DPD shows EMI delay days, SMA is an early warning stage, and NPA means the loan has turned non-performing after 90+ days overdue.

AI ANSWER BOX

What is the difference between DPD, SMA and NPA?

DPD shows how many days an EMI is overdue, SMA is a bank’s early warning category for stressed loans, and NPA means the loan has defaulted after 90 days of non-payment.

INTRODUCTION

If you’ve ever checked your credit report or spoken to a bank about a delayed EMI, you may have heard confusing terms like DPD, SMA, or NPA.

For borrowers, these terms can feel intimidating — but they’re actually part of a simple loan overdue tracking system used by banks and NBFCs.

This blog explains:

What DPD, SMA and NPA really mean

How they are connected

When a missed EMI becomes serious

How they affect your credit score

How to avoid moving from DPD to NPA

Explained in plain language, with real borrower logic, not banking jargon.

WHAT IS DPD? (Days Past Due)

DPD (Days Past Due) shows:

👉 How many days your EMI payment is delayed

Common DPD values:

DPD 0 → Paid on time

DPD 1–30 → Short delay

DPD 31–60 → Moderate delay

DPD 61–90 → Serious delay

📌 DPD appears directly on your credit report.

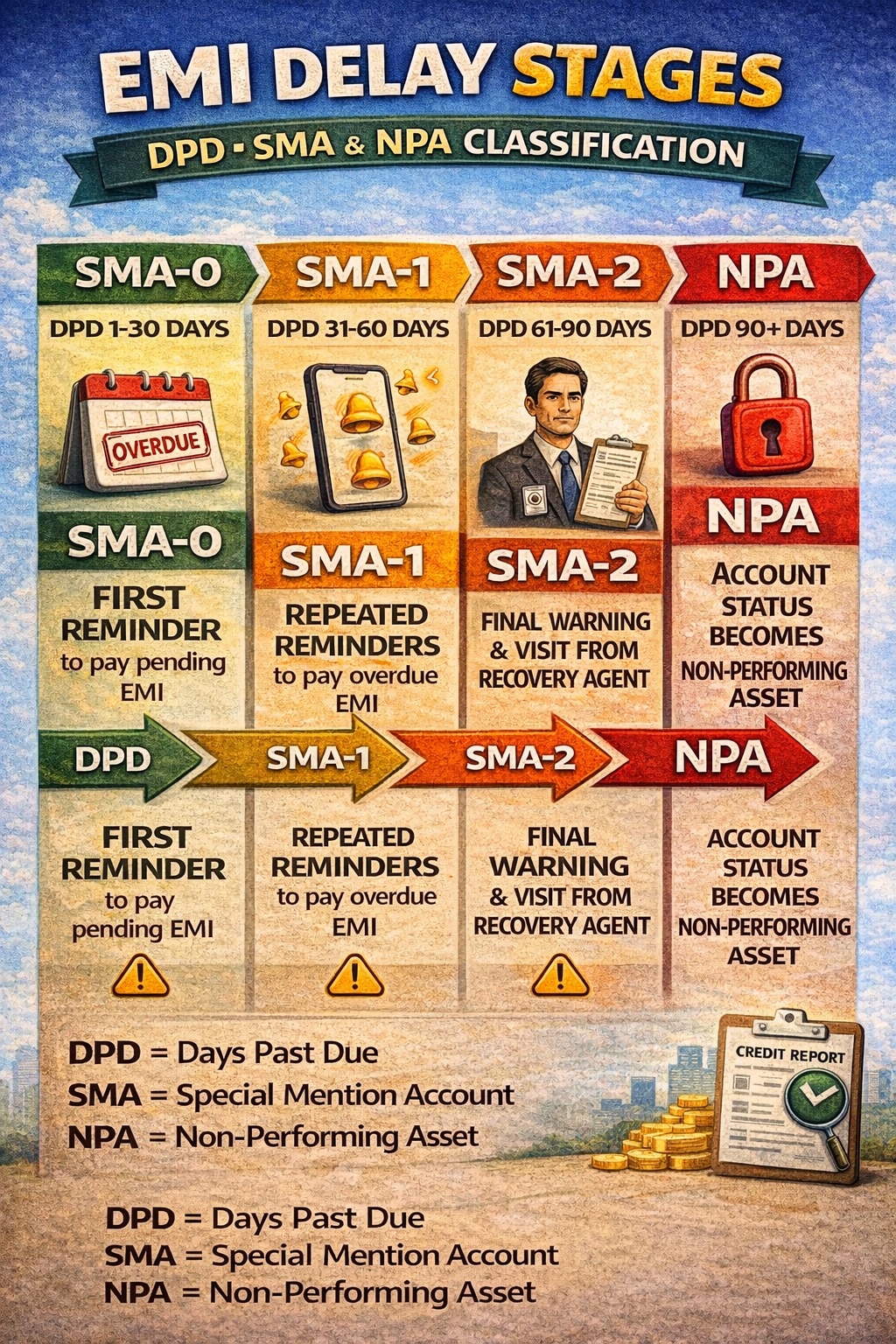

WHAT IS SMA? (Special Mention Account)

SMA is a bank’s internal early warning system for stressed loans.

It is classified as:

| SMA Type | Overdue Days |

|---|---|

| SMA-0 | 1–30 days |

| SMA-1 | 31–60 days |

| SMA-2 | 61–90 days |

📌 SMA status is used by banks, not shown directly to borrowers like DPD.

WHAT IS NPA? (Non-Performing Asset)

A loan becomes NPA when:

👉 EMI remains unpaid for more than 90 days

Once classified as NPA:

Loan is considered defaulted

Credit score drops sharply

Recovery action may start

📌 NPA is the final and most serious stage.

DPD, SMA & NPA: HOW THEY ARE CONNECTED

They represent stages of the same problem.

Simple flow:

Missed EMI → DPD increases → SMA category → NPA

DPD vs SMA vs NPA (SIMPLE COMPARISON)

| Factor | DPD | SMA | NPA |

|---|---|---|---|

| Meaning | EMI delay days | Stress warning | Loan default |

| Who uses it | Credit bureaus | Banks | Banks & RBI |

| Days overdue | 1–90 | 1–90 | 90+ |

| Credit report impact | Yes | Indirect | Severe |

| Loan approval impact | Moderate | High | Very high |

REAL-WORLD BORROWER EXAMPLE

| EMI Status | Classification | Impact |

|---|---|---|

| Paid after 10 days | DPD 10 | Minor |

| Missed 45 days | SMA-1 | Warning |

| Missed 75 days | SMA-2 | Serious |

| Missed 95 days | NPA | Default |

👉 Early action prevents long-term damage.

HOW THESE AFFECT YOUR CREDIT SCORE

DPD 1–30: Small dip (if rare)

Repeated DPD: Major impact

SMA-2: Strong negative signal

NPA: Severe damage (recovery takes years)

📌 Repayment history forms 35–40% of your credit score.

EXPERT COMMENTARY

“Most NPAs start as small DPDs. Borrowers who act early can stop long-term credit damage.”

— Senior Credit Risk Manager, Indian Bank

HOW TO STOP DPD TURNING INTO NPA

Practical borrower steps:

Pay EMIs before due date

Set auto-debit reminders

Contact lender if income drops

Request restructuring early

Avoid ignoring bank calls

📌 Communication matters more than silence.

HOW LONG DO DPD & NPA STAY ON RECORD?

DPD records: up to 7 years

NPA history: 7 years or more

Recent behaviour matters more than old mistakes

📌 Time + disciplined repayment = recovery.

❓ FREQUENTLY ASKED QUESTIONS (FAQs)

1. What is DPD?

Days Past Due for EMI delay.

2. Is DPD same as default?

No.

3. What is SMA?

Early warning loan stress category.

4. Does SMA appear in credit report?

Indirectly through DPD.

5. When does loan become NPA?

After 90 days overdue.

6. Is NPA bad for credit score?

Yes, very bad.

7. Can NPA be reversed?

Status improves only after settlement & time.

8. Does one missed EMI make NPA?

No.

9. Which is worst: DPD, SMA or NPA?

NPA.

10. Can banks restructure SMA loans?

Yes.

11. Does NPA affect future loans?

Yes.

12. How to avoid SMA?

Pay EMIs on time.

13. How long does recovery take?

2–5 years or more.

14. Should I check credit report regularly?

Yes, every 6 months.

KEY TAKEAWAYS

DPD shows EMI delay

SMA is early stress warning

NPA means loan default

Small delays can snowball

Early action protects credit health

CONCLUSION + CTA

Understanding DPD, SMA and NPA gives you control over your credit life. These are not just banking terms — they are warning signs that help you act before damage becomes permanent.

Pay on time, communicate early, and stay credit-aware.

For transparent loan support and borrower guidance, trust Vizzve Financial.

👉 Apply now at www.vizzve.com

Published on : 14th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed