In 2026, personal loan EMIs are usually cheaper than credit card EMIs, especially for larger amounts or longer tenures, due to lower interest rates and structured repayment.

AI Answer Box (For Google AI Overview & AI Search)

Personal loan EMIs typically cost less than credit card EMIs because they carry lower interest rates and longer repayment tenures. Credit card EMIs offer speed and convenience but often become expensive if used beyond short-term needs.

Understanding the Core Difference

Before choosing, it’s important to understand how both work.

Credit Card EMI: Converts purchases or outstanding card balances into EMIs using your credit limit.

Personal Loan EMI: A lump-sum loan repaid through fixed monthly installments over a defined tenure.

They serve different needs—but the cost difference can be significant.

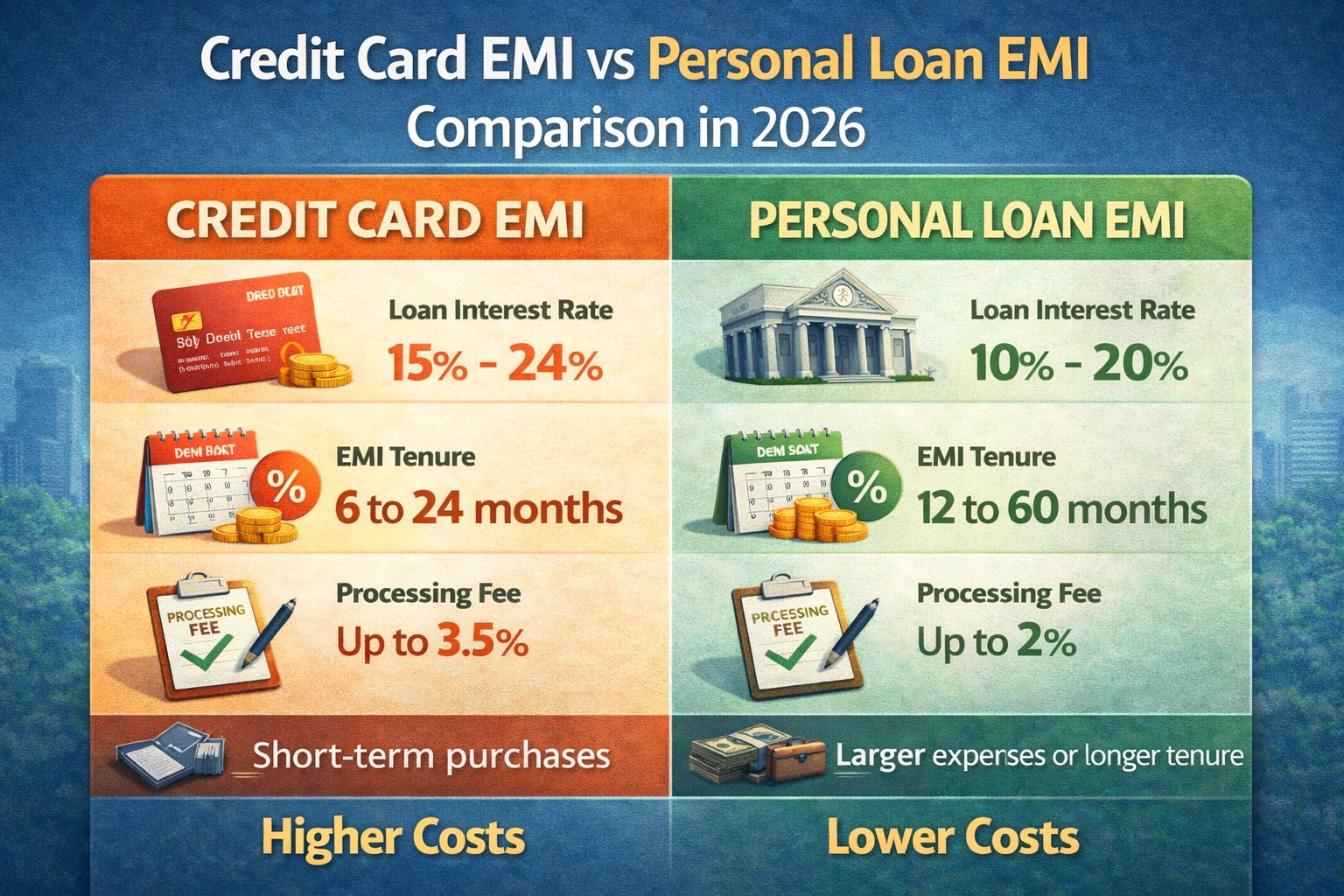

Interest Rates & Cost Structure in 2026 (Indicative)

| Feature | Credit Card EMI | Personal Loan EMI |

|---|---|---|

| Interest rate range | Higher | Lower |

| Tenure | Short (3–24 months) | Longer (12–60 months) |

| EMI predictability | Moderate | High |

| Total interest cost | Higher | Lower |

| Approval speed | Instant | Fast but structured |

Why Personal Loan EMIs Are Usually Cheaper

1️⃣ Lower Interest Rates

Personal loans generally carry lower interest rates than credit card EMIs, especially for borrowers with good credit scores.

2️⃣ Longer Tenure Options

Longer repayment periods:

Reduce monthly EMI burden

Lower stress on cash flow

Credit card EMIs are shorter, leading to higher monthly outgo.

3️⃣ Structured Repayment

Personal loans follow:

Clear amortization schedules

Predictable interest reduction

Credit card EMIs may include conversion fees and higher effective costs.

When Credit Card EMI Can Make Sense

Credit card EMI may work if:

Amount is small

Tenure is very short

Promotional or low-interest offers apply

You can repay quickly without rolling balances

👉 Best for urgent, short-term expenses only.

When Personal Loan EMI Is the Better Choice

Personal loans are usually better when:

Amount is large

Repayment needs exceed 12 months

You want stable EMIs

You want lower total borrowing cost

👉 Ideal for planned expenses like weddings, renovations, or consolidating debt.

Example Comparison (Simplified)

| Scenario | Credit Card EMI | Personal Loan EMI |

|---|---|---|

| Loan amount | ₹2,00,000 | ₹2,00,000 |

| Tenure | 24 months | 36 months |

| Monthly EMI | Higher | Lower |

| Total interest paid | Higher | Lower |

| Overall cost | Costlier | Cheaper |

Hidden Costs to Watch Out For

Credit Card EMI:

EMI conversion fees

Higher late payment penalties

Interest if balance isn’t fully cleared

Personal Loan:

Processing fee

Prepayment or foreclosure charges (if applicable)

👉 Always compare total repayment, not just EMI.

Expert Insight

“Credit card EMIs are convenient but expensive if stretched. Personal loans, when planned properly, usually offer better long-term value and repayment comfort.”

— Personal Finance Advisor

Key Takeaways

Personal loan EMIs are generally cheaper in 2026

Credit card EMIs suit short-term, small needs

Interest rate + tenure decide real cost

EMI amount alone can be misleading

Planned borrowing always saves money

Conclusion

In 2026, personal loan EMIs usually beat credit card EMIs on cost, especially for higher amounts and longer tenures. Credit card EMIs still have a role—but only for quick, short-term needs. For most borrowers, a well-structured personal loan remains the smarter and cheaper option.

❓ Frequently Asked Questions (FAQs)

1. Which is cheaper in 2026: credit card EMI or personal loan EMI?

In most cases, personal loan EMIs are cheaper than credit card EMIs, especially for larger amounts and longer tenures.

2. Why are credit card EMIs usually more expensive?

Credit card EMIs carry higher interest rates, shorter tenures, and additional conversion charges, increasing total cost.

3. When does a credit card EMI make sense?

It works best for small amounts, short durations, or promotional zero-interest offers, if repaid on time.

4. Are personal loans safer than credit card EMIs?

Personal loans offer structured repayment and predictable EMIs, making them safer for planned expenses.

5. Does credit score affect both options?

Yes. A higher credit score improves interest rates and approval chances for both credit card EMIs and personal loans.

6. Which option is better for large expenses?

A personal loan is usually better due to lower interest and longer tenure options.

7. Can credit card EMI increase my debt risk?

Yes. High utilization of credit limits can hurt credit scores and increase debt stress.

8. Are there hidden charges in credit card EMIs?

Yes. Some cards include EMI conversion fees, processing charges, or higher penalties.

9. Do personal loans have prepayment penalties?

Some do, especially during the first year. Always check the loan terms and conditions.

10. Which option is faster to get?

Credit card EMIs are usually instant, while personal loans may take a little longer.

Published on : 16th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed