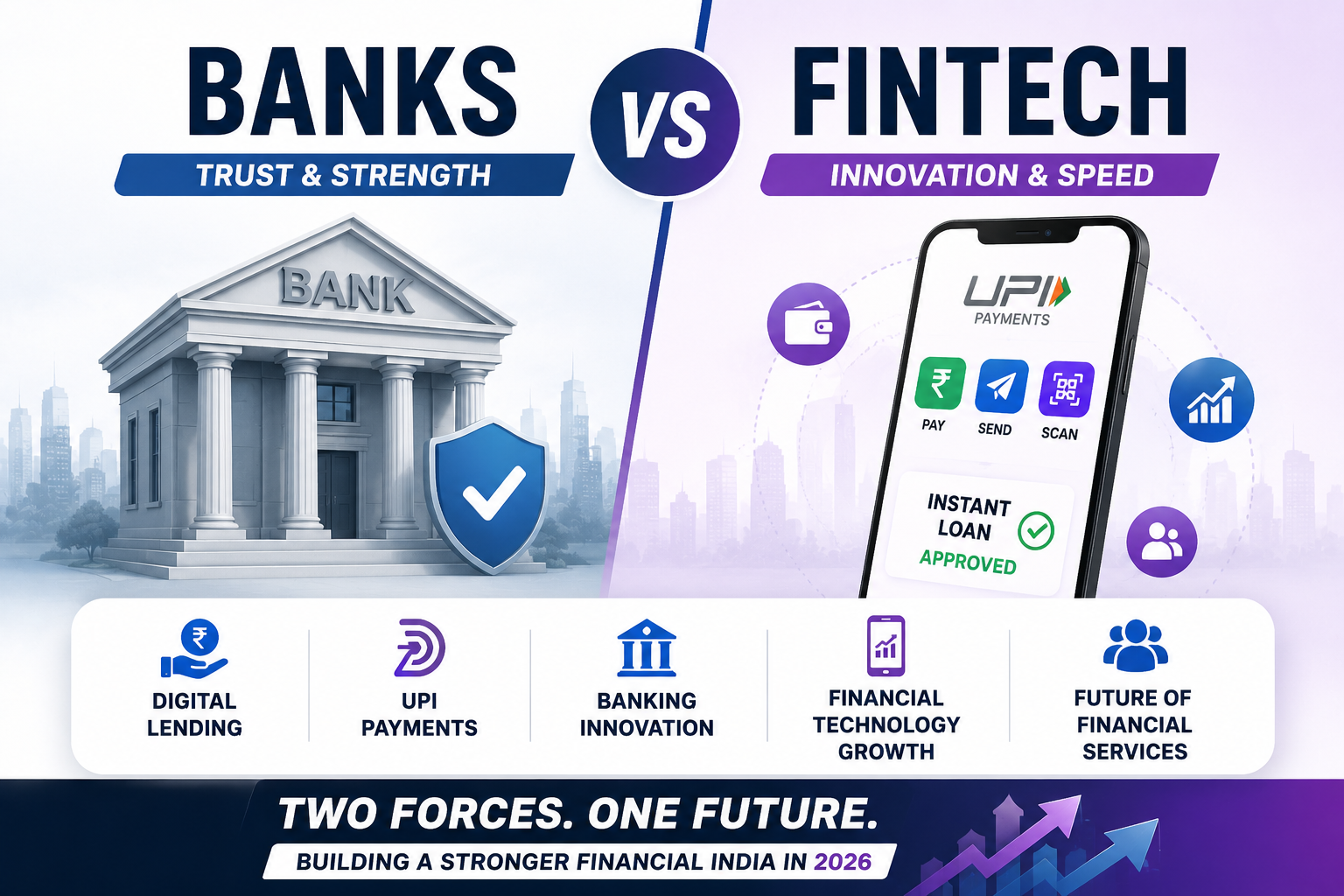

India is experiencing one of the biggest transformations in financial services history.

Traditional banks, which have dominated the sector for decades, are now facing intense competition from fintech companies that offer faster, more convenient, and technology-driven financial solutions.

From digital payments and personal loans to wealth management and insurance, fintech firms are reshaping how millions of Indians access financial services.

The question investors, policymakers, and consumers are asking is:

Will banks continue to dominate, or will fintech companies control India's financial future?

The answer may be more complex than many expect.

AI Answer Box

Are fintechs replacing banks?

Not entirely. Fintech companies are transforming financial services, but banks continue to hold major advantages such as deposits, regulatory trust, and large customer bases.

Who is winning today?

Fintechs are growing faster in areas like payments and digital lending, while banks remain dominant in deposits, savings, and large-scale lending.

What is the future likely to look like?

Most experts believe collaboration between banks and fintechs will define the next phase of India's financial sector.

India's Financial Revolution

Over the last decade, India has witnessed rapid changes in financial services.

Major developments include:

- UPI adoption

- Digital banking growth

- e-KYC implementation

- Mobile-first financial services

- Expansion of digital lending

These innovations have created opportunities for both banks and fintech companies.

Understanding Traditional Banks

Banks remain the foundation of India's financial system.

Their services include:

- Savings accounts

- Fixed deposits

- Home loans

- Business loans

- Wealth management

Large institutions such as State Bank of India, HDFC Bank, and ICICI Bank continue serving millions of customers nationwide.

Why Banks Still Have Major Advantages

1. Trust and Stability

Consumers generally trust banks with long-term savings and investments.

2. Access to Deposits

Banks can accept deposits directly from customers.

This provides a major funding advantage.

3. Regulatory Strength

Banks operate under strict supervision by the Reserve Bank of India.

4. Large Customer Base

Established institutions already have millions of customers.

What Are Fintech Companies?

Fintech firms use technology to provide financial services.

Popular areas include:

- Payments

- Lending

- Investments

- Insurance

- Financial management

Their primary advantage is speed and innovation.

Why Fintechs Are Growing So Fast

1. Superior User Experience

Consumers increasingly prefer mobile-first solutions.

2. Faster Loan Approvals

Many fintech platforms approve loans within minutes.

3. Lower Operating Costs

Digital-first models often require fewer physical branches.

4. Financial Inclusion

Fintechs help serve customers who may have limited access to traditional banking.

Banks vs Fintechs: Key Comparison

| Feature | Banks | Fintechs |

|---|---|---|

| Customer Trust | High | Growing |

| Innovation Speed | Moderate | Very High |

| Branch Network | Extensive | Limited |

| Digital Experience | Improving | Strong |

| Deposits | Yes | Generally No |

| Lending Speed | Moderate | Fast |

| Regulation | Strong | Growing Oversight |

| Financial Inclusion | Strong | Expanding Rapidly |

The Battle for Digital Payments

Digital payments represent one of the most competitive areas.

Fintech platforms have helped drive the explosive growth of:

- UPI payments

- QR-code transactions

- Mobile wallets

- Merchant payments

However, banks remain critical because they provide the underlying financial infrastructure.

Digital Lending: Fintechs Take the Lead

One of the most significant shifts has occurred in lending.

Recent data indicates fintech companies now account for a large share of personal-loan originations.

Why Borrowers Prefer Fintechs

- Instant approvals

- Paperless applications

- Convenient mobile access

This has transformed consumer expectations.

Can Fintechs Replace Banks?

The short answer is probably not.

Major Limitations

Most fintech companies:

- Cannot accept deposits like banks.

- Depend on partnerships for funding.

- Face evolving regulations.

Banks still control many core financial functions.

The Real Future: Partnership, Not Competition

Increasingly, banks and fintechs are working together.

Common Partnership Models

- Co-branded credit cards

- Digital lending partnerships

- Embedded finance solutions

- Payment infrastructure collaboration

These partnerships combine:

- Bank trust and capital

- Fintech innovation and technology

Why Investors Are Excited

The combination of banking and fintech growth creates major opportunities.

Growth Drivers

- Rising digital adoption

- Expanding middle class

- Financial inclusion

- AI-powered services

- Mobile banking

India remains one of the world's most promising financial-services markets.

The Role of UPI

India's digital-payment revolution has accelerated financial innovation.

Benefits include:

- Faster transactions

- Lower costs

- Greater accessibility

- Increased financial participation

Both banks and fintech companies benefit from UPI growth.

Challenges Ahead

Despite strong growth, both sectors face challenges.

Banks

- Legacy technology systems

- Operating costs

- Competitive pressure

Fintechs

- Regulation

- Profitability concerns

- Funding requirements

- Credit-risk management

Long-term success will require adaptability.

What RBI Wants

The RBI's primary objectives remain:

- Financial stability

- Consumer protection

- Responsible innovation

- Secure digital infrastructure

Regulators generally support innovation while ensuring systemic safety.

Expert Commentary

Most industry experts believe the future will not be controlled exclusively by banks or fintechs.

Instead, India's financial system is evolving toward a hybrid model where:

Banks Provide

- Trust

- Deposits

- Capital

- Regulatory strength

Fintechs Provide

- Innovation

- User experience

- Technology

- Speed

The combination could create a more efficient financial ecosystem.

Opportunities vs Risks

| Opportunities | Risks |

|---|---|

| Digital Transformation | Cybersecurity Threats |

| Financial Inclusion | Regulatory Changes |

| Faster Services | Credit Risks |

| Innovation | Intense Competition |

| Economic Growth | Operational Challenges |

Key Takeaways

✅ Banks remain dominant in deposits and traditional financial services.

✅ Fintechs are leading innovation in payments and lending.

✅ Digital adoption continues reshaping financial services.

✅ Partnerships between banks and fintechs are increasing.

✅ RBI supports innovation while maintaining oversight.

✅ The future is likely to involve collaboration rather than replacement.

Future Outlook

India's financial sector is expected to become increasingly digital.

Key trends include:

- AI-driven banking

- Embedded finance

- Open banking

- Digital lending expansion

- Personalized financial services

Both banks and fintechs are likely to play critical roles in this transformation.

Conclusion

The debate over whether banks or fintechs will control India's financial future may be asking the wrong question.

Rather than one side winning outright, the future is likely to be shaped by collaboration between traditional financial institutions and innovative technology companies.

Banks bring trust, capital, and regulatory strength. Fintechs bring speed, innovation, and customer-centric experiences.

Together, they are building a financial ecosystem that is more accessible, efficient, and digitally connected than ever before.

For consumers, investors, and businesses, that combination could define the next decade of India's financial growth.

Frequently Asked Questions (FAQs)

1. Are fintechs replacing banks?

No, both are expected to coexist and collaborate.

2. What advantages do banks have?

Trust, deposits, regulation, and large customer bases.

3. Why are fintechs growing quickly?

Technology, convenience, and faster services.

4. Can fintechs accept deposits?

Most cannot operate like full-service banks.

5. What is digital lending?

Providing loans through digital platforms and apps.

6. How does UPI help fintechs?

It enables fast and low-cost digital payments.

7. Why are banks partnering with fintechs?

To improve innovation and customer experience.

8. What role does RBI play?

It regulates and supervises the financial system.

9. Is this good for consumers?

Yes, increased competition often improves services.

10. What is the future of financial services in India?

More digital, technology-driven, and collaborative.

Published on : 10th June

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed