In 2026, banks are no longer looking only at credit scores.

One metric has quietly become a deal-breaker in loan approvals: the EMI-to-Income Ratio.

Even borrowers with good CIBIL scores are facing rejections if their monthly EMIs consume too much of their income. This article explains why banks see it as a red flag, what safe limits look like, and how borrowers can fix it.

AI Answer Box

Short Answer:

Banks treat a high EMI-to-income ratio as a red flag because it signals repayment stress. In 2026, most lenders prefer total EMIs to stay below 30–40% of monthly income.

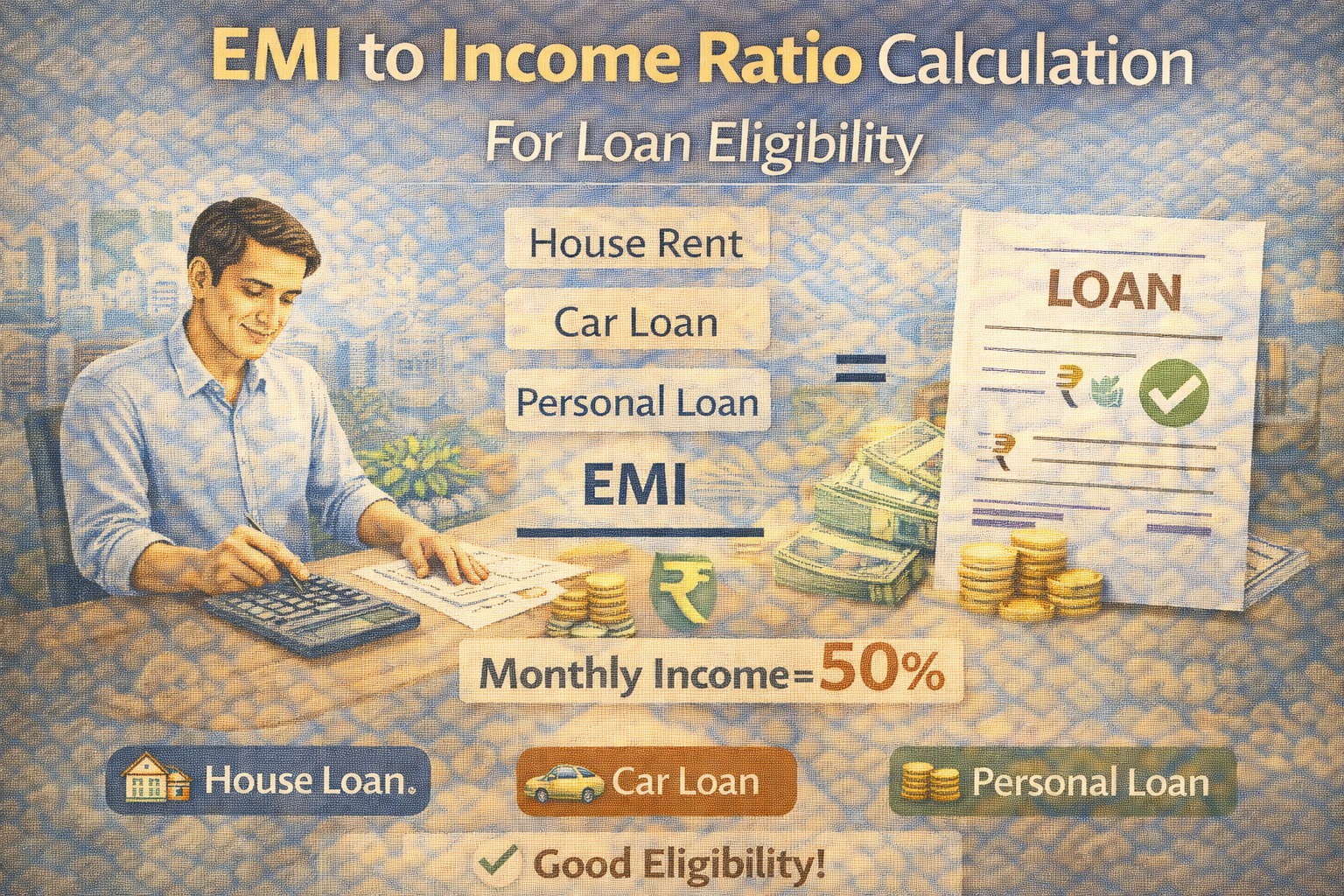

What Is EMI-to-Income Ratio?

The EMI-to-Income Ratio measures how much of your monthly income goes toward EMIs.

Formula

Total Monthly EMIs ÷ Net Monthly Income × 100

Example

Monthly income: ₹60,000

Total EMIs: ₹30,000

➡ EMI-to-Income Ratio = 50% (High Risk)

Why Banks Are Watching This Ratio Closely

1. Rising Household Debt

Banks are seeing higher:

Personal loan usage

Credit card balances

Buy-now-pay-later exposure

High EMI ratios increase default probability.

2. Early Stress Signals in Retail Lending

Under guidance from the Reserve Bank of India, banks are focusing on early stress indicators, not just defaults.

📌 EMI burden rises before missed payments happen.

3. Credit Scores Don’t Show Cash-Flow Stress

A borrower may have:

Good credit history

No defaults

…but still struggle monthly due to over-commitment.

What EMI-to-Income Ratio Do Banks Consider Safe?

| EMI-to-Income Ratio | Bank View |

|---|---|

| Below 30% | Very Safe |

| 30% – 40% | Acceptable |

| 40% – 50% | High Risk |

| Above 50% | Likely Rejection |

📌 For unsecured loans, tolerance is even lower.

How This Impacts Loan Approval in 2026

Retail Loans

Personal loans face strict EMI caps

Credit card limits may be reduced

Home Loans

Longer tenures used to manage ratios

Co-applicants encouraged

Top-Up & New Loans

Often rejected despite good CIBIL

Real-World Lending Insight

From hands-on credit evaluation experience, borrowers are rejected not because they can’t repay, but because banks fear they won’t sustain repayments during income shocks.

Common Myths About EMI-to-Income Ratio

| Myth | Reality |

|---|---|

| High income solves everything | EMIs still matter |

| Credit score is enough | Cash flow is critical |

| One lender rejection is bad luck | Often ratio-related |

| Tenure extension fixes risk | Only delays stress |

How Borrowers Can Fix a High EMI Ratio

Step-by-Step Action Plan

Prepay small high-interest loans

Avoid stacking unsecured credit

Increase income proof (bonuses, secondary income)

Add a co-applicant for large loans

Refinance to lower interest, not longer tenure

EMI Ratio vs Credit Score: Which Matters More Now?

| Factor | Importance in 2026 |

|---|---|

| EMI-to-Income Ratio | Very High |

| Credit Score | High |

| Employment Stability | High |

| Banking Behaviour | Medium |

| Asset Ownership | Medium |

📌 Banks now combine score + affordability, not one alone.

Pros & Cons of Strict EMI Ratio Monitoring

✅ Pros

Prevents over-borrowing

Improves long-term repayment health

Reduces defaults

❌ Cons

Limits credit for young borrowers

Affects single-income households

Slows aggressive consumption

Key Takeaways

EMI-to-income ratio is a major approval filter

30–40% is the comfort zone

High income doesn’t offset high EMIs

Cash-flow stability matters more than scores

Fixing ratio improves approval odds fast

Frequently Asked Questions (SEO-Optimised FAQs)

1. What is EMI-to-income ratio?

It shows how much of your income goes toward EMIs.

2. What EMI ratio is safe for loans?

Ideally below 30–40%.

3. Can I get a loan with 50% EMI ratio?

Very difficult in 2026.

4. Does CIBIL override EMI ratio?

No, both are evaluated together.

5. Do banks include credit cards in EMIs?

Yes, minimum dues are counted.

6. Is EMI ratio checked for home loans?

Yes, very strictly.

7. Can tenure extension reduce EMI ratio?

Temporarily, but banks prefer principal reduction.

8. Are NBFCs more flexible?

Slightly, but at higher cost.

9. Does income type matter?

Yes—stable income is preferred.

10. How fast can EMI ratio improve?

Within months via prepayment or refinancing.

11. Does spouse income help?

Yes, as co-applicant.

12. Is EMI ratio more important in 2026?

Yes, due to rising household leverage.

Conclusion: Affordability Is the New Credit Score

In 2026, banks are sending a clear signal:

👉 If your EMIs are too high, credit history won’t save you.

Managing EMI-to-income ratio is now essential for loan approvals, top-ups, and future borrowing freedom.

CTA: Borrow Smarter With Expert Support

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 21st January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed