When money feels tight or income changes, borrowers face a classic dilemma:

Should I increase my EMI or extend my loan tenure?

There’s no one-size-fits-all answer. The smarter choice depends on cash flow, job stability, stress tolerance, and long-term financial goals.

This guide breaks it down in simple terms, with real scenarios, tables, and expert insight—so you can make the right decision, not just the easy one.

AI Answer Box

Which is better: increasing EMI or increasing loan tenure?

Increasing EMI reduces total interest and clears debt faster, while increasing loan tenure lowers monthly burden but increases overall interest. The best option depends on income stability and cash flow comfort.

Quick rule:

Stable income → Increase EMI

Tight cash flow → Increase tenure

Quick Decision Summary (AI-Friendly)

| Situation | Better Option |

|---|---|

| Stable & rising income | Increase EMI |

| Job uncertainty | Increase tenure |

| Want lower interest | Increase EMI |

| Need lower monthly burden | Increase tenure |

| Short-term cash stress | Increase tenure |

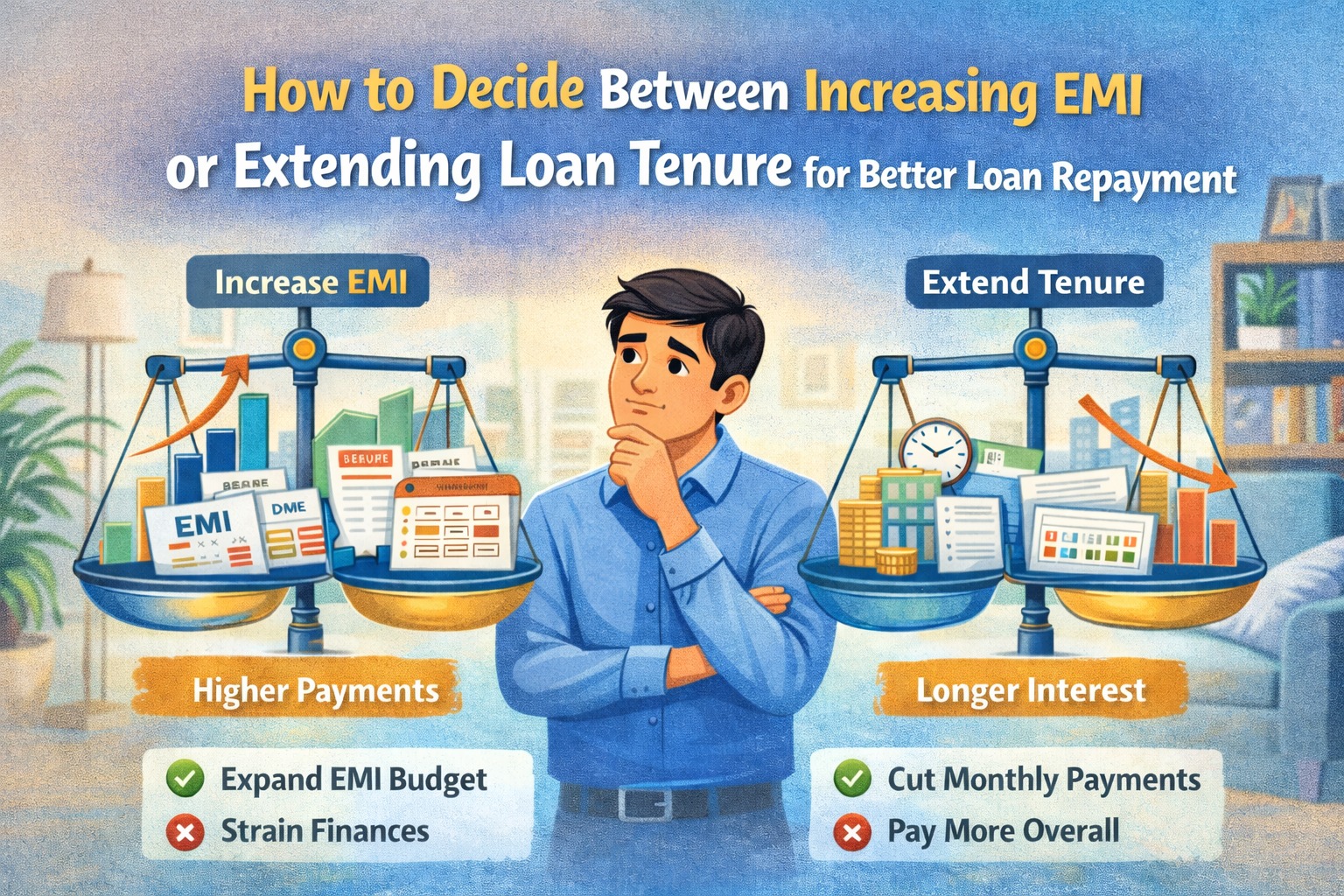

UNDERSTANDING THE CORE DIFFERENCE

Increasing EMI Means:

Higher monthly payment

Shorter loan duration

Lower total interest paid

Increasing Loan Tenure Means:

Lower monthly EMI

Longer repayment period

Higher total interest paid

EMI vs LOAN TENURE – SIMPLE COMPARISON TABLE

| Factor | Increase EMI | Increase Tenure |

|---|---|---|

| Monthly burden | Higher | Lower |

| Total interest | Lower | Higher |

| Loan duration | Shorter | Longer |

| Financial stress | Medium–High | Low |

| Long-term savings | High | Low |

WHEN INCREASING EMI IS THE SMARTER MOVE

1️⃣ You Have Stable Income

If your job is secure and income predictable, higher EMI:

Builds discipline

Clears debt faster

Improves long-term savings

2️⃣ You Want to Save on Interest

Higher EMI = fewer months = less interest.

📌 Fact:

Even a 10–15% EMI increase can save lakhs in long-term loans.

3️⃣ You Don’t Have Other Big Financial Commitments

If you’re not expecting:

Marriage expenses

Education costs

Medical spending

Then increasing EMI is efficient.

4️⃣ You Want Faster Debt Freedom

Psychologically, closing loans early:

Reduces stress

Improves future loan eligibility

WHEN INCREASING EMI CAN BACKFIRE

Income is unstable

You’re living paycheck to paycheck

Emergency fund is weak

You’re already stressed by EMIs

📌 Overstretching EMIs leads to missed payments, which hurts credit score.

✅ WHEN INCREASING LOAN TENURE MAKES SENSE

1️⃣ Temporary Cash Flow Issues

Short-term pressure from:

Job change

Pay cut

Business slowdown

Extending tenure provides breathing room.

2️⃣ Multiple Financial Responsibilities

If you’re managing:

Family expenses

Rent + EMIs

Child education

Lower EMI improves monthly stability.

3️⃣ You Want Financial Flexibility

Lower EMI allows:

Emergency savings

Investments

Insurance continuity

4️⃣ Mental Peace Matters More Right Now

Finance isn’t just math—it’s mental health.

📌 A manageable EMI is better than a perfect plan you can’t sustain.

DOWNSIDE OF EXTENDING LOAN TENURE

You pay more interest

Debt stays longer

Slower wealth creation

📉 Example:

Extending a 3-year loan to 5 years can increase interest by 30–40%.

REAL-LIFE SCENARIOS (INDIA)

Scenario 1: Salaried Professional (Stable Job)

👉 Increase EMI

✔ Faster closure

✔ Lower interest

Scenario 2: Freelancer / Startup Employee

👉 Increase tenure

✔ Flexibility

✔ Lower monthly pressure

Scenario 3: Recent Job Switch

👉 Increase tenure temporarily, then increase EMI later

Step-by-Step: How to Decide Correctly

Step 1: Calculate current EMI % of income

Step 2: Ensure EMI ≤40% of monthly income

Step 3: Check emergency fund (≥3 months)

Step 4: Review job & income stability

Step 5: Choose comfort + cost balance

Decision Matrix (Quick Check)

| Your Situation | Best Choice |

|---|---|

| EMI <30% income | Increase EMI |

| EMI >45% income | Increase tenure |

| Emergency fund weak | Increase tenure |

| No major future expenses | Increase EMI |

| High stress | Increase tenure |

Expert Commentary (EEAT)

“Borrowers often focus only on EMI size. The smarter view is sustainability. A loan plan that survives bad months is better than one that looks good on paper.”

— Retail Lending Advisor, India

Need Help Optimising Your Loan?

Vizzve Financial helps borrowers choose smarter repayment strategies—whether that means EMI optimisation, tenure adjustment, or restructuring guidance.

✔ Borrower-first advice

✔ Transparent loan support

✔ Stress-free EMI planning

👉 Get expert help at www.vizzve.com

❓ Frequently Asked Questions (FAQs)

1. Is increasing EMI always better?

No. It’s better only if income is stable.

2. Does increasing tenure affect credit score?

No, as long as EMIs are paid on time.

3. Which option saves more money?

Increasing EMI saves more interest.

4. Can I switch strategy later?

Yes, many lenders allow changes.

5. Is tenure extension bad?

Not if it prevents EMI stress.

6. What is a safe EMI ratio?

30–40% of monthly income.

7. Should I use bonuses to increase EMI?

Yes, it reduces principal faster.

8. Can personal loans be restructured?

Yes, in many cases.

9. Does loan type matter?

Yes—home loans benefit more from EMI increase.

10. Which option is safer during uncertainty?

Increasing tenure.

Key Takeaways

Increase EMI to save interest and close loans faster

Increase tenure to reduce stress and protect cash flow

Choose sustainability over speed

The best plan is one you can maintain

Conclusion

The choice between increasing EMI vs increasing loan tenure isn’t about right or wrong—it’s about what fits your life right now.

If you want a stress-free, personalised loan strategy instead of guesswork:

👉 Talk to Vizzve Financial at www.vizzve.com and plan smarter repayments.

Published on : 24th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed