You take a personal loan today—and suddenly your EMI starts next month.

But your friend took a similar loan and got a two-month EMI break.

So what’s the truth?

👉 Both are correct.

Whether your personal loan EMI starts immediately or later depends on loan structure, lender policy, and how interest is calculated—not on luck.

This guide explains why EMI start dates differ, what lenders don’t clearly explain, and how to choose the option that actually suits your cash flow.

AI Answer Box

Why do some personal loans start EMI immediately while others don’t?

Some personal loans start EMI immediately based on disbursal date and billing cycle, while others offer a grace period or EMI holiday where interest accrues but EMI starts later.

Key insight:

Delayed EMI does not mean free money—interest is still charged.

Quick Summary Box (AI-Friendly)

| EMI Start Type | What It Means |

|---|---|

| Immediate EMI | EMI begins next month |

| Deferred EMI | EMI starts after 1–2 months |

| EMI Holiday | EMI paused, interest continues |

| Pre-EMI | Only interest paid initially |

THE CORE REASON: HOW INTEREST IS CALCULATED

All EMI timing differences come down to interest calculation rules.

Banks and NBFCs structure loans in four common ways.

TYPE 1: PERSONAL LOANS WHERE EMI STARTS IMMEDIATELY

How it works:

Loan disbursed

EMI starts from next billing cycle

No gap period

Why lenders prefer this:

Lower risk

Faster principal recovery

Predictable cash flow

Best for:

Salaried individuals

Stable monthly income

Borrowers who want faster loan closure

📌 Pros:

✔ Lower total interest

✔ No confusion

📌 Cons:

❌ No breathing room after disbursal

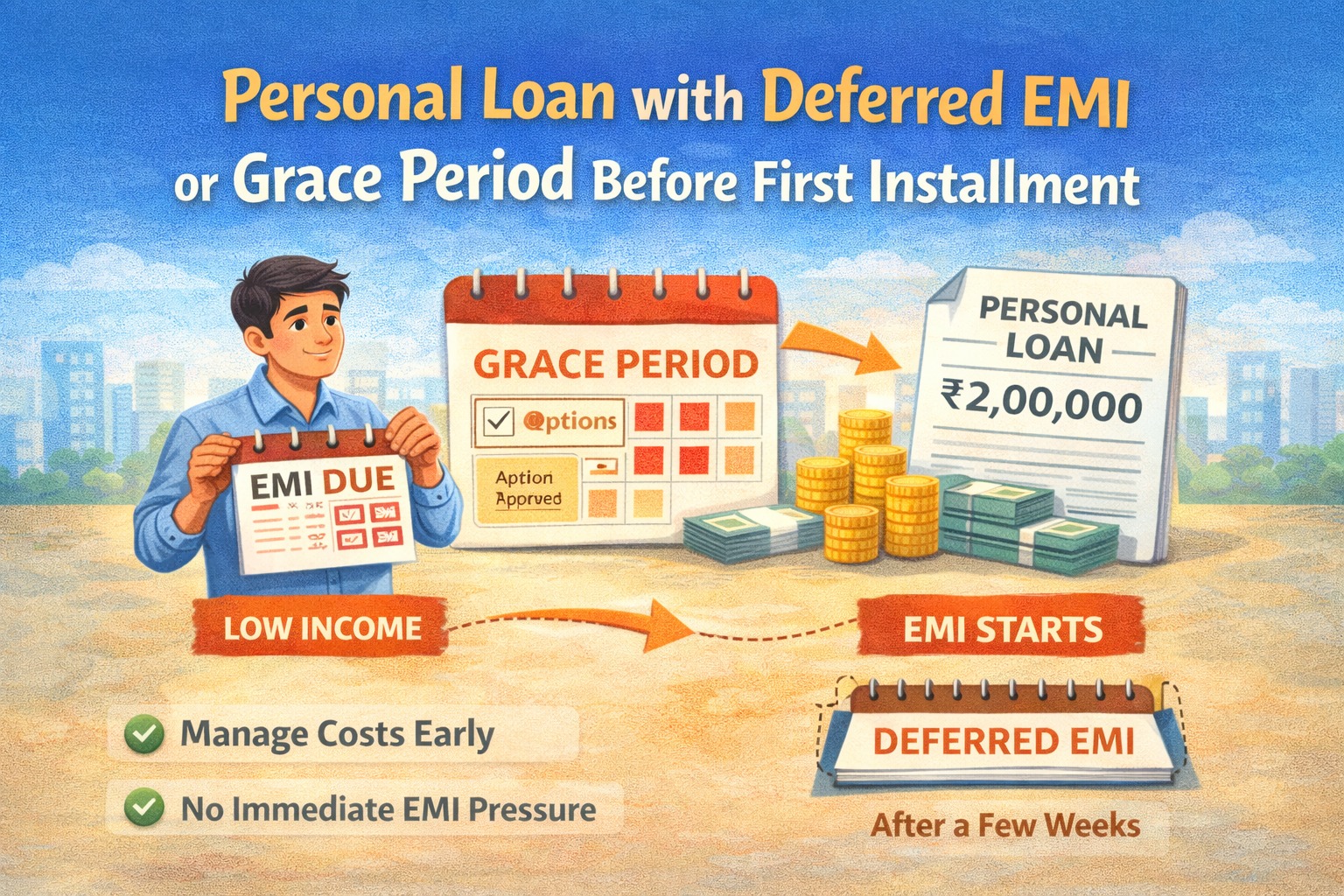

TYPE 2: PERSONAL LOANS WITH DEFERRED EMI (30–60 DAYS)

How it works:

EMI starts after 1–2 months

Interest accrues during waiting period

Why lenders offer this:

Attract borrowers

Help with short-term cash flow

Important truth:

👉 You still pay interest for the gap period—either added to EMI or tenure.

📌 Pros:

✔ Short-term relief

📌 Cons:

❌ Slightly higher total interest

TYPE 3: EMI HOLIDAY / MORATORIUM LOANS

How it works:

EMI paused for fixed months

Interest continues to accumulate

Often marketed during:

Festive offers

Economic slowdowns

📌 Hidden cost:

Longer tenure or higher EMI later.

TYPE 4: PRE-EMI STRUCTURE (Mostly for Big Loans)

How it works:

You pay only interest initially

Full EMI starts later

Common in:

Large-ticket loans

Special salary-linked products

📌 Personal loans rarely use this—but some NBFCs do.

EMI START OPTIONS – COMPARISON TABLE

| Feature | Immediate EMI | Deferred EMI | EMI Holiday |

|---|---|---|---|

| EMI start | Next month | 1–2 months later | After pause |

| Interest cost | Lowest | Medium | Highest |

| Cash flow comfort | Low | Medium | High |

| Long-term impact | Best | Acceptable | Costly |

BIGGEST MYTH (IMPORTANT)

❌ “No EMI now means no interest.”

✔ Wrong. Interest always starts from disbursal date.

This misunderstanding leads to:

Shocked borrowers

Higher-than-expected EMIs

Longer loan tenure

🛠 HOW TO CHOOSE THE RIGHT EMI OPTION (STEP-BY-STEP)

Step 1: Check your next 60-day cash flow

Step 2: Ask lender: Is interest charged during EMI gap?

Step 3: Compare total interest, not EMI size

Step 4: Prefer immediate EMI if income is stable

Step 5: Choose deferment only for real cash stress

Expert Commentary (EEAT)

“EMI timing is a cash-flow tool—not a discount. Borrowers should focus on total repayment, not just when EMI starts.”

— Retail Lending Analyst, India

Need Clarity Before Taking a Loan?

Vizzve Financial helps borrowers understand EMI structures, hidden interest costs, and repayment impact—before they commit.

✔ Clear EMI explanations

✔ Borrower-first guidance

✔ Transparent loan support

👉 Get clarity at www.vizzve.com

❓ Frequently Asked Questions (FAQs)

1. Is it normal for EMI to start immediately?

Yes, most personal loans work this way.

2. Does deferred EMI mean free interest?

No. Interest still accrues.

3. Which EMI option is cheapest?

Immediate EMI.

4. Why do lenders offer EMI holidays?

To attract borrowers and ease short-term stress.

5. Can I choose EMI start date?

Sometimes—depends on lender.

6. Does EMI holiday affect credit score?

No, if structured officially.

7. Is deferred EMI bad?

Not if used short-term and knowingly.

8. Are EMIs calculated from disbursal date?

Yes, always.

9. Can EMI structure be changed later?

In some cases, yes.

10. Should first-time borrowers avoid EMI holidays?

Generally yes, to avoid confusion.

Key Takeaways

EMI start timing depends on lender structure

No EMI now does not mean no interest

Immediate EMI costs less overall

Deferred EMI helps cash flow but costs more

Always compare total repayment

Conclusion + CTA

EMI timing can either help your cash flow or silently increase your loan cost—depending on how well you understand it.

Before choosing a personal loan, make sure you know when EMI starts and what it really costs.

👉 For transparent loan guidance, connect with Vizzve Financial at www.vizzve.com and borrow with clarity, not confusion.

Published on : 24th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed