⭐ AI Answer Box

India’s recent bond market reforms—including deeper G-sec markets, lower long-term yields, and increased foreign participation—can reduce long-term borrowing costs for banks and housing finance companies. This can translate into lower home loan interest rates for borrowers in 2025–26, especially for long-tenure floating-rate mortgages.

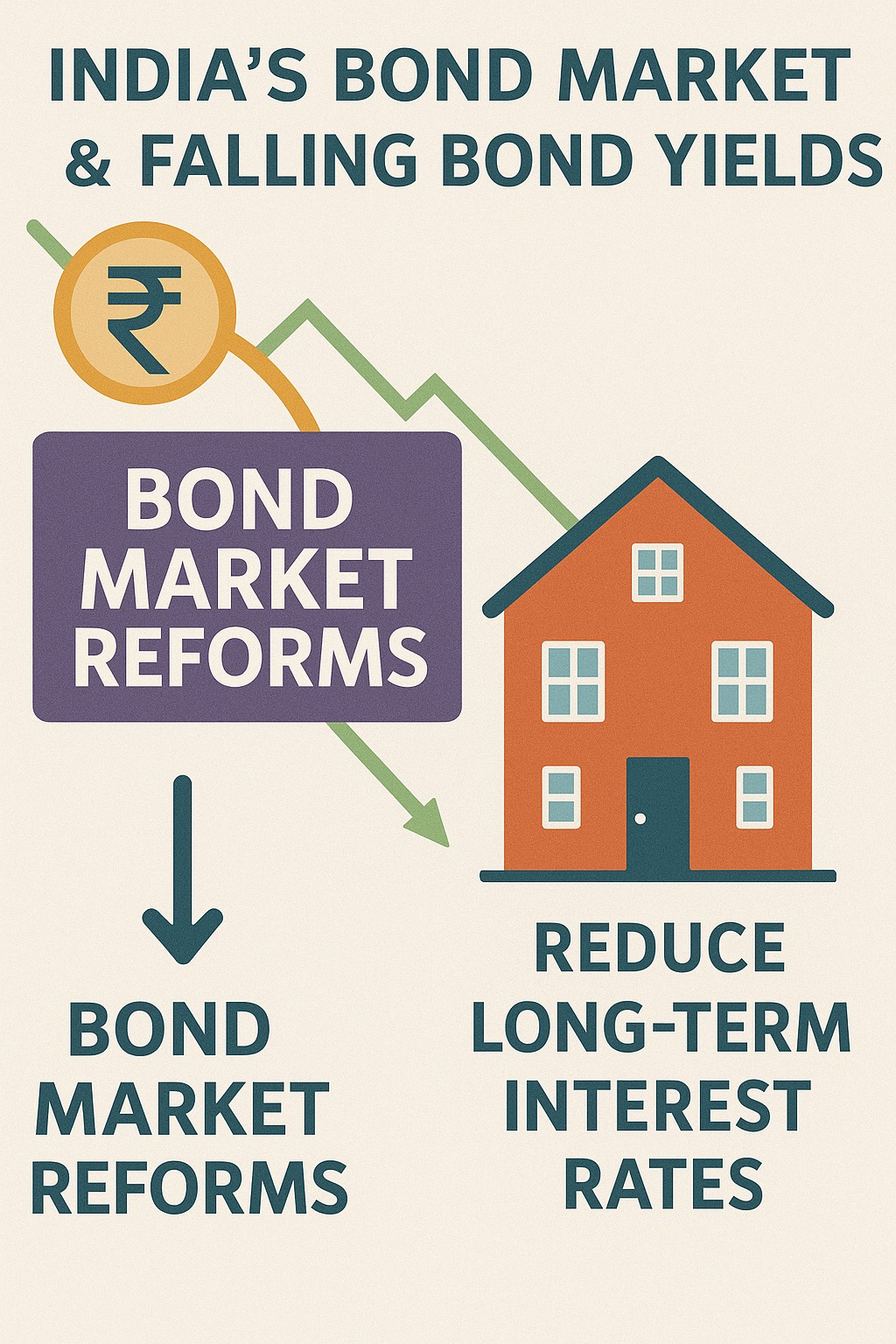

Introduction

India’s bond market is undergoing one of its biggest transformations in years—driven by regulatory reforms, foreign investor participation, stable inflation, and technological upgrades.

But what does this mean for homebuyers?

👉 Lower long-term loan rates and cheaper EMIs in coming years.

Since home loans in India often run for 15–30 years, they are heavily influenced by long-term bond yields, not just repo rates. When yields fall, banks borrow cheaper—and EMIs drop.

This blog gives a clear, practical explanation of why bond market changes matter and how they can reduce your home loan cost.

Understanding the Bond Market–Loan Rate Connection

Banks price long-term home loans using:

G-sec (Government Security) yields

Cost of long-term borrowing

Market liquidity

RBI’s regulatory policy

If bond yields fall → bank funding cost falls → home loan rates fall.

This especially affects:

RLLR home loans

MCLR-based floating loans

Long-term mortgage products

Housing finance company loan rates

What’s Changing in India’s Bond Market (2024–2026)

India’s bond market is becoming:

Deeper

More liquid

More transparent

More globally integrated

Key developments:

1. Inclusion of Indian Bonds in Global Indexes

Large foreign funds can now invest in Indian government bonds, increasing demand.

Higher demand → lower yields → cheaper loans.

2. Stable Inflation & Predictable Monetary Policy

Inflation trending within RBI’s comfortable band creates:

Lower long-term risk

Reduced yield volatility

Strong downward pressure on G-sec yields

3. Digital Bond Platforms & Retail Participation

Stock exchanges now allow easier retail bond purchases → wider market → stable yields.

4. Corporate Bond Reforms

RBI and SEBI are improving risk frameworks and trading platforms.

More stable corporate bond yields → cheaper borrowing for housing finance companies → lower mortgage rates.

Why Lower Bond Yields Reduce Home Loan Rates

1. Banks Borrow Cheaper

Banks raise long-term money via bonds.

Falling yields = lower cost = cheaper loans.

2. HFCs (Housing Finance Companies) Reprice Quickly

HFCs rely heavily on bond markets → lower yields directly reduce their lending rates.

3. G-sec Yields Guide Home Loan Rates

If 10-year G-sec yield falls from 7.2% to 6.5%, home loan rates can drop by 0.25–0.40%.

4. Long-Tenure Loans Benefit the Most

Home loans (15–30 years) align with long-term yields → big impact.

How Much Can Homebuyers Save If Bond Yields Fall?

Example:

Loan Amount: ₹50,00,000

Tenure: 20 years

Rate Drop: 0.30%

Monthly EMI Drop: ₹800–₹1,050

Annual Savings: ₹10,000–₹12,600

Total Savings: ₹2–2.5 lakh over loan tenure

A deeper bond market = larger long-term savings.

Why 2025–26 Could See Record-Low Home Loan Rates

Based on current economic trends:

Bond yields trending downward

Inflation stabilizing

RBI signaling long-term easing

Foreign bond inflows increasing

Banks reducing risk premium

Housing finance companies expanding lending

All these support lower long-term mortgage rates.

Expert Commentary

“India’s bond market is entering a golden phase. As yields stabilize and foreign participation expands, we will see a structural reduction in long-term borrowing costs. Home loans will be among the biggest beneficiaries.”

— R. Menon, Fixed-Income Strategist

Who Will Benefit the Most?

✔ First-time homebuyers

Cheaper EMIs improve loan eligibility.

✔ Existing borrowers planning balance transfer

Lower rates = big refinancing gains.

✔ HFC borrowers

HFCs pass bond yield benefits quickly.

✔ Salaried borrowers

Better stability for long-term planning.

What Borrowers Should Do Now

1. Prefer Floating-Rate Home Loans

Benefit immediately from yield-driven cuts.

2. Consider a Balance Transfer

If your rate is 0.50% higher than market, switch.

3. Track 10-Year G-Sec Yield

It indicates where home loan rates are headed.

4. Lock in Low Rates During Dips

Bond yields move fast—grab opportunities.

Summary Box

Bond market reforms → lower yields

Lower yields → cheaper home loans

Foreign participation boosts demand

Long-term rates likely to fall in 2025–26

Borrowers may see record-low mortgage rates

Best time to refinance or take new loans

Vizzve Financial helps homebuyers get the lowest interest rates, compare lenders instantly, and secure fast approvals with minimal documentation.

👉 Apply now at: www.vizzve.com

❓ FAQs

1. Do bond yields directly affect home loan interest rates?

Yes—especially long-term floating rates.

2. Will home loan rates fall in 2026?

Highly likely if yields keep trending downward.

3. Are HFCs faster to reduce rates?

Yes, because they rely more on bond market funding.

4. Should I choose fixed or floating during falling yields?

Floating usually performs better.

5. Is this a good time to refinance?

Yes, if your current rate is higher than market rate.

Conclusion

India’s bond market transformation is a silent but powerful catalyst for cheaper home loans.

With yields stabilizing and reforms kicking in, long-term home loan rates may fall significantly—making 2025–26 an excellent window for homebuyers.

Published on : 7th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed