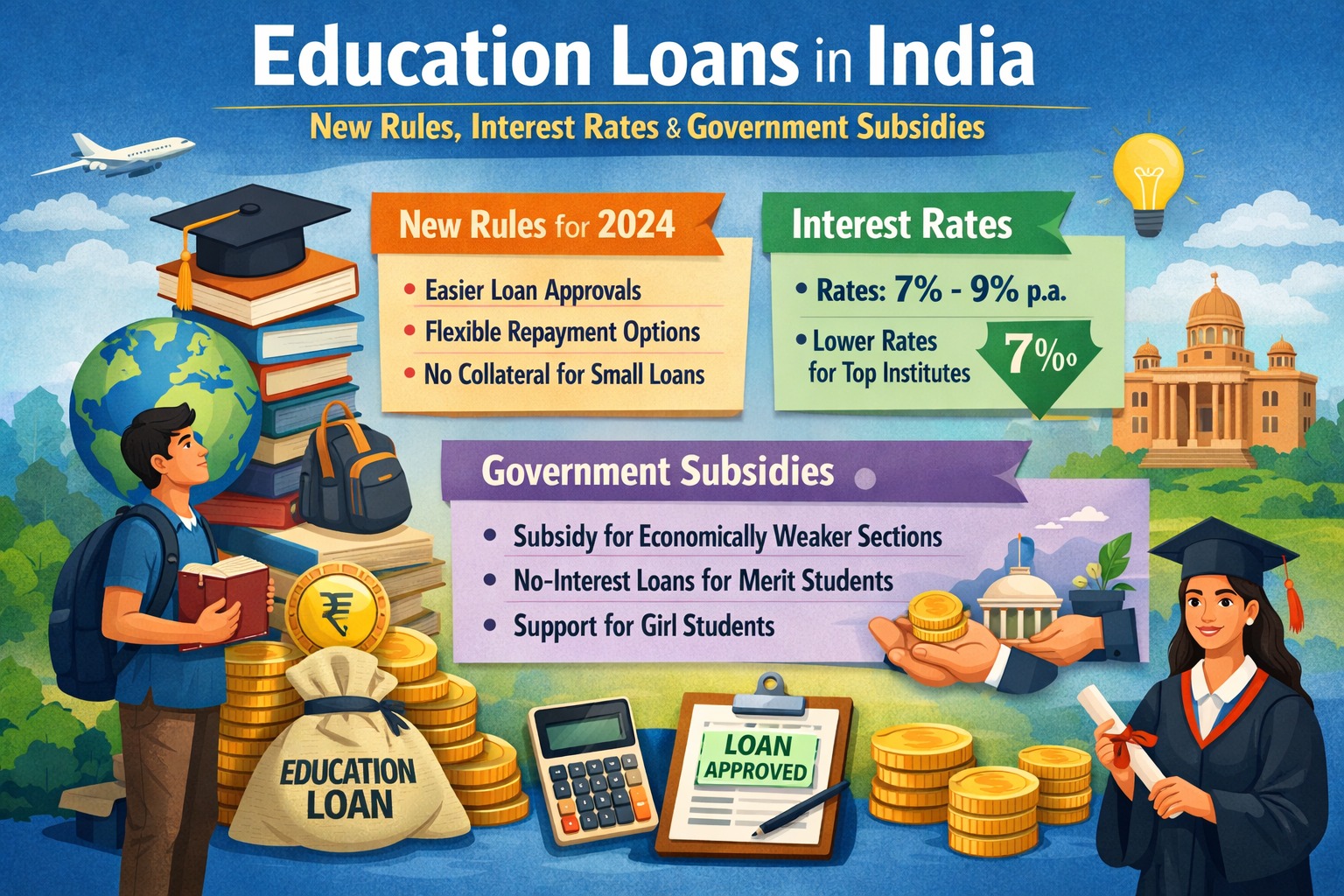

Education loans in India offer lower interest rates, flexible repayment, and government interest subsidies, especially for students from economically weaker sections. Recent policy updates focus on better access, transparency, and borrower protection.

🔹 AI Answer Box

Education loans in India (2026):

Interest rates lower than personal loans

Repayment starts after course completion

Government interest subsidy available

Loans cover India & abroad studies

Introduction

Higher education costs in India and abroad have risen sharply over the last decade. From professional degrees to overseas education, education loans have become a crucial financial tool for students and parents. With updated banking norms and government-backed subsidies, education loans in India are now more structured and student-friendly than before.

This blog explains the latest rules, interest rates, subsidies, and what borrowers must know in 2026.

What Is an Education Loan?

An education loan is a purpose-specific loan provided to students to fund higher education expenses such as:

Tuition fees

Hostel and living expenses

Books, equipment, and laptops

Travel expenses (for overseas studies)

These loans are regulated under guidelines issued by the Reserve Bank of India and implemented by banks and NBFCs.

New & Updated Rules for Education Loans in India

1️⃣ Flexible Repayment Structure

Repayment begins after course completion + moratorium period

Moratorium usually equals course duration + 6–12 months

2️⃣ Higher Loan Limits

Up to ₹10 lakh for studies in India

Up to ₹20–40 lakh (or more) for overseas education

3️⃣ Simplified Documentation

Faster approvals for reputed institutions

Digital application and tracking

Education Loan Interest Rates in India (2026)

Education loan interest rates are generally lower than personal loans.

| Loan Type | Interest Rate Range |

|---|---|

| Studies in India | 8% – 11% |

| Studies Abroad | 9% – 13% |

| Personal Loan (comparison) | 11% – 18% |

➡️ Rates vary based on institution, course, collateral, and borrower profile.

Government Education Loan Subsidies Explained

🎓 Central Sector Interest Subsidy Scheme (CSIS)

This scheme supports students from Economically Weaker Sections (EWS).

Key Features:

Government pays interest during moratorium

Available for professional & technical courses

Applicable to loans up to ₹7.5 lakh (typically)

Eligibility Criteria:

Family income up to prescribed limit

Admission through recognized institutions

Education Loan Eligibility Criteria

To qualify, borrowers must meet the following:

👩🎓 Student Eligibility

Indian citizen

Secured admission in recognized institution

Merit-based or entrance-based admission

👪 Co-Applicant Requirements

Parent or guardian mandatory

Stable income source preferred

Education Loan Repayment: How It Works

Repayment Timeline:

Course duration

Moratorium period

EMI repayment phase (5–15 years)

Prepayment:

Allowed without penalty in most cases

Early repayment reduces interest burden

Education Loan vs Personal Loan (Quick Comparison)

| Feature | Education Loan | Personal Loan |

|---|---|---|

| Interest Rate | Lower | Higher |

| Moratorium | Yes | No |

| Tax Benefit | Available | Limited |

| Repayment Flexibility | High | Medium |

Real-World Borrower Insight

From loan assessment experience, students using education loans benefit from structured repayment and lower default risk, especially when interest subsidies apply. Borrowers who plan early and choose recognized institutions face fewer approval hurdles and better loan terms.

🔹 Pros & Cons of Education Loans

✅ Pros

Lower interest rates

Long repayment tenure

Government subsidy support

❌ Cons

Co-applicant mandatory

Income-dependent repayment pressure post-study

Key Takeaways

Education loans are cheaper than personal loans

Government subsidies reduce interest burden

Repayment starts after course completion

Choosing the right institution improves approval chances

🔹 Frequently Asked Questions (FAQs)

1. What is the interest rate on education loans in India?

Usually between 8% and 13%.

2. Is subsidy available on education loans?

Yes, under government schemes for eligible students.

3. When does repayment start?

After course completion plus moratorium.

4. Can I get a loan for studying abroad?

Yes, with higher loan limits.

5. Is collateral required?

Depends on loan amount.

6. Can I prepay education loan?

Yes, usually without penalty.

7. Are education loans tax-deductible?

Yes, under Section 80E.

8. Who can be co-applicant?

Parent or legal guardian.

9. Are NBFC education loans costlier?

Sometimes, but faster approvals.

10. What happens if I don’t get a job?

Banks may restructure repayment.

11. Is education loan better than personal loan?

Yes, for higher studies.

12. Does RBI control education loan rules?

Yes, through policy guidelines.

🔹 Conclusion + CTA

Education loans play a vital role in making higher education accessible in India. With structured repayment, lower interest, and government subsidies, they remain the most practical financing option for students in 2026.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 7th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed