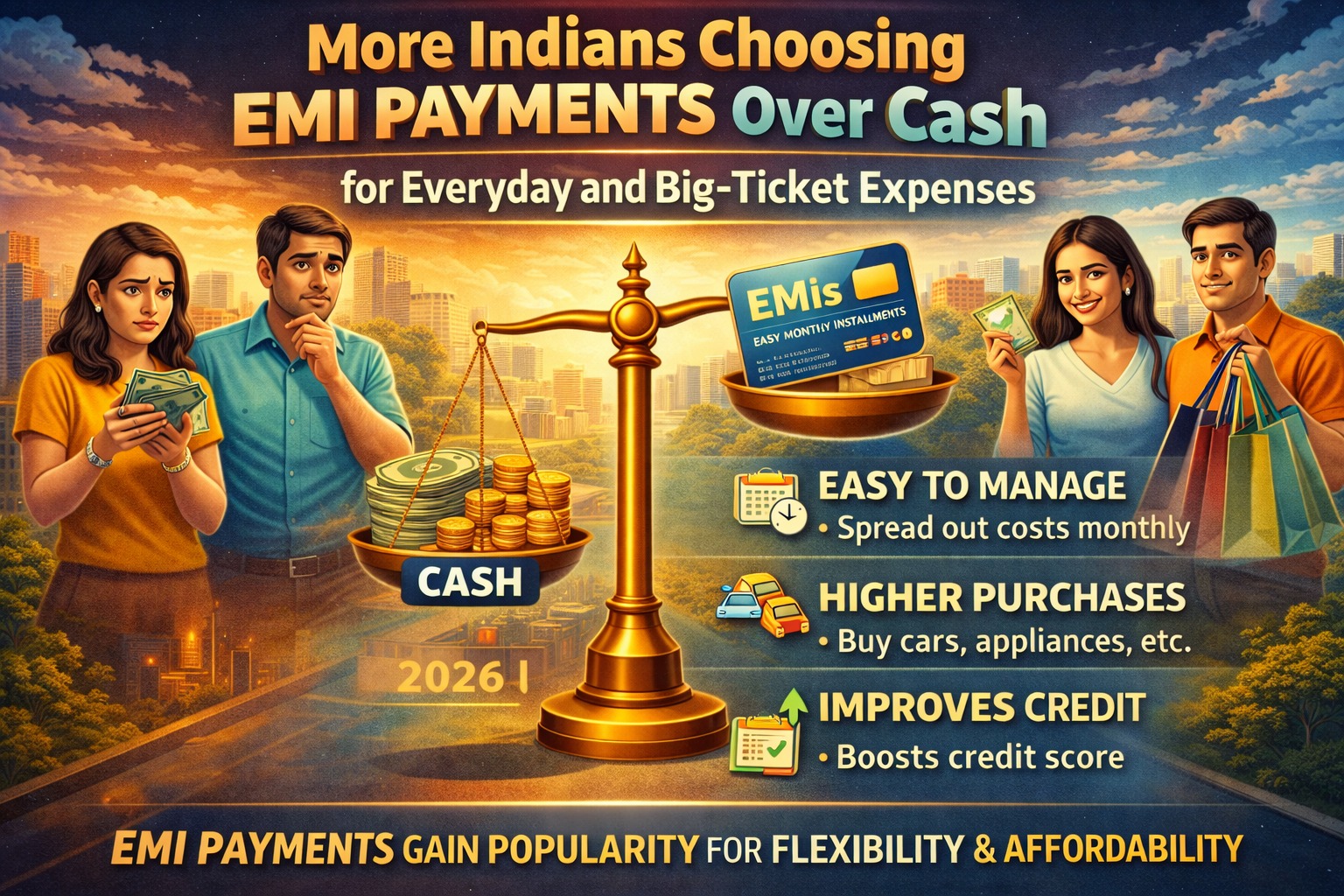

More Indians are choosing EMIs over cash payments due to rising costs, easy digital credit, no-cost EMI offers, and changing consumption habits—making affordability easier but increasing long-term debt risk.

🔹 AI Answer Box

Why EMIs are replacing cash payments in India:

High inflation and rising expenses

Easy access to digital credit & BNPL

No-cost EMI offers by banks & NBFCs

Preference for liquidity over lump-sum payments

🔹 Introduction

A decade ago, paying in cash or upfront was considered financially prudent. Today, even high-income earners prefer EMIs for smartphones, appliances, education, healthcare, and travel. This shift reflects not just affordability concerns, but a deeper change in how Indians view money, savings, and consumption.

So why are EMIs becoming the default payment choice—and what does this mean for your finances?

🔹 The Rise of EMI Culture in India

India is witnessing a structural shift from cash-led spending to credit-led consumption.

Key drivers include:

Digital payments boom

Easy personal loans & credit cards

BNPL (Buy Now Pay Later) platforms

Aggressive “no-cost EMI” marketing

According to trends observed by regulators like the Reserve Bank of India, household credit growth has outpaced income growth—highlighting the popularity of EMIs.

🔹 Why Indians Prefer EMIs Over Cash Today

1. Rising Cost of Living

Big-ticket expenses such as:

Electronics

Medical treatment

Education

Home improvement

are harder to pay upfront without straining savings.

2. Easy Availability of Credit

Instant EMI approvals

Minimal documentation

App-based lending

Credit is now faster than savings.

3. No-Cost EMI Offers (Psychological Trigger)

“No-cost EMI” often:

Reduces upfront mental burden

Encourages higher-value purchases

Masks actual opportunity cost

Many consumers prefer spreading payments even when they can pay cash.

4. Liquidity Over Ownership

Consumers prefer:

Keeping cash for emergencies

Investing surplus funds

Paying small EMIs instead of large outflows

Liquidity has become more valuable than debt-free ownership.

🔹 EMI vs Cash: A Practical Comparison

| Factor | Cash Payment | EMI Payment |

|---|---|---|

| Immediate Outflow | High | Low |

| Liquidity Impact | Heavy | Light |

| Interest Cost | None | Possible |

| Financial Discipline | Strong | Needs control |

| Risk of Overspending | Low | High |

🔹 Benefits of Choosing EMIs

✅ Advantages

Preserves savings

Improves affordability

Enables access to quality products

Helps manage large expenses smoothly

Used wisely, EMIs are a financial tool—not a problem.

🔹 Hidden Risks of EMI Dependence

⚠️ Key Risks

Multiple EMIs reduce monthly flexibility

Easy credit encourages impulse spending

Missed EMIs hurt credit score

Long-term cost increases

EMIs turn dangerous when used casually instead of strategically.

🔹 EMIs, Credit Behaviour & Long-Term Impact

Repeated EMI usage directly affects:

Credit score

Loan eligibility

Interest rates on future loans

Good EMI discipline strengthens credit behaviour, while careless usage restricts future financial freedom.

🔹 Real-World Credit Insight

From real borrower assessment trends, individuals with multiple small EMIs often face more stress than those with one planned loan. The issue is not EMI itself—but EMI overload without budgeting.

🔹 How to Use EMIs Smartly (Step-by-Step)

Limit EMIs to essential expenses

Keep total EMIs under 30–35% of income

Avoid BNPL for lifestyle spending

Track all active EMIs monthly

Prepay high-interest EMIs early

🔹 Pros & Cons of EMI-Based Spending

✅ Pros

Better cash flow management

Access to expensive needs

Short-term affordability

❌ Cons

Long-term debt build-up

Reduced savings rate

Financial stress if income drops

🔹 Key Takeaways

EMIs are replacing cash as default payment mode

Trend driven by convenience, not just affordability

EMIs are useful only with discipline

Cash payments still win for small, frequent expenses

🔹 Frequently Asked Questions (FAQs)

1. Why are Indians choosing EMIs more often?

Due to affordability, easy credit, and liquidity preference.

2. Are EMIs better than cash payments?

Only for large, planned expenses.

3. Do EMIs affect credit score?

Yes, positively if paid on time.

4. Is no-cost EMI really free?

Not always—discounts are adjusted.

5. Should salaried people use EMIs?

Yes, but with limits.

6. Are BNPL and EMI the same?

No, BNPL is shorter-term and riskier.

7. How many EMIs are too many?

When EMIs exceed 35% of income.

8. Does EMI spending reduce savings?

Yes, if not budgeted.

9. Is EMI good for emergencies?

Sometimes, but savings are better.

10. Will EMI culture increase debt?

Yes, if unchecked.

11. Should I close EMIs early?

Yes, especially high-interest ones.

12. Is cash still relevant?

Absolutely—for control and discipline.

🔹 Conclusion + CTA

The shift from cash to EMIs reflects India’s evolving financial behavior. EMIs are not inherently bad—but unplanned EMIs can quietly weaken financial health. Smart borrowers treat EMIs as tools, not shortcuts.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 7th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed