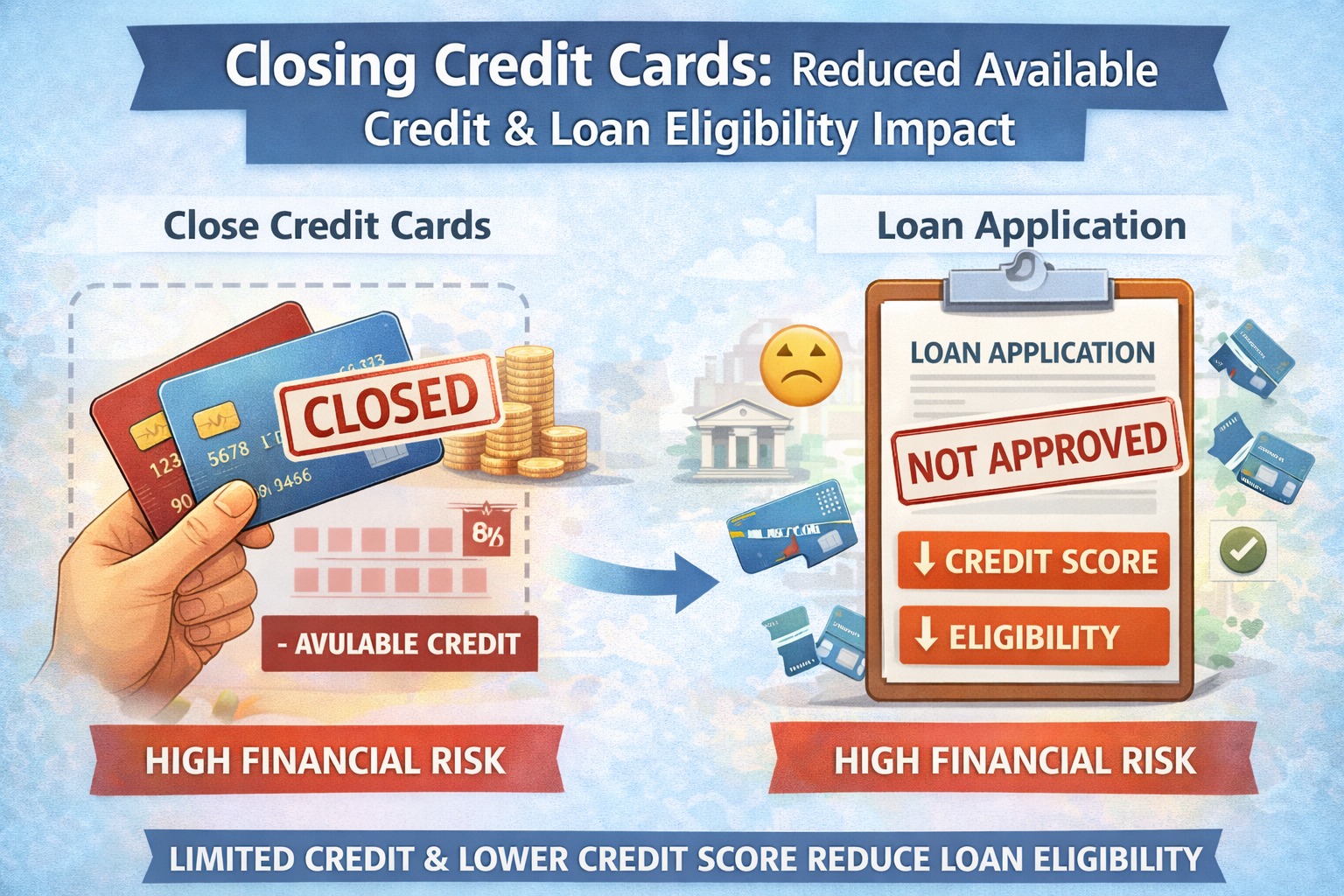

Closing credit cards can reduce loan eligibility because it lowers available credit, increases utilisation ratios, shortens credit history, and weakens your credit profile in lenders’ eyes.

AI Answer Box

Does closing a credit card affect loan eligibility?

Yes. Closing a credit card reduces your available credit limit and credit history length, which can increase utilisation ratios and make lenders see you as a higher-risk borrower.

Introduction: “I Closed My Credit Cards to Be Responsible—So Why Was My Loan Rejected?”

This is a surprisingly common story.

You:

Cleared your credit card dues

Closed unused cards

Reduced credit exposure

Yet when you applied for a loan:

Eligibility dropped

Interest rate increased

Or approval was denied

The issue isn’t discipline.

It’s how credit systems interpret behaviour.

Expert Commentary

“Credit cards are not just spending tools—they are signals. Closing them removes valuable data lenders use to assess risk.”

— Credit Scoring Consultant, India

How Lenders Actually View Credit Cards

Credit Cards Are Capacity Indicators, Not Just Debt

To lenders, credit cards show:

How much credit you’re trusted with

How responsibly you use it

Whether you can handle revolving credit

📌 A credit card limit is unused capacity, not automatic debt.

Reason #1: Closing Cards Reduces Available Credit

Why Credit Limit Matters

Loan eligibility models look at:

Total available credit

Current usage

Utilisation ratio

When you close a card:

Total credit limit drops

Same spending now uses a higher %

Risk perception increases

📌 Even with zero dues, your profile looks tighter.

Example: Utilisation Ratio Impact

| Scenario | Credit Limit | Usage | Utilisation |

|---|---|---|---|

| Before closure | ₹4,00,000 | ₹40,000 | 10% ✅ |

| After closing 1 card | ₹2,00,000 | ₹40,000 | 20% ⚠️ |

📌 Same spending. Higher perceived risk.

Reason #2: Credit History Gets Shorter

Old Cards Strengthen Your Profile

Long-standing credit cards:

Increase average account age

Show long-term discipline

Build trust over time

Closing older cards:

Shortens credit history

Removes positive data

Slows score improvement

📌 Time is a non-replaceable factor in credit scoring.

Reason #3: Fewer Active Accounts = Less Data

Lenders Prefer Predictability

Active, well-managed cards provide:

Monthly behaviour data

Proof of consistency

Risk patterns over time

Closing cards:

Reduces data points

Makes behaviour harder to assess

📌 Less data = more caution from lenders.

Reason #4: Closure Can Signal Risk Aversion or Instability

To automated systems, sudden closures may suggest:

Financial stress

Behavioural shift

Reduced credit confidence

📌 Systems don’t ask why—they just read what happened.

Real-World Experience Insight

Many borrowers see:

Credit score dip after card closure

Lower loan limits offered

Higher interest rates

Even though:

No payments were missed

No debt was carried

📌 Credit systems reward managed access, not avoidance.

When Closing a Credit Card Makes Sense

Smart Closures vs Harmful Closures

Closing a card is reasonable when:

Fees are high and unjustified

Card is newly opened and unused

Multiple cards strain discipline

Avoid closing when:

Card is old

Limit is high

Usage is low and controlled

📌 Keep the cards that strengthen history and capacity.

Smarter Alternatives to Closing Cards

What to Do Instead

Keep cards active with minimal use

Reduce credit limits if needed

Set spending alerts

Avoid carrying balances

📌 Presence without pressure is ideal.

Myths vs Reality

| Myth | Reality |

|---|---|

| Closing cards improves credit | Often reduces eligibility |

| Fewer cards = safer profile | Managed access is safer |

| Zero credit exposure is best | Predictable usage is best |

| Credit cards are bad for loans | Misuse is bad—not cards |

Key Takeaways

Credit cards show capacity, not just debt

Closing cards reduces available credit

Utilisation ratio worsens quietly

Credit history shortens

Loan eligibility can drop despite discipline

In credit systems, controlled access beats total avoidance.

❓ Frequently Asked Questions (FAQs)

1. Does closing a credit card reduce credit score?

Often yes, temporarily.

2. Should I close unused cards?

Not if they’re old and free.

3. How many credit cards are ideal?

Enough to show capacity, not chaos.

4. Is zero credit card usage good?

Low usage is good; zero data is not.

5. Can closing cards hurt loan approval?

Yes, especially before applying.

6. How long before loan application should I avoid closures?

At least 6–12 months.

7. Is high credit limit bad?

No, if utilisation is low.

8. Can I reduce limit instead of closing?

Yes—that’s often better.

9. Do lenders prefer card users?

They prefer disciplined users.

10. What’s better—one card or many?

Few well-managed cards.

Conclusion

Closing credit cards feels like discipline—but in modern lending, disciplined usage matters more than withdrawal.

If you want better loan eligibility:

Keep credit lines open

Use them lightly

Manage them consistently

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply now at www.vizzve.com

Published on : 30th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed