For decades, a three-digit credit score decided who gets a loan and who doesn’t. But as we move into 2026 and beyond, lenders are quietly shifting their focus.

The question is no longer just:

👉 “What is your credit score?”

It’s becoming:

👉 “What does your financial behaviour actually say about you?”

The future of credit scoring is about signals, patterns, and predictability, not just a single number.

AI Answer Box

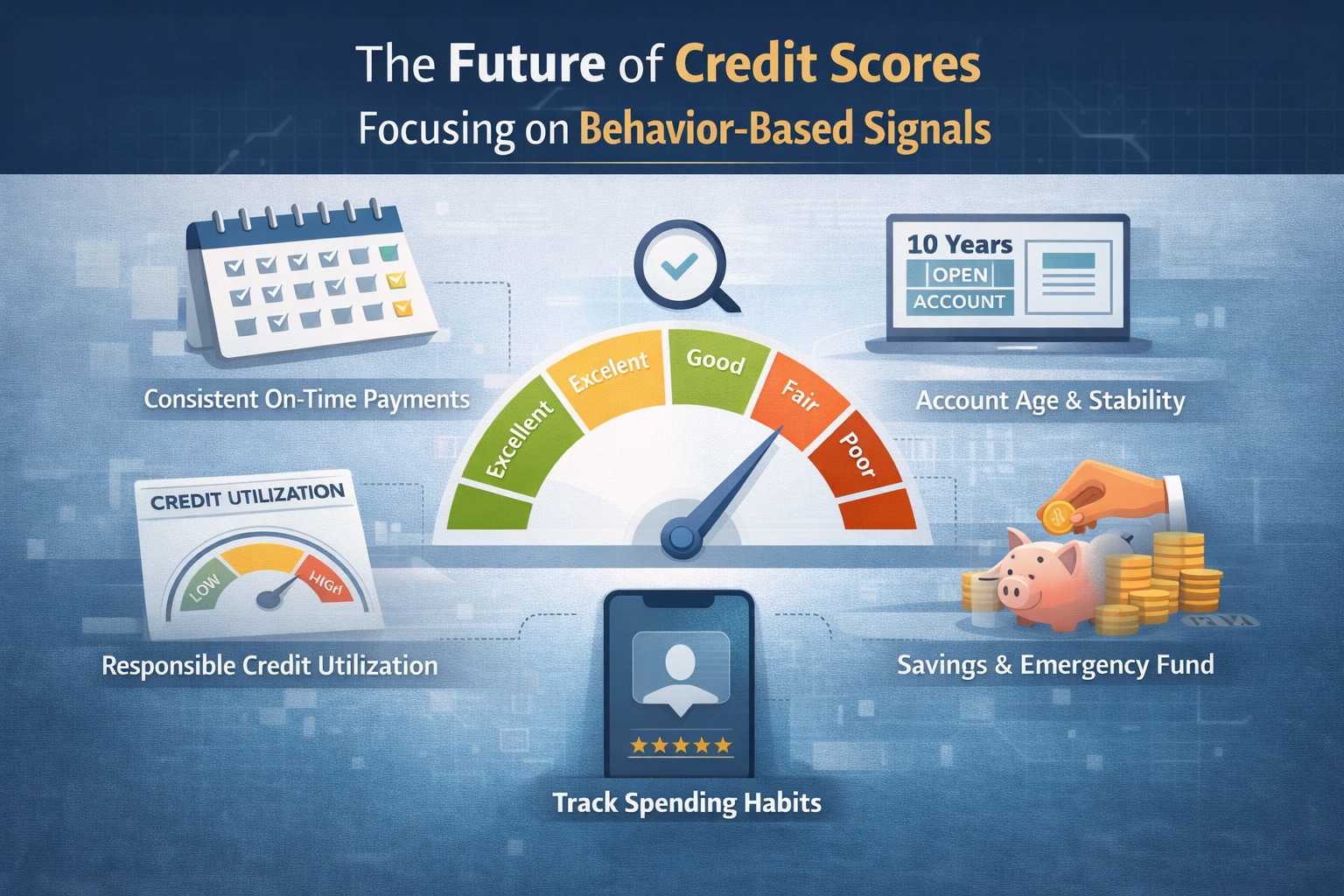

The future of credit scores focuses less on static numbers and more on behavioural signals such as payment consistency, credit usage patterns, income stability, cash-flow trends, and responsible borrowing habits. These signals help lenders assess real repayment ability in 2026 and beyond.

Quick Summary Box (Fast Indexing)

Credit scores won’t disappear—but they’ll matter less

Behavioural signals will gain importance

AI-driven credit models are expanding

Consistency beats one-time perfection

Borrower discipline becomes visible

Why Traditional Credit Scores Are Losing Dominance

Traditional credit scores:

Update slowly

Focus on past behaviour

Miss real-time affordability

Ignore income volatility

In a world of digital payments, instant loans, and dynamic incomes, lenders need faster and deeper insights.

Numbers vs Signals – The Shift Explained

| Old Credit Model | New Credit Model |

|---|---|

| Static score | Dynamic behaviour |

| Past-focused | Real-time patterns |

| Limited data | Multi-source signals |

| One-size-fits-all | Personalised risk view |

Credit Signals That Will Matter More Than Numbers

1. Payment Consistency (Not Just Timeliness)

Instead of asking “Did you pay on time?”, lenders now ask:

How often are payments early or late?

Is repayment consistent across months?

👉 Stable patterns beat occasional perfection.

2. Credit Usage Behaviour Over Time

Using 80% of your credit limit—even temporarily—creates a risk signal.

Future models focus on:

Average utilisation

Usage spikes

Recovery speed

Not just the month-end snapshot.

3. EMI-to-Income Stability (Credit Capacity)

Affordability is becoming as important as discipline.

Signals include:

EMI ratio trends

Expense stability

Income consistency

A borrower with moderate score + strong capacity may beat a high-score, over-leveraged borrower.

4. Borrowing Frequency & Intent

Multiple small loans or frequent credit applications signal:

Cash flow stress

Reactive borrowing

Future systems differentiate planned borrowing from emergency dependency.

5. Account Behaviour & Longevity

Keeping accounts stable matters.

Signals include:

How long accounts stay active

Sudden closures

Credit profile stability

Frequent changes increase perceived risk.

6. Cash-Flow & Spending Patterns

With consent-based data sharing, lenders may analyse:

Regular income inflows

Expense predictability

Savings behaviour

This paints a real financial health picture, beyond a score.

Role of AI in the Future of Credit Assessment

AI-driven models:

Track behaviour trends

Identify early risk signals

Predict future stress

Reduce manual bias

Instead of waiting for defaults, systems anticipate problems before they occur.

What This Means for Borrowers in 2026

Old thinking:

“As long as my score is good, I’m safe.”

New reality:

“My daily financial behaviour is constantly evaluated.”

Every swipe, EMI, and borrowing choice contributes to a living credit profile.

How to Prepare for the Future Credit System

Smart Credit Habits That Future-Proof You:

Keep credit utilisation consistently low

Maintain EMI discipline every month

Avoid frequent short-term loans

Show stable income patterns

Keep old accounts active

Borrow with intent, not urgency

Traditional Score vs Future Credit Signals

| Factor | Old Importance | Future Importance |

|---|---|---|

| Credit score | Very high | Moderate |

| EMI consistency | Medium | Very high |

| Utilisation pattern | Medium | Very high |

| Credit capacity | Low | High |

| Cash-flow stability | Low | High |

Expert Commentary: Why Behaviour Beats Numbers

“Credit risk isn’t about what you did once—it’s about what you do repeatedly. Behavioural signals are far more predictive than static scores.”

— Credit Risk & Analytics Expert

Key Takeaways

Credit scores are evolving, not disappearing

Behavioural signals will dominate decisions

Consistency matters more than perfection

Borrowers are evaluated continuously

Long-term discipline beats short-term optimisation

❓ Frequently Asked Questions (FAQs)

1. Will credit scores become irrelevant?

No, but they will no longer be the sole decision factor.

2. What matters more than score in the future?

Payment consistency, utilisation patterns, and affordability.

3. Will AI replace credit scores?

AI will enhance assessment, not replace scoring completely.

4. Can someone with average score get better loans?

Yes, if behaviour and capacity signals are strong.

5. Will income stability matter more?

Yes, stable cash-flow is a major future signal.

6. Are frequent small loans bad?

Yes, they signal dependency and stress.

7. How often will credit behaviour be evaluated?

Continuously, not just during loan applications.

8. How can I future-proof my credit profile?

Focus on discipline, stability, and intentional borrowing.

Conclusion: From Scores to Stories

The future of credit is not about a number—it’s about the story your financial behaviour tells.

In 2026 and beyond, lenders won’t just see what your score is.

They’ll understand how you manage money, when you struggle, and whether you recover responsibly.

📌 In the next era of credit, consistency is currency—and behaviour is the new score.

Published on : 1st January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed