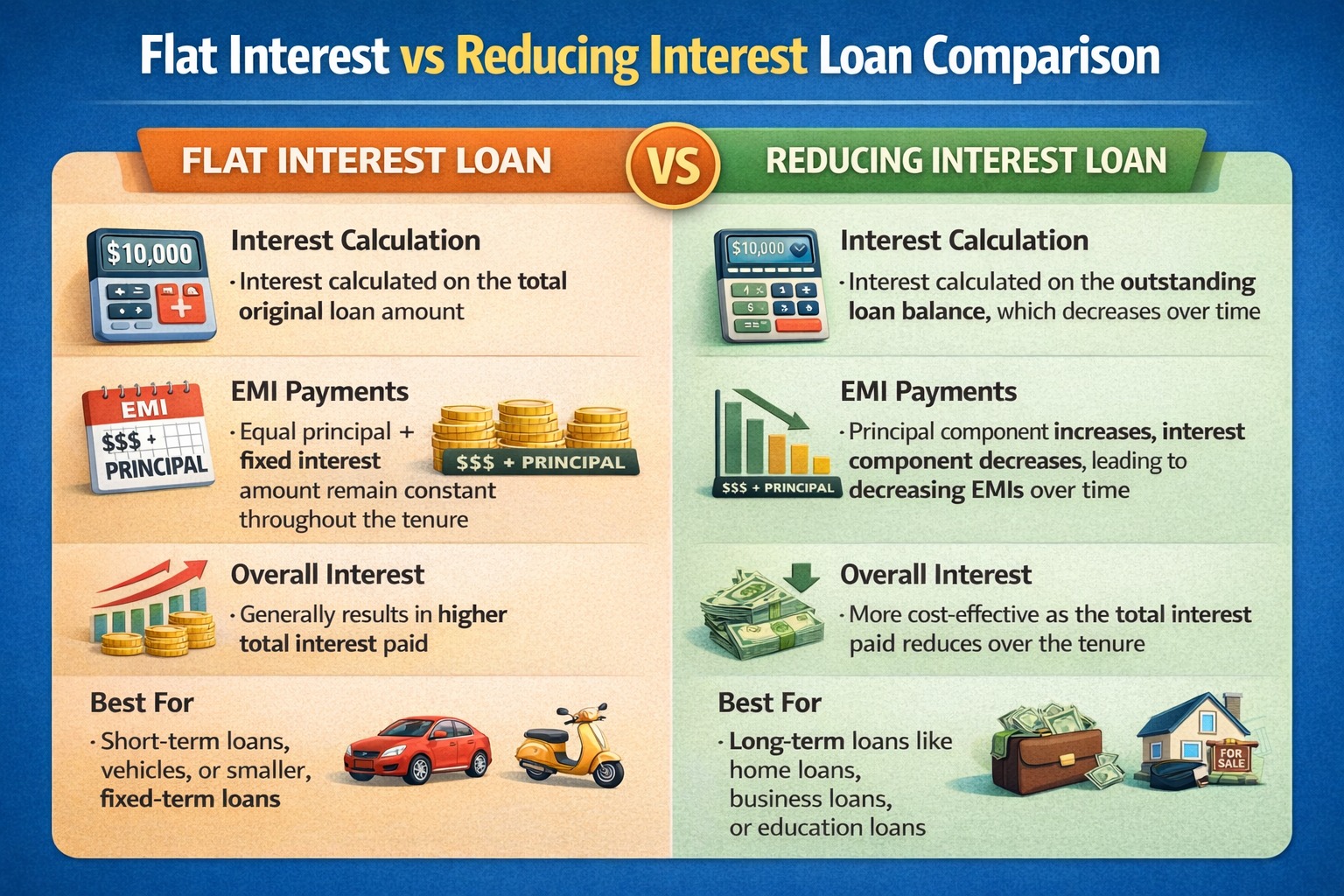

Flat interest is calculated on the full loan amount for the entire tenure, while reducing interest is calculated on the outstanding balance—making reducing-rate loans significantly cheaper over time.

AI Answer Box

Flat interest loans calculate interest on the original principal throughout the loan tenure, while reducing balance loans calculate interest on the remaining principal. Reducing interest loans usually cost much less, even if the EMI appears similar.

Why This Difference Matters More Than You Think

Many borrowers choose loans based only on:

EMI amount

Advertised interest rate

But how interest is calculated can change your total repayment by thousands or even lakhs.

What Is Flat Interest Rate?

In a flat interest loan:

Interest is calculated on the entire loan amount

Interest remains constant throughout the tenure

EMI looks simple and predictable

Flat Interest Formula (Simple)

Interest = Principal × Rate × Time

Even when you repay the loan, interest does not reduce.

What Is Reducing Interest Rate?

In a reducing (diminishing) balance loan:

Interest is calculated on the outstanding principal

As you repay principal, interest reduces

EMI impact feels lighter over time

This is also called:

Diminishing balance

Reducing balance method

Flat vs Reducing Interest: Side-by-Side Comparison

Example: ₹1,00,000 Loan for 2 Years at 12%

| Feature | Flat Interest | Reducing Interest |

|---|---|---|

| Interest calculation | On full ₹1,00,000 | On remaining balance |

| Total interest | Higher | Lower |

| EMI appearance | Looks cheaper | Looks slightly higher |

| Actual loan cost | Much higher | Much lower |

| Borrower-friendly | ❌ | ✅ |

👉 Reality: Flat rate loans can cost 20–30% more overall.

The “Hidden” Part Borrowers Miss

A 12% flat rate can actually be equal to 22–24% reducing rate in real terms.

This is why:

Flat-rate loans feel attractive

Marketing focuses on EMI, not total cost

Loans That Commonly Use Flat Interest

Flat interest is often seen in:

Personal loans from small lenders

Consumer durable loans

Some NBFC short-term loans

Quick approval loans

Reducing balance is common in:

Home loans

Car loans

Bank personal loans

Expert Insight

“Flat interest rates are easy to sell but expensive to repay. Borrowers who understand reducing balance loans save significantly over the loan tenure.”

— Retail Lending & Credit Expert

How to Choose the Right Interest Type

Smart Borrower Checklist:

Ask how interest is calculated

Compare total repayment, not EMI

Use EMI calculators for both methods

Prefer reducing balance wherever possible

Avoid flat-rate loans for long tenures

When Flat Interest Might Still Be Acceptable

Flat interest may work if:

Loan tenure is very short

Amount is small

No prepayment allowed anyway

But even then, reducing balance is usually better.

Key Takeaways

Flat interest is calculated on full principal

Reducing interest drops as you repay

Flat loans look cheaper but cost more

EMI alone is misleading

Always check total loan cost

Conclusion

Flat and reducing interest rates are not the same, even if the EMI looks similar. Understanding this hidden difference can save you a lot of money and stress. Smart borrowers always ask how interest is calculated, not just how much EMI they will pay.

❓ Frequently Asked Questions (FAQs)

1. Which is better: flat or reducing interest?

Reducing interest is almost always cheaper.

2. Why do lenders offer flat interest loans?

They are easier to explain and more profitable.

3. Does flat interest mean lower EMI?

It may look lower, but total repayment is higher.

4. Can I convert flat interest to reducing?

Usually no, unless refinancing is allowed.

5. Are flat interest loans bad?

Not bad, but more expensive.

6. Do banks use flat interest?

Most banks prefer reducing balance methods.

7. How can I spot a flat interest loan?

Check the interest calculation clause.

8. Is prepayment useful in flat interest loans?

Less effective, as interest is fixed.

9. Why does EMI feel lighter later in reducing loans?

Because interest reduces with principal repayment.

10. Should I avoid flat loans for long tenure?

Yes, always.

Published on : 15th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed