Introduction

MFI loans are designed to serve low-income and underserved borrowers, but they are not given without checks.

In fact, eligibility criteria for MFI loans are carefully defined to prevent over-borrowing and repayment stress. Understanding these criteria helps borrowers apply confidently, avoid rejection, and borrow responsibly.

AI Answer Box

Short Answer:

Eligibility for MFI loans depends on age, household income limits, loan purpose, repayment capacity, existing loans, and residence in eligible rural or semi-urban areas.

Who Are MFI Loans Meant For?

Microfinance Institutions focus on borrowers who:

Lack access to traditional bank credit

Work in informal or self-employed roles

Need small-ticket loans for livelihood or essential needs

MFIs operate under regulations of the Reserve Bank of India, which sets clear borrower eligibility norms.

Core Eligibility Criteria for MFI Loans

1. Age Criteria

Most MFIs require borrowers to be:

Between 18 and 60 years

(Some MFIs allow up to 65 years)

📌 Age ensures legal capacity and repayment ability.

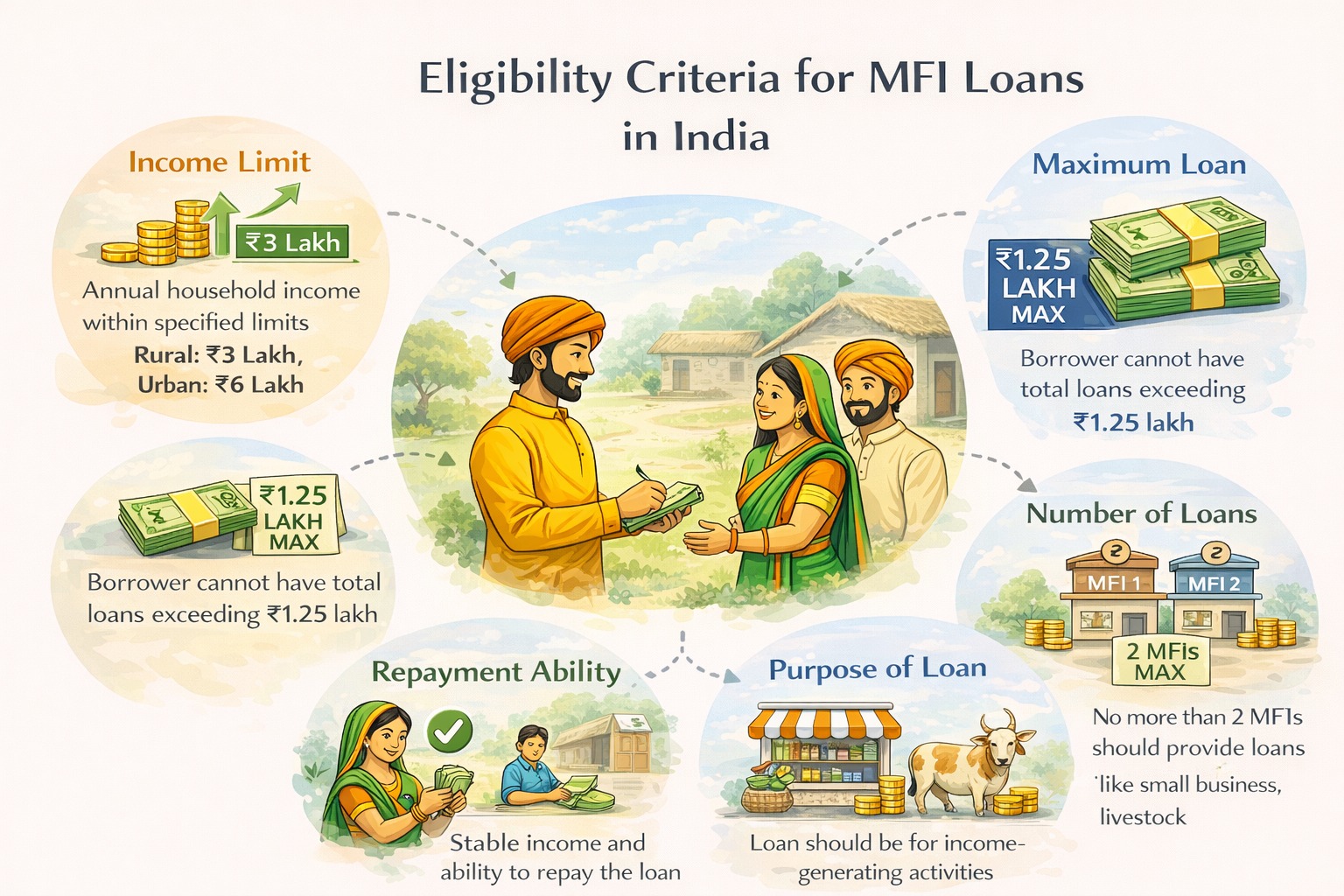

2. Household Income Limits

MFI loans are meant for low-income households.

Typical limits:

Rural areas: Up to ₹1.25–₹1.50 lakh annually

Urban/semi-urban: Up to ₹2.00 lakh annually

📌 Income limits ensure credit reaches intended segments.

3. Area of Residence

Eligible borrowers usually live in:

Rural areas

Semi-urban locations

Low-income urban pockets

MFIs often require:

Minimum stay of 6–12 months at current address

4. Purpose of Loan

MFIs strongly prefer purpose-based lending.

Accepted purposes include:

Income-generating activities

Small business or livelihood support

Education-related expenses

Essential household needs

📌 Using loans for speculative or luxury spending may lead to rejection.

5. Existing Loans & Loan Limits

MFIs closely track:

Number of active loans

Total outstanding loan amount

Typical norms:

No more than 2–3 active MFI loans

Household loan cap as per RBI norms

📌 This prevents loan stacking.

6. Repayment Capacity (Cash Flow Check)

Even without formal income proof, MFIs assess:

Daily or weekly income patterns

Household expenses

Ability to meet weekly EMIs

This is done via:

Field visits

Group discussions

Community references

7. Credit History (If Available)

While many MFI borrowers are first-time borrowers:

Credit bureau checks are increasingly common

Past defaults may affect eligibility

📌 Credit score is not mandatory, but behaviour matters.

Documentation Required for MFI Loans

MFIs keep documentation simple and accessible.

Common Documents

Aadhaar card

Address proof

Passport-size photographs

Basic household details

📌 No salary slips or ITRs required in most cases.

Group vs Individual Loan Eligibility

| Aspect | Group Loans | Individual Loans |

|---|---|---|

| Guarantee | Group responsibility | Individual |

| Eligibility Strictness | Moderate | Higher |

| Loan Size | Smaller | Slightly higher |

| Risk Sharing | Shared | Individual |

Common Reasons MFI Loan Applications Get Rejected

Income above eligibility limits

Too many existing loans

Weak repayment capacity

Mismatch in stated loan purpose

Incorrect or incomplete information

How Borrowers Can Improve Eligibility

Practical Tips

Avoid multiple simultaneous loans

Repay existing loans on time

Choose realistic loan amounts

Be transparent during field checks

Use loans for stated purposes only

Real-World Insight

From field-level microfinance operations, borrowers with stable cash flow and honest disclosure have far higher approval and repayment success than those overstretching eligibility.

MFIs prioritise sustainability over speed.

Eligibility Snapshot (Quick View)

| Criteria | Requirement |

|---|---|

| Age | 18–60 years |

| Income | Within RBI limits |

| Area | Rural / Semi-Urban |

| Loan Purpose | Productive / Essential |

| Existing Loans | Limited |

| Repayment Ability | Mandatory |

Key Takeaways

MFI loans target low-income households

Eligibility is purpose- and cash-flow-driven

Income limits and loan caps matter

Documentation is simple but verification is strict

Responsible borrowing improves long-term access

Frequently Asked Questions

1. Who is eligible for MFI loans?

Low-income rural or semi-urban borrowers.

2. Is income proof required?

Usually no formal proof.

3. Is credit score mandatory?

No, but repayment history matters.

4. Can salaried people apply?

Rarely, unless income is informal.

5. What is loan stacking?

Taking multiple loans simultaneously.

6. Are women preferred borrowers?

Yes, in many MFIs.

7. Is collateral required?

No, MFI loans are unsecured.

8. Can first-time borrowers apply?

Yes, MFIs specialise in first-time borrowers.

9. Are group loans compulsory?

Not always.

10. Can urban borrowers apply?

Yes, if income criteria match.

11. Do MFIs verify residence?

Yes, through field checks.

12. Can eligibility improve over time?

Yes, with good repayment behaviour.

Conclusion: Eligibility Protects Borrowers Too

MFI eligibility criteria are not barriers—they are safeguards.

By ensuring loans go to the right borrowers at the right size, MFIs help prevent debt traps and support sustainable livelihoods. Understanding these rules empowers borrowers to borrow smarter and grow steadily.

Published on : 26th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed