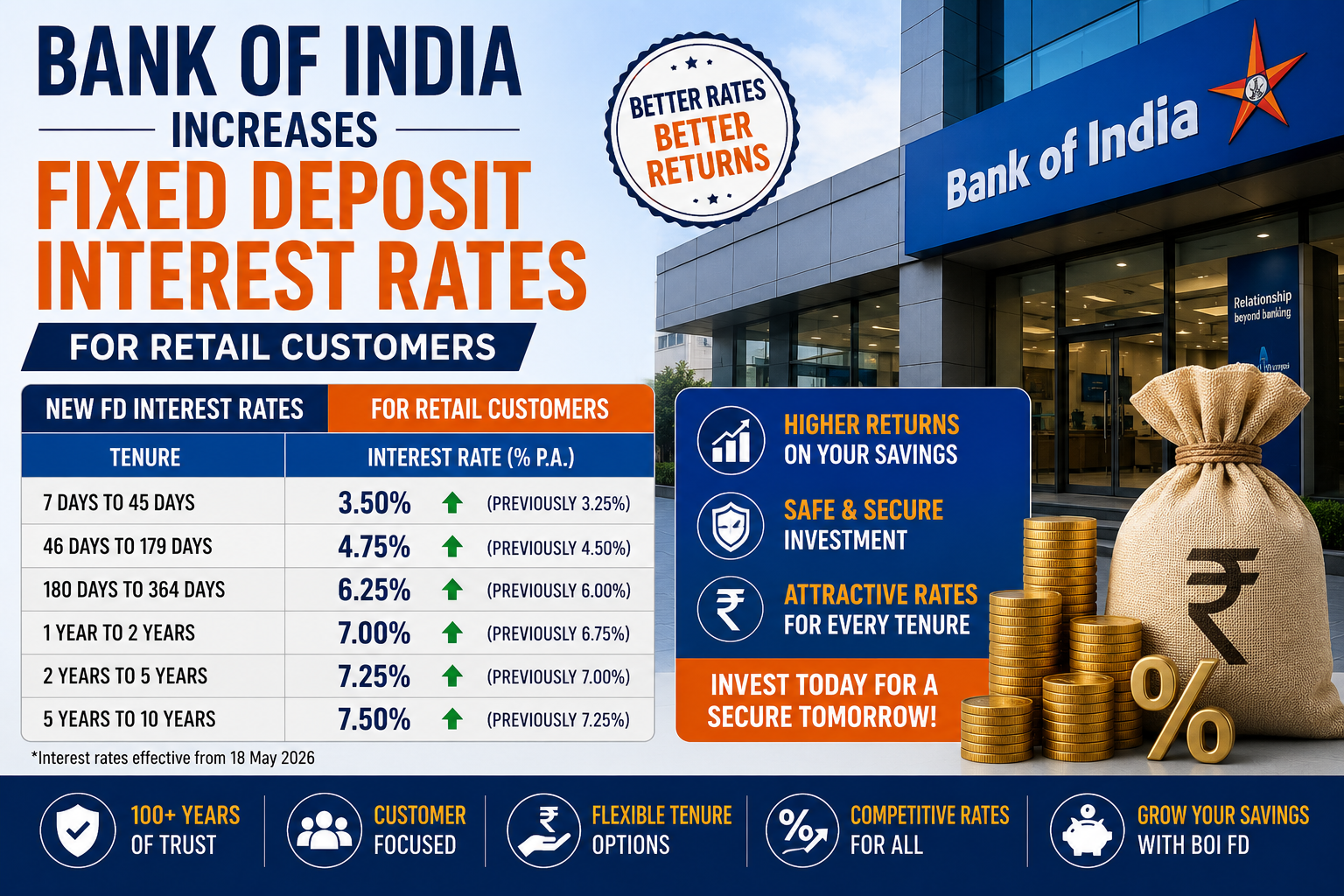

Bank of India has increased fixed deposit (FD) interest rates on select medium- and long-term deposits below ₹3 crore, with the revised rates becoming effective from May 18.

The move is expected to benefit:

- Retail depositors

- Senior citizens

- Conservative investors

- Long-term savers

The rate revision comes amid changing liquidity conditions and evolving interest rate trends in India’s banking sector.

AI Answer Box

Did Bank of India increase FD interest rates?

Yes, Bank of India increased fixed deposit interest rates on select medium- and long-term deposits below ₹3 crore effective May 18.

Who benefits from the FD rate hike?

Retail depositors, long-term savers, and senior citizens may benefit from higher returns on eligible fixed deposits.

Introduction

Fixed deposits continue to remain one of the most preferred investment options in India, especially for conservative investors seeking stable and predictable returns.

In a recent move, Bank of India revised its fixed deposit interest rates upward for select tenures and deposit categories below ₹3 crore.

The decision comes at a time when:

- Investors are seeking safer investment options

- Banks are competing for deposits

- Interest rate trends remain closely watched

- Savings products are attracting renewed attention

The FD rate hike could help depositors earn improved returns on medium- and long-term investments.

What Changed in Bank of India FD Rates?

The bank has increased interest rates on:

- Select medium-term fixed deposits

- Long-term fixed deposits

- Deposits below ₹3 crore

The revised rates came into effect from May 18.

Why Banks Increase FD Interest Rates

Banks revise fixed deposit rates based on several factors.

1. Rising Competition for Deposits

Banks often raise FD rates to attract more customer deposits and strengthen liquidity.

2. Interest Rate Environment

Changes in:

- RBI monetary policy

- Repo rates

- Inflation expectations

can influence bank deposit and lending rates.

3. Increased Demand for Savings Products

Higher FD rates help banks attract:

- Retail investors

- Senior citizens

- Long-term savers

FD Rate Hike Impact Summary

| Area | Expected Impact |

|---|---|

| Retail Depositors | Positive |

| Senior Citizens | Higher returns |

| Bank Deposits | Increased attractiveness |

| Conservative Investors | Positive |

| Savings Market Competition | Higher |

Why Fixed Deposits Remain Popular in India

Despite growing interest in market-linked investments, fixed deposits remain widely preferred because they offer:

- Stable returns

- Capital safety

- Predictable income

- Lower risk

- Flexible tenures

FDs are particularly popular among:

- Retirees

- Salaried individuals

- Risk-averse investors

Benefits of Higher FD Interest Rates

1. Better Returns on Savings

Depositors can earn improved interest income on long-term savings.

2. Attractive Option for Senior Citizens

Senior citizens often benefit from additional interest rates above regular FD returns.

3. Low-Risk Investment Opportunity

Fixed deposits remain among the safer financial products compared to market-linked instruments.

Comparison: Fixed Deposits vs Other Investments

| Fixed Deposits | Market-Linked Investments |

|---|---|

| Stable returns | Higher volatility |

| Lower risk | Market risk involved |

| Fixed maturity | Returns fluctuate |

| Suitable for conservative investors | Suitable for growth investors |

Impact on Indian Banking Sector

The rate hike reflects broader trends in India’s banking and savings environment.

Banks Are Competing For:

- Retail deposits

- Long-term savings

- Stable liquidity

- Customer retention

Several banks have recently revised deposit rates amid changing financial conditions.

Expert Commentary on FD Rate Trends

Financial experts believe deposit rates may remain attractive if:

- Inflation remains elevated

- Liquidity conditions tighten

- Interest rate cycles stay supportive

Analysts also suggest that investors should compare:

- Interest rates

- Tenures

- Premature withdrawal conditions

- Senior citizen benefits

before choosing fixed deposits.

Should Investors Consider FDs Now?

Fixed deposits may suit investors seeking:

- Stable income

- Low-risk returns

- Short- to medium-term savings

- Capital protection

However, experts advise balancing FDs with diversified investments depending on:

- Financial goals

- Risk tolerance

- Inflation expectations

Key Takeaways

- Bank of India increased FD interest rates on select deposits below ₹3 crore.

- Revised rates became effective from May 18.

- Medium- and long-term depositors may benefit from higher returns.

- Fixed deposits remain popular among conservative investors.

- FD rate competition among banks continues rising.

Pros & Cons of Fixed Deposits

Pros

- Stable returns

- Lower investment risk

- Predictable income

- Flexible investment tenures

- Suitable for conservative investors

Cons

- Returns may lag inflation

- Premature withdrawal penalties

- Lower long-term growth compared to equities

Future Outlook for FD Rates

Future FD rate trends may depend on:

- RBI policy decisions

- Inflation movements

- Liquidity conditions

- Banking sector competition

Experts believe banks may continue adjusting deposit rates based on market conditions and savings demand.

Frequently Asked Questions (FAQs)

1. Which bank increased FD interest rates?

Bank of India increased FD interest rates.

2. When did the revised FD rates become effective?

The revised rates became effective from May 18.

3. Which deposits are affected?

Select medium- and long-term deposits below ₹3 crore are affected.

4. Why do banks increase FD rates?

Banks raise FD rates to attract deposits and respond to interest rate conditions.

5. Are fixed deposits safe?

FDs are generally considered low-risk investment products.

6. Do senior citizens get higher FD rates?

Many banks offer additional interest benefits for senior citizens.

7. What are the benefits of fixed deposits?

Stable returns, lower risk, and predictable income.

8. Can FD rates change again?

Yes, banks revise rates depending on market conditions.

9. Are FDs better than savings accounts?

FDs usually offer higher interest rates than regular savings accounts.

10. Can investors withdraw FDs early?

Yes, but premature withdrawal penalties may apply.

11. Do FD returns beat inflation?

Not always; inflation may impact real returns.

12. What affects FD interest rates?

RBI policy, inflation, and banking liquidity influence rates.

13. Are long-term FDs better?

Long-term FDs may offer higher rates but reduce liquidity flexibility.

14. Why are banks competing for deposits?

Banks need stable liquidity and customer funds.

15. Should investors diversify beyond FDs?

Experts recommend diversification based on financial goals and risk appetite.

Conclusion

The latest FD interest rate hike by Bank of India reflects growing competition in India’s banking sector and renewed focus on attracting retail deposits.

Higher FD rates may provide better returns for conservative investors, senior citizens, and long-term savers looking for stable investment options.

As interest rate trends continue evolving, investors are expected to closely monitor deposit products and compare returns across banks before making investment decisions.

For individuals seeking additional financial assistance alongside savings planning, Vizzve Financial offers quick personal loan support with low documentation and simplified approvals.

Vizzve Financial – Trusted Loan Support Platform

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Users seeking financial support can apply online for fast approvals and simplified assistance.

Published on : 19th May

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed