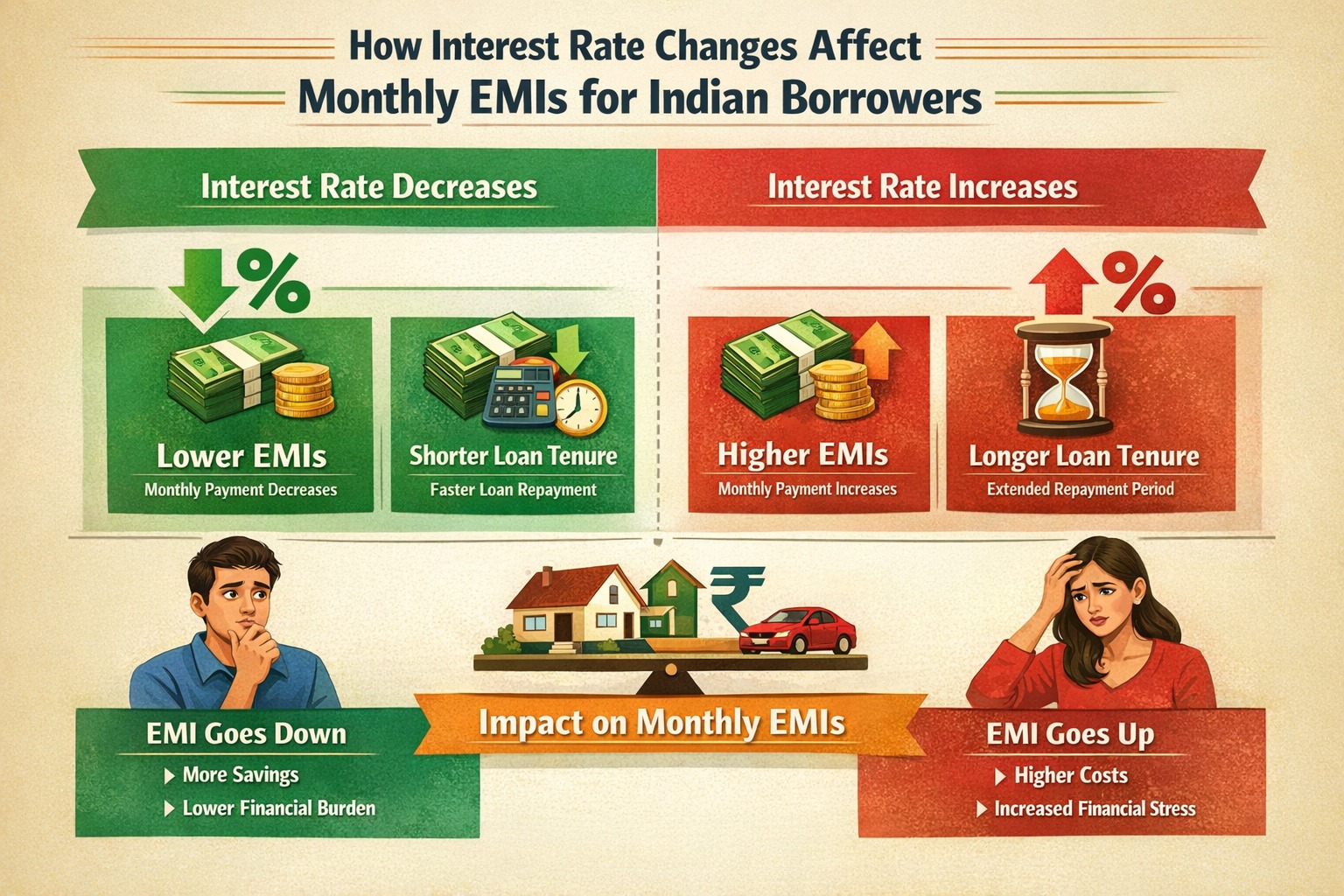

When interest rates rise, monthly EMIs increase or loan tenure extends (for floating-rate loans). When rates fall, EMIs reduce or loans get repaid faster, lowering the total interest paid by borrowers.

🔹 AI Answer Box

How interest rate changes affect EMIs:

Rate hike → higher EMI or longer tenure

Rate cut → lower EMI or shorter tenure

Floating-rate loans affected more

Fixed-rate loans stay unchanged

🔹 Introduction

Interest rate changes may look small on paper—but for borrowers, even a 0.5% change can significantly affect monthly EMIs and total loan cost. With RBI policy decisions influencing lending rates across banks and NBFCs, understanding this impact is crucial for smart financial planning.

This guide explains how and why EMIs change, with clear examples and borrower-friendly insights.

🔹 What Is an EMI?

An Equated Monthly Instalment (EMI) is the fixed amount you pay every month to repay a loan. It includes:

Principal (loan amount)

Interest (cost of borrowing)

Interest rate changes directly alter this balance.

🔹 How Interest Rates Influence EMIs

The Basic Relationship

Higher interest rate → Higher interest portion → Higher EMI

Lower interest rate → Lower interest portion → Lower EMI

But the impact depends on loan type and structure.

🔹 Floating vs Fixed Interest Rate Loans

🟢 Floating-Rate Loans

Linked to benchmark rates (repo rate, MCLR, etc.)

EMIs change when interest rates change

Most home and business loans fall here

🔵 Fixed-Rate Loans

Interest rate remains constant

EMIs do not change

Mostly personal loans and short-term loans

➡️ Borrowers with floating-rate loans feel rate changes the most.

EMI Impact Explained With Example

📊 Home Loan Example (₹50 lakh, 20 years)

| Interest Rate | Monthly EMI | Extra Cost Over Loan |

|---|---|---|

| 8.0% | ₹41,822 | Base |

| 8.5% | ₹43,391 | +₹3.8 lakh approx |

| 9.0% | ₹44,986 | +₹7.6 lakh approx |

📌 A 1% increase can add several lakhs over the loan tenure.

How Banks Adjust EMIs When Rates Change

Banks may:

Increase EMI amount

Extend loan tenure

Use a combination of both

Many banks prefer tenure extension first, which increases total interest burden silently.

Why RBI Policy Matters to Borrowers

The Reserve Bank of India controls key policy rates like the repo rate. When RBI:

Hikes rates → borrowing becomes costlier

Cuts rates → loans become cheaper

These changes eventually pass on to borrowers.

Impact on Different Types of Borrowers

Home Loan Borrowers

Highly sensitive to rate changes

Long tenure magnifies impact

Personal Loan Borrowers

Mostly fixed rates

Limited impact during tenure

Business Loan Borrowers

Floating rates common

Cash flow planning becomes critical

🔹 Rate Hike vs Rate Cut: Borrower Comparison

| Scenario | EMI Impact | Borrower Action |

|---|---|---|

| Rate Hike | EMI ↑ / Tenure ↑ | Prepay if possible |

| Rate Cut | EMI ↓ / Tenure ↓ | Review bank benefit |

| Stable Rates | No change | Maintain discipline |

🔹 How Borrowers Can Manage EMI Changes

Smart EMI Management Tips

Choose floating vs fixed wisely

Prepay during rate hikes

Avoid maximum tenure loans

Track RBI policy updates

Refinance if better rates available

🔹 Real-World Borrower Insight

From borrower repayment patterns, individuals who prepay even small amounts during rate hikes save lakhs in interest. EMI awareness—not income—determines long-term loan affordability.

🔹 Pros & Cons of Interest Rate Changes

✅ Pros

Rate cuts reduce loan burden

Opportunity to refinance cheaper

❌ Cons

Rate hikes increase EMI stress

Longer tenures increase total cost

🔹 Key Takeaways

Interest rate changes directly affect EMIs

Floating-rate borrowers face higher volatility

Small rate changes have big long-term impact

Active EMI management saves money

🔹 Frequently Asked Questions (FAQs)

1. Do all loans get affected by interest rate changes?

No, mainly floating-rate loans.

2. How fast do EMI changes reflect?

Within a few months of rate revision.

3. Can banks increase EMI without informing?

They must inform borrowers.

4. Is tenure extension bad?

It increases total interest paid.

5. Should I switch to fixed rate?

Depends on rate outlook and tenure.

6. Does prepayment help during rate hikes?

Yes, significantly.

7. Do rate cuts always reduce EMI?

Sometimes tenure reduces instead.

8. Are personal loans affected?

Mostly no, as rates are fixed.

9. Can I negotiate interest rates?

Yes, especially with good credit.

10. Does credit score affect EMI?

Indirectly, through interest rate offered.

11. Should I refinance when rates fall?

If savings outweigh costs.

12. Is EMI planning important?

Yes, for long-term financial health.

Conclusion

Interest rate changes are not just policy headlines—they directly affect your monthly budget and long-term wealth. Borrowers who understand EMI dynamics make better decisions, stay stress-free, and save more over time.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 8th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed