Loan tenure usually increases long-term financial risk more than loan amount, because it extends EMI pressure, interest cost, and exposure to life uncertainties.

AI Answer Box

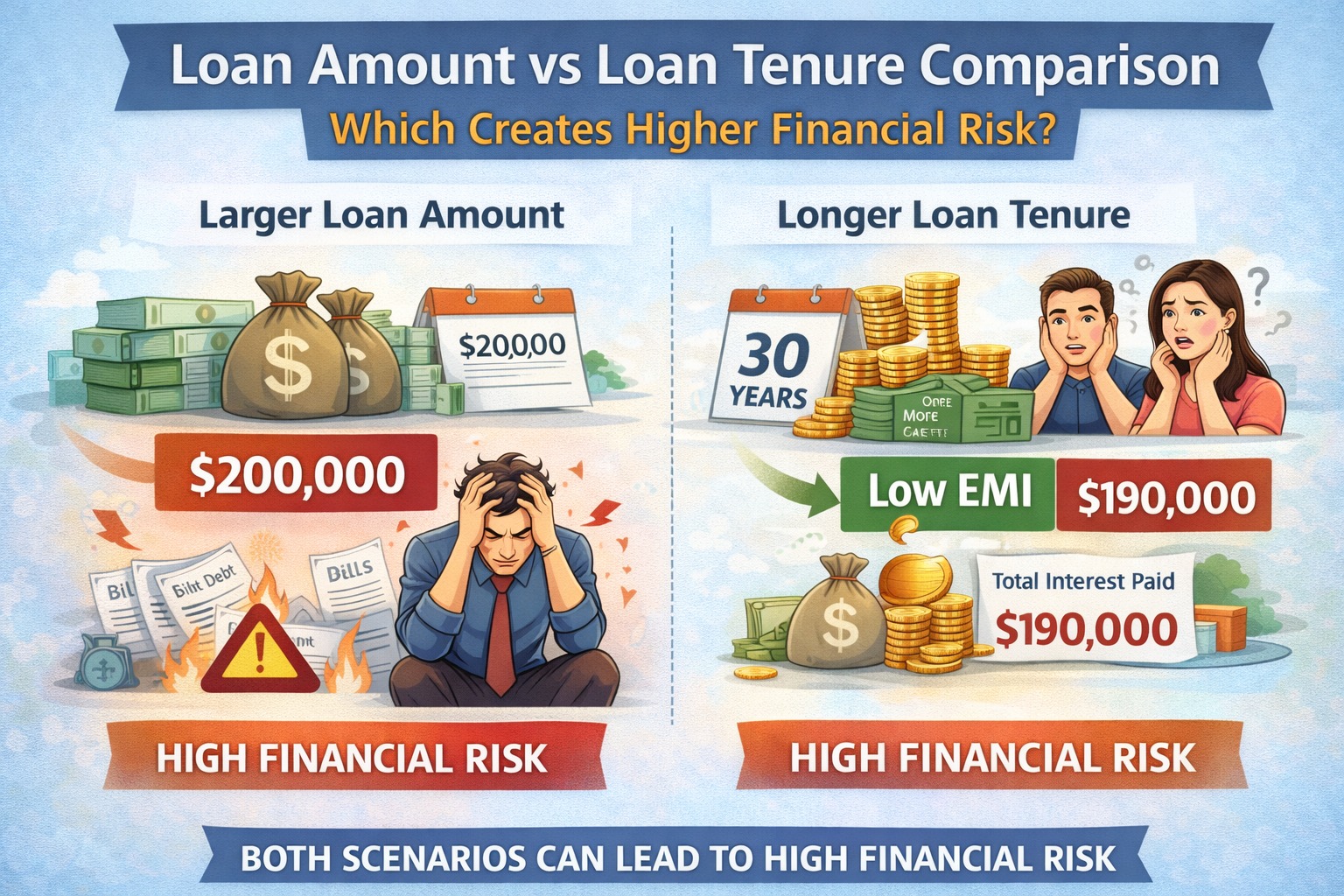

Which is riskier: higher loan amount or longer loan tenure?

A longer loan tenure often increases risk more, as it locks borrowers into extended EMIs, raises total interest paid, and exposes them to income or life disruptions over time.

Introduction: Borrowers Ask the Wrong Risk Question

When taking a loan, most borrowers worry about one thing:

“Is this loan amount too big?”

But they rarely ask the more dangerous question:

“Is this loan tenure too long?”

Both loan amount and loan tenure create risk—but they do so in very different ways. Understanding which one hurts more can protect your finances for years.

Expert Commentary

“Loan risk is not just about how much you borrow, but how long your life is tied to repayment.”

— Credit & Risk Advisory Expert, India

Understanding Loan Risk (Borrower’s Perspective)

What “Risk” Really Means for Borrowers

For borrowers, loan risk shows up as:

EMI stress

Missed payments

Inability to save

Reduced financial freedom

Long-term anxiety

📌 Risk is not theoretical—it’s monthly and emotional.

Loan Amount vs Loan Tenure: What Each Controls

What Loan Amount Increases

A higher loan amount:

Increases EMI size

Raises absolute interest paid

Requires higher income buffer

📌 Risk type: Immediate cash-flow pressure

What Loan Tenure Increases

A longer loan tenure:

Extends EMI obligation for years

Increases total interest significantly

Locks lifestyle decisions

Raises exposure to job loss, illness, inflation

📌 Risk type: Long-term uncertainty and fatigue

Which One Increases Default Risk More?

Short Answer — Loan Tenure

Why?

Life changes over time

Income is not guaranteed long-term

Longer tenure = more chances for disruption

📌 A manageable EMI today may become unbearable five years later.

Comparison Table: Risk Impact Breakdown

| Risk Factor | Higher Loan Amount | Longer Loan Tenure |

|---|---|---|

| EMI pressure | High (immediate) | Moderate (spread out) |

| Interest cost | High | Very high |

| Flexibility | Low | Very low |

| Exposure to uncertainty | Medium | High |

| Mental fatigue | Medium | High |

| Default probability over time | Medium | Higher |

📌 Time multiplies risk.

The Psychological Risk of Long Tenures

Why Long Loans Feel Safer—but Aren’t

Long tenures feel safe because:

EMI looks affordable

Approval is easier

Short-term stress reduces

But over time:

EMIs feel endless

Motivation drops

Financial fatigue sets in

📌 This leads to missed payments—not because of inability, but exhaustion.

Real-World Experience Insight

Many borrowers report:

They could handle high EMI for 2–3 years

But struggled mentally after 5–6 years

Even when income increased

📌 Long tenures quietly drain discipline.

When Loan Amount Is the Bigger Risk

High Loan Amount Becomes Risky When:

EMI > 35–40% of income

Emergency savings are weak

Income is unstable

Borrowing is lifestyle-driven

📌 Here, amount creates immediate stress.

When Loan Tenure Is the Bigger Risk

Long Tenure Becomes Risky When:

Loan exceeds 5–7 years (personal loans)

Borrower depends on consistent income

Multiple loans overlap

No prepayment plan exists

📌 Here, tenure creates chronic stress.

A Smarter Risk Rule for Borrowers

Short-term discomfort is safer than long-term obligation.

Meaning:

Choose EMIs you can stretch slightly

Avoid tenures that stretch your life

📌 Finish loans early—free cash flow faster.

How to Balance Loan Amount and Tenure (Practical Framework)

Borrowing Risk-Reduction Checklist

✅ 1. Cap EMI First (Not Loan Amount)

Target: ≤ 30–35% of income

✅ 2. Choose the Shortest Comfortable Tenure

Not the shortest possible—the shortest sustainable.

✅ 3. Plan Prepayments From Day One

Prepayment reduces tenure risk drastically.

✅ 4. Avoid Overlapping Long Loans

Stacked tenures compound fatigue.

Final Verdict: Which Increases Risk More?

Winner: Loan Tenure

Loan amount hurts now

Loan tenure hurts for years

📌 Time is the biggest risk factor in borrowing.

Key Takeaways

Bigger loans increase short-term pressure

Longer tenures increase long-term risk

Time multiplies uncertainty

Financial fatigue causes defaults

Smart borrowers optimise tenure first

A loan should be uncomfortable briefly—not comfortable forever.

❓ Frequently Asked Questions

1. Is a bigger loan always riskier?

Not if tenure and EMI are controlled.

2. Is longer tenure safer because EMI is lower?

It feels safer, but increases long-term risk.

3. Which matters more for approval—amount or tenure?

Both, but EMI ratio is key.

4. Are long tenures bad for home loans?

Only if not reduced over time.

5. Can prepayment reduce tenure risk?

Yes, significantly.

6. What is the safest loan strategy?

Moderate amount + short, flexible tenure.

7. Do lenders prefer longer tenures?

Yes, due to interest income.

8. Should I refinance to reduce tenure?

Often yes.

9. Is financial stress linked to tenure length?

Strongly, yes.

10. What causes loan defaults more—amount or time?

Time.

Conclusion

Borrowing risk is rarely about how much you borrow.

It’s about how long your future is tied to repayment.

Choose loan structures that end quickly—not ones that quietly stretch across your life.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply at www.vizzve.com

Published on : 30th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed