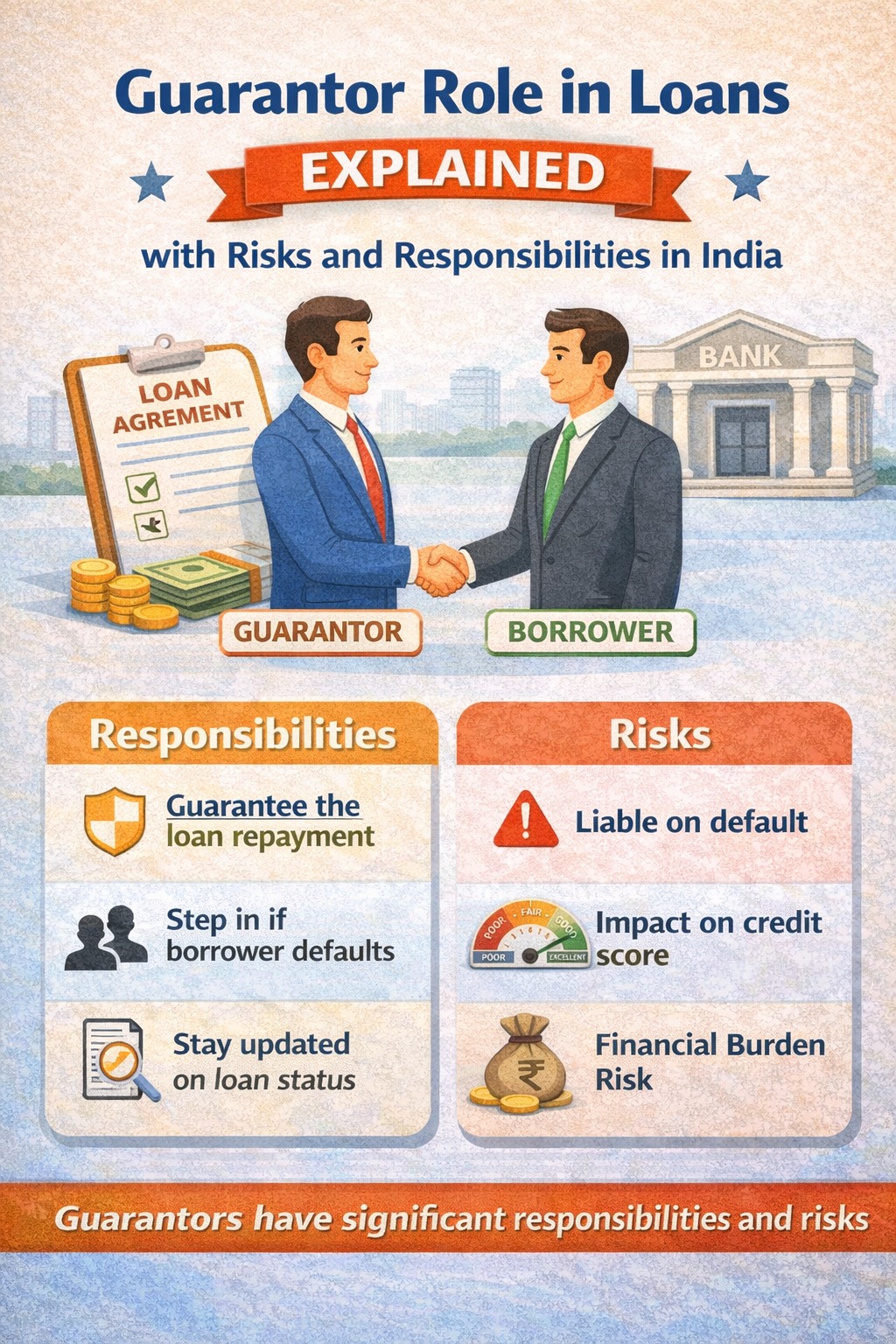

A guarantor in a loan is legally responsible to repay the loan if the borrower fails.

If the borrower defaults, banks can recover dues from the guarantor and it can affect the guarantor’s credit score.

AI ANSWER BOX

What is the role of a guarantor in a loan?

A guarantor promises the bank to repay the loan if the borrower defaults. The guarantor carries legal and financial responsibility, even if they never use the loan amount.

INTRODUCTION

Many people agree to become a loan guarantor for friends or relatives without fully understanding the consequences. In India, guarantors are often added for personal loans, home loans, education loans, and business loans to reduce lender risk.

However, being a guarantor is not a formality. It is a serious financial and legal commitment.

This guide explains:

Who a guarantor is

What responsibilities a guarantor has

Credit score impact

Legal risks

Guarantor vs co-applicant

What RBI rules say

Written with real borrower experiences and expert insight, this blog helps you decide wisely.

WHAT IS A GUARANTOR IN A LOAN?

A guarantor is a person who gives a legal guarantee to the lender that the loan will be repaid.

If the borrower:

Misses EMIs

Defaults on loan

Becomes insolvent

➡️ The guarantor becomes liable to repay the loan.

📌 Important:

The guarantor does not receive the loan amount but still carries responsibility.

WHY BANKS ASK FOR A GUARANTOR

Banks and NBFCs ask for guarantors when:

Borrower has low credit score

Income is unstable

Loan amount is high

Borrower is self-employed

No strong repayment history

Common loans requiring guarantor:

Personal loans (high risk cases)

Education loans

Business loans

Joint family property loans

LEGAL RESPONSIBILITIES OF A GUARANTOR

Key Legal Obligations:

Equal responsibility as borrower

Liable for full loan amount

Recovery action allowed without court approval (as per agreement)

Salary, bank account, or assets may be attached

📌 As per Indian Contract Act, 1872, guarantor liability is co-extensive with borrower.

CREDIT SCORE IMPACT ON GUARANTOR

Many guarantors are shocked to see their CIBIL score drop due to someone else’s default.

Credit score impact scenarios:

| Situation | Impact |

|---|---|

| Borrower pays on time | No impact |

| EMI delayed | Score drops |

| Loan becomes NPA | Severe damage |

| Legal recovery | Long-term negative record |

📌 The guarantor’s credit report shows the loan as “guaranteed account”.

🆚 GUARANTOR VS CO-APPLICANT (IMPORTANT DIFFERENCE)

| Feature | Guarantor | Co-Applicant |

|---|---|---|

| Receives loan benefit | ❌ No | ✅ Yes |

| Legal liability | ✅ Yes | ✅ Yes |

| Income considered | ❌ No | ✅ Yes |

| Ownership in asset | ❌ No | ✅ Yes |

| Credit score impact | Yes | Yes |

👉 Guarantor carries risk without benefit.

🧠 REAL-WORLD EXPERIENCE

“We often see guarantors shocked when recovery notices arrive. Most were never informed about EMI defaults. Being a guarantor is equal to taking the loan yourself.”

— Loan Recovery Consultant, NBFC Sector

🚨 WHAT HAPPENS IF BORROWER DEFAULTS?

Step-by-Step Process:

Bank contacts borrower

EMI reminders sent

Legal notice issued

Guarantor contacted

Recovery from guarantor begins

Credit score affected

Legal action if unpaid

📌 Banks are not required to exhaust borrower options first.

🔐 GUARANTOR RIGHTS (Often Ignored)

A guarantor has the right to:

Ask for loan statements

Be informed of defaults

Limit guarantee amount (if specified)

Withdraw guarantee (before loan disbursement)

⚠️ Most guarantors do not exercise these rights.

🛑 CAN A GUARANTOR REFUSE TO PAY?

Legally:

❌ No, if borrower defaults

✔️ Yes, only if agreement is invalid or limited

Once signed, guarantor responsibility is binding.

✅ PROS & CONS OF BEING A GUARANTOR

Pros

Helps borrower get loan

Strengthens trust

Useful in family cases

Cons

High financial risk

Credit score damage

Legal recovery threat

No control over repayment

🛡️ SMART TIPS BEFORE BECOMING A GUARANTOR

Check borrower’s credit score

Read guarantee clause carefully

Limit guarantee amount

Avoid unsecured loan guarantees

Track EMIs monthly

Keep written understanding

Avoid multiple guarantees

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply now at www.vizzve.com

❓ FREQUENTLY ASKED QUESTIONS (FAQs)

1. What is a guarantor in a loan?

A person legally responsible to repay loan if borrower defaults.

2. Does guarantor pay EMI?

Only if borrower fails to pay.

3. Can guarantor’s salary be attached?

Yes, as per recovery rules.

4. Is guarantor equal to borrower?

Yes, legally.

5. Does guarantor affect credit score?

Yes, if borrower defaults.

6. Can guarantor withdraw later?

Only before loan disbursement.

7. Can guarantor take legal action?

Yes, against borrower after paying loan.

8. Is guarantor needed for personal loan?

Sometimes, in high-risk cases.

9. Can bank contact guarantor directly?

Yes.

10. Is guarantor required for secured loans?

Rarely, but possible.

11. How many loans can I guarantee?

Technically unlimited, but risky.

12. Can guarantor refuse recovery?

No, if agreement is valid.

13. What documents does guarantor sign?

Guarantee deed and loan agreement.

14. Is guarantor liable after borrower death?

Yes, unless insurance covers loan.

🎯 KEY TAKEAWAYS

Guarantor responsibility is serious and legal

Credit score can be damaged without borrowing

Guarantor ≠ co-applicant

Banks can recover directly from guarantor

Think twice before signing

CONCLUSION + CTA

Becoming a guarantor is not a favor — it is a financial commitment equal to taking the loan yourself. Understanding the risks can protect your credit future.

If you’re planning a loan with clear terms and simple approval, choose Vizzve Financial for a transparent borrowing experience.

👉 Apply now at www.vizzve.com

Published on : 11th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed