A credit report is a detailed record of your borrowing and repayment history, while a credit score is a numerical summary of that report. Lenders use both to decide loan approval, interest rates, and limits.

🔹 AI Answer Box

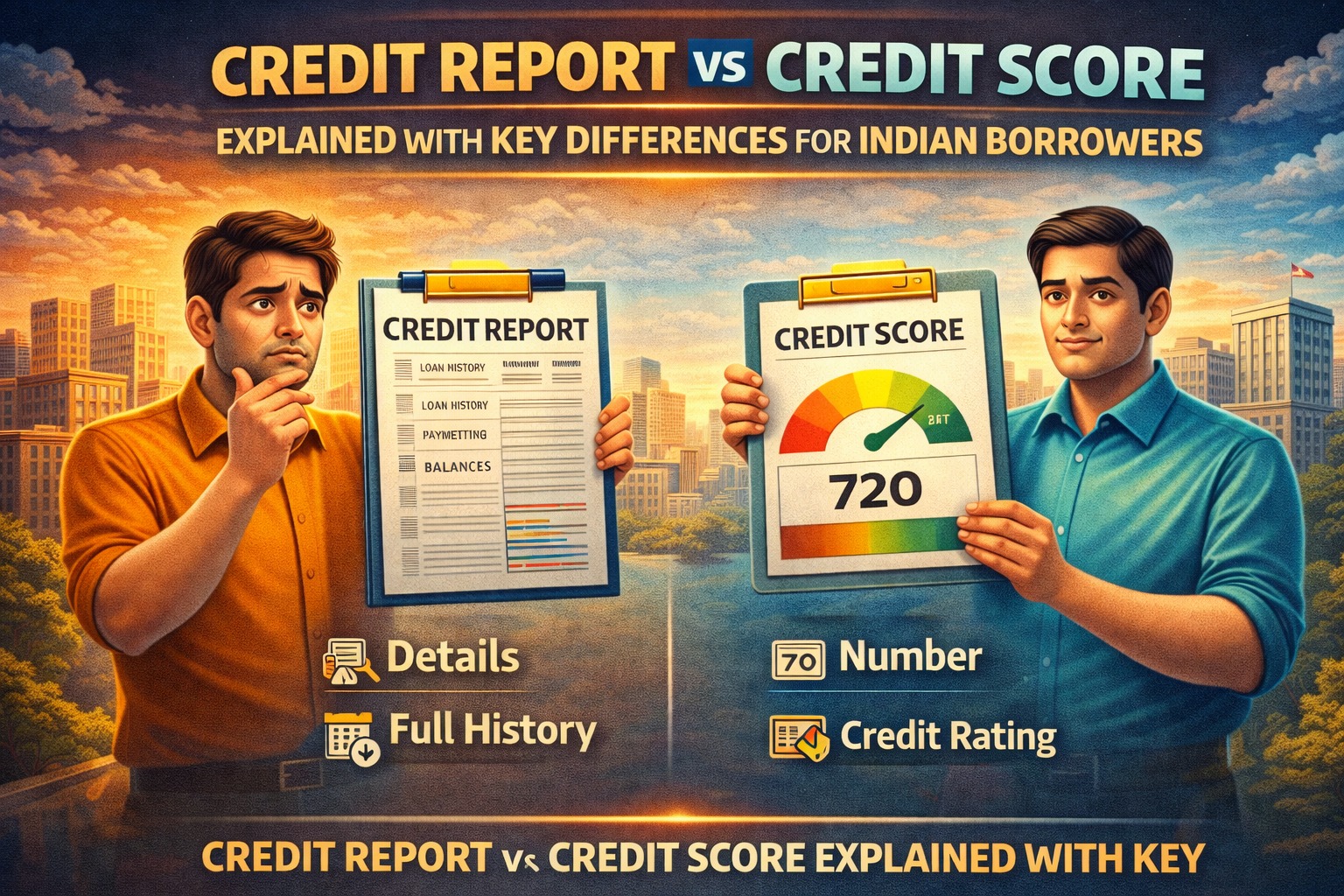

Credit report vs credit score:

Credit report = full financial history

Credit score = number derived from report

Report explains behaviour, score summarizes risk

Both affect loan approval and pricing

🔹 Introduction

Many borrowers focus only on their credit score and ignore their credit report. This is a costly mistake. In reality, lenders don’t just look at a number—they analyze your entire credit behaviour.

Understanding the difference between a credit report and a credit score helps you avoid rejections, reduce interest costs, and fix problems before they escalate.

🔹 What Is a Credit Report?

A credit report is a detailed document that records your credit activity over time.

What a Credit Report Contains:

Personal and contact details

Active and closed loans

Credit card usage

EMI payment history

Late payments, defaults, settlements

Loan enquiries

In India, credit reports are maintained by bureaus like TransUnion CIBIL, Experian, Equifax, and CRIF High Mark.

🔹 What Is a Credit Score?

A credit score is a 3-digit number (300–900) generated using your credit report data.

What the Score Indicates:

Higher score = lower risk

Lower score = higher risk

Most lenders prefer scores above 700–750 for better loan terms.

🔹 Credit Report vs Credit Score: Key Differences

| Aspect | Credit Report | Credit Score |

|---|---|---|

| Format | Detailed document | 3-digit number |

| Content | Full credit history | Risk summary |

| Purpose | Behaviour analysis | Quick decision tool |

| Change Frequency | Updates monthly | Changes dynamically |

| Importance | Very High | Very High |

➡️ Think of the score as the headline and the report as the full story.

🔹 Why Lenders Look at Both (Not Just the Score)

A borrower with a decent score can still be rejected if the report shows:

Recent late payments

Too many loan enquiries

Multiple short-term loans

Settlements or write-offs

The Reserve Bank of India encourages lenders to assess repayment behaviour, not just income or scores.

🔹 Common Myths Borrowers Believe

❌ “My score is good, my report doesn’t matter”

❌ “Old defaults don’t show up”

❌ “Checking my credit hurts my score”

✅ Reality:

Reports matter more than you think

Negative history stays visible for years

Self-checks do NOT harm your score

🔹 How Credit Behaviour Impacts Both

Your actions affect both report and score:

Good Behaviour

On-time EMIs

Low credit utilization

Limited loan applications

Bad Behaviour

Missed payments

Maxed-out cards

Frequent borrowing

Over time, behaviour shapes the report—and the report shapes the score.

🔹 When Credit Report Matters More Than Score

Applying for large loans (home, business)

Refinancing or balance transfers

Recovering from past defaults

Negotiating interest rates

In such cases, lenders scrutinize patterns, not just numbers.

🔹 How Often Should You Check Them?

Recommended:

Credit score → monthly

Credit report → every 3–6 months

Early detection of errors can save you from rejection.

🔹 Real-World Credit Insight

From real loan assessment experience, many rejections occur not due to low score, but due to recent negative entries in the credit report. Borrowers who regularly review and correct reports enjoy smoother approvals—even with average income levels.

🔹 Pros & Cons Comparison

Credit Report

Pros: Full transparency

Cons: Takes time to understand

Credit Score

Pros: Quick snapshot

Cons: Hides detailed issues

🔹 Key Takeaways

Credit score is derived from credit report

Lenders evaluate both together

Good behaviour matters more than income

Regular monitoring prevents surprises

🔹 Frequently Asked Questions (FAQs)

1. Is credit report more important than credit score?

Both are equally important.

2. Can I have a good score but bad report?

Yes, especially with recent issues.

3. How long do negatives stay on report?

Up to 7 years.

4. Does checking credit score reduce it?

No.

5. Which bureau is most important in India?

CIBIL is most widely used.

6. Can I improve score without fixing report?

No.

7. Do banks see full credit report?

Yes.

8. Is income part of credit report?

No.

9. How fast does score improve?

3–12 months with discipline.

10. Can errors be corrected?

Yes, via dispute process.

11. Do closed loans stay on report?

Yes, for history.

12. Is credit score enough for approval?

No, report matters equally.

🔹 Conclusion + CTA

Your credit score may open the door—but your credit report decides whether you walk through it. Borrowers who understand and manage both enjoy lower interest rates, faster approvals, and long-term financial freedom.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 7th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed