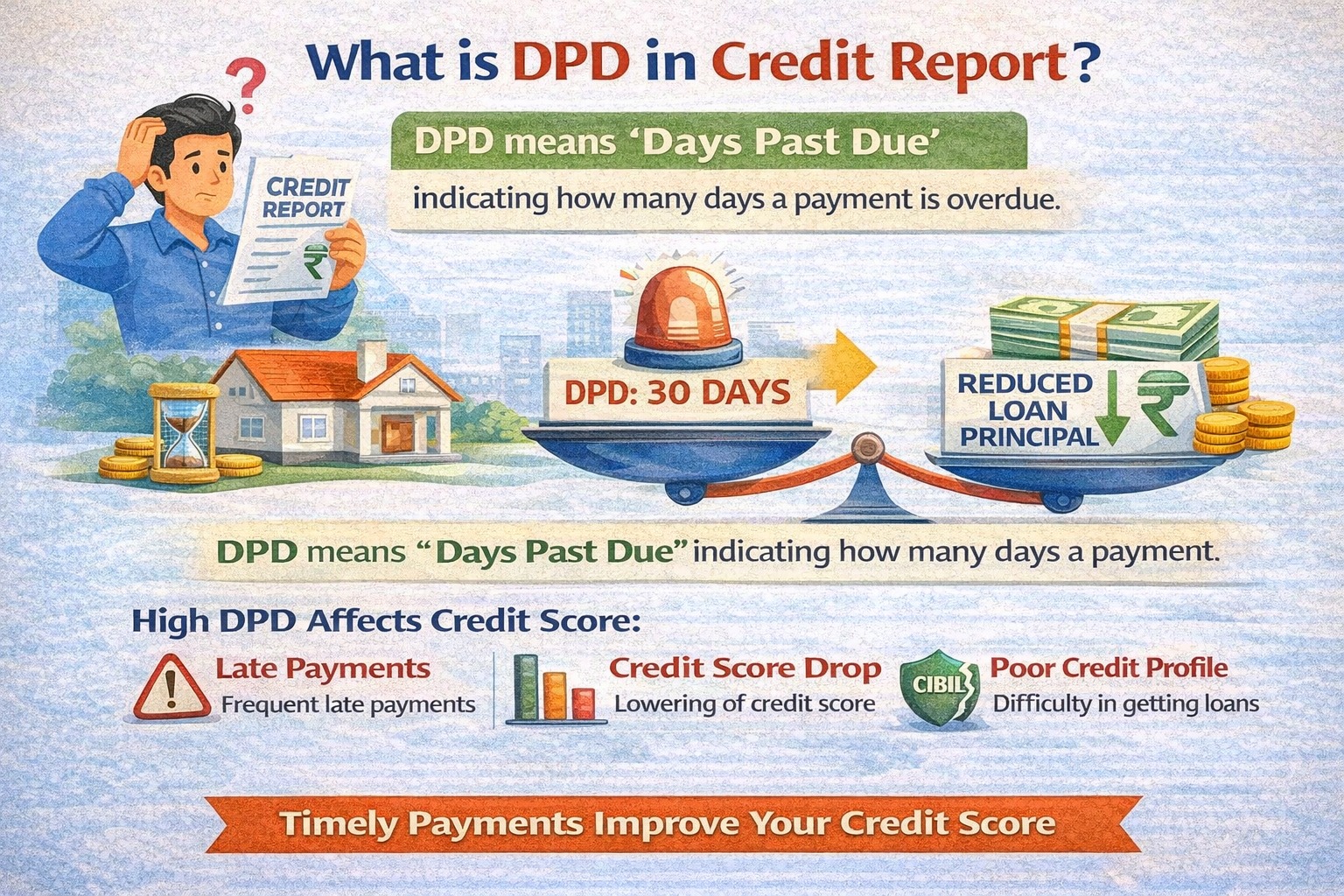

DPD stands for “Days Past Due” and shows how many days your loan or credit card payment is overdue.

Higher DPD means delayed payments and leads to a lower credit score.

AI ANSWER BOX

What is DPD in a credit report?

DPD (Days Past Due) indicates the number of days a borrower has delayed EMI or credit card payment. A higher DPD reflects higher credit risk and negatively impacts credit score.

INTRODUCTION

If you’ve ever checked your CIBIL or credit report, you may have noticed numbers like 0, 30, 60, or 90 under the DPD column. Many borrowers panic seeing these numbers without understanding what they mean.

DPD is one of the most important indicators of your repayment discipline.

This guide explains:

What DPD means

How it appears in credit reports

Different DPD levels

How DPD affects credit score

How to fix or improve DPD

Written with real borrower experience and credit-industry insight, this blog helps you stay credit-healthy.

WHAT IS DPD IN CREDIT REPORT?

DPD = Days Past Due

It shows the number of days your EMI or credit card payment is overdue.

Example:

EMI due date: 5th June

EMI paid on: 20th June

➡️ DPD = 15 days

📌 DPD is reported monthly by banks and NBFCs to credit bureaus.

HOW DPD APPEARS IN A CREDIT REPORT

In your credit report, DPD is shown as a numeric value under each loan or credit card account.

| DPD Value | Meaning |

|---|---|

| 0 | Payment on time |

| 1–30 | Slight delay |

| 31–60 | Moderate delay |

| 61–90 | Serious delay |

| 90+ | Default / NPA risk |

📌 Even 1 missed EMI creates a negative DPD entry.

DPD LEVELS EXPLAINED (VERY IMPORTANT)

🔹 DPD 0

Ideal status

No impact on credit score

🔹 DPD 30

EMI delayed by up to 30 days

Credit score starts dropping

🔹 DPD 60

Repeated delay

Strong negative impact

🔹 DPD 90+

Considered default

Severe damage to credit profile

📌 DPD 90+ may lead to NPA classification.

HOW DPD AFFECTS YOUR CREDIT SCORE

| DPD Pattern | Credit Score Impact |

|---|---|

| Occasional DPD 30 | Mild |

| Repeated DPD 30–60 | High |

| DPD 90+ | Very severe |

| Multiple accounts with DPD | Extremely damaging |

📌 Payment history contributes ~35% to credit score.

❌ COMMON MYTHS ABOUT DPD

❌ “Small delays don’t matter”

❌ “Once paid, DPD disappears immediately”

❌ “Only defaults affect credit score”

✅ Truth: Even short delays impact your score.

HOW LONG DPD RECORDS STAY IN CREDIT REPORT?

DPD entries stay for up to 7 years

Impact reduces over time with good repayment behavior

Older DPD hurts less than recent DPD

📌 Time + discipline improves credit health.

REAL-WORLD EXPERIENCE

“Most credit score drops we see are due to repeated DPD 30 entries, not big defaults. Consistency matters more than people realise.”

— Credit Risk Manager, Indian NBFC

HOW TO FIX DPD IN CREDIT REPORT

Step-by-Step Action Plan:

Clear all overdue EMIs immediately

Ensure current month shows DPD 0

Avoid settlements (if possible)

Set auto-debit reminders

Keep EMI-to-income ratio healthy

Monitor credit report every 3–6 months

📌 DPD cannot be erased instantly—but it can be overpowered by good history.

CAN DPD BE REMOVED FROM CREDIT REPORT?

DPD can be removed only if:

Entry is incorrect

EMI was paid on time but reported wrongly

Bank made reporting error

What to do:

Raise dispute with credit bureau

Submit payment proof

Follow up with lender

📌 Genuine delays cannot be deleted early.

🆚 DPD VS NPA (IMPORTANT DIFFERENCE)

| Factor | DPD | NPA |

|---|---|---|

| Meaning | Delay indicator | Default classification |

| Timeline | Immediate | After 90 days |

| Impact | Gradual | Severe |

| Recovery | Easier | Difficult |

🛡️ HOW TO PREVENT DPD IN FUTURE

Use auto-debit for EMIs

Keep emergency fund (3–6 EMIs)

Avoid over-borrowing

Track due dates

Don’t ignore SMS/email alerts

❓ FREQUENTLY ASKED QUESTIONS (FAQs)

1. What does DPD mean in credit report?

Days Past Due – delayed payment days.

2. Is DPD bad for credit score?

Yes, especially repeated DPD.

3. Does DPD 30 affect score?

Yes, mildly to moderately.

4. How long does DPD stay?

Up to 7 years.

5. Can DPD be removed?

Only if incorrect.

6. Is DPD same as default?

No, default is more serious.

7. Does credit card DPD matter?

Yes, equally.

8. How to check DPD?

In CIBIL or credit report.

9. Will score recover after DPD?

Yes, with time and discipline.

10. Is DPD shown monthly?

Yes.

11. Does settlement clear DPD?

No, it worsens profile.

12. Can one DPD ruin score?

No, but repeated ones can.

13. Is DPD visible to banks?

Yes.

14. Does prepayment remove DPD?

No, only improves future record.

KEY TAKEAWAYS

DPD shows delayed EMI days

Even small delays matter

DPD impacts credit score strongly

Records stay up to 7 years

Timely payments heal credit

CONCLUSION + CTA

DPD may look like just a number, but it reflects your credit discipline. Understanding and controlling DPD is one of the fastest ways to protect and rebuild your credit score.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply at www.vizzve.com

Published on : 12th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed