India offers multiple financing options in 2026: traditional bank loans, NBFC credit, fintech lending, microfinance, and government-backed welfare credit schemes aimed at financial inclusion.

AI Answer Box

Financing in India ranges from commercial bank loans and NBFC lending to government welfare schemes like MSME credit programs and rural finance initiatives. Borrowers can choose based on income level, credit score, business needs, and eligibility for government subsidies.

1️⃣ Traditional Bank Loans

Banks remain the largest source of credit in India.

Types:

• Home Loans

• Personal Loans

• Auto Loans

• Business Loans

• Education Loans

Pros:

✔ Lower interest rates (compared to informal lending)

✔ Longer tenure options

✔ Regulated system

Cons:

❌ Strict documentation

❌ Credit score required

All banks operate under the supervision of the

Reserve Bank of India

2️⃣ NBFC & Fintech Lending

Non-Banking Financial Companies (NBFCs) and digital apps offer:

• Quick personal loans

• Consumer durable finance

• MSME loans

• Small ticket loans

Why popular?

✔ Fast approval

✔ Less paperwork

✔ Suitable for new borrowers

However, interest rates may be higher.

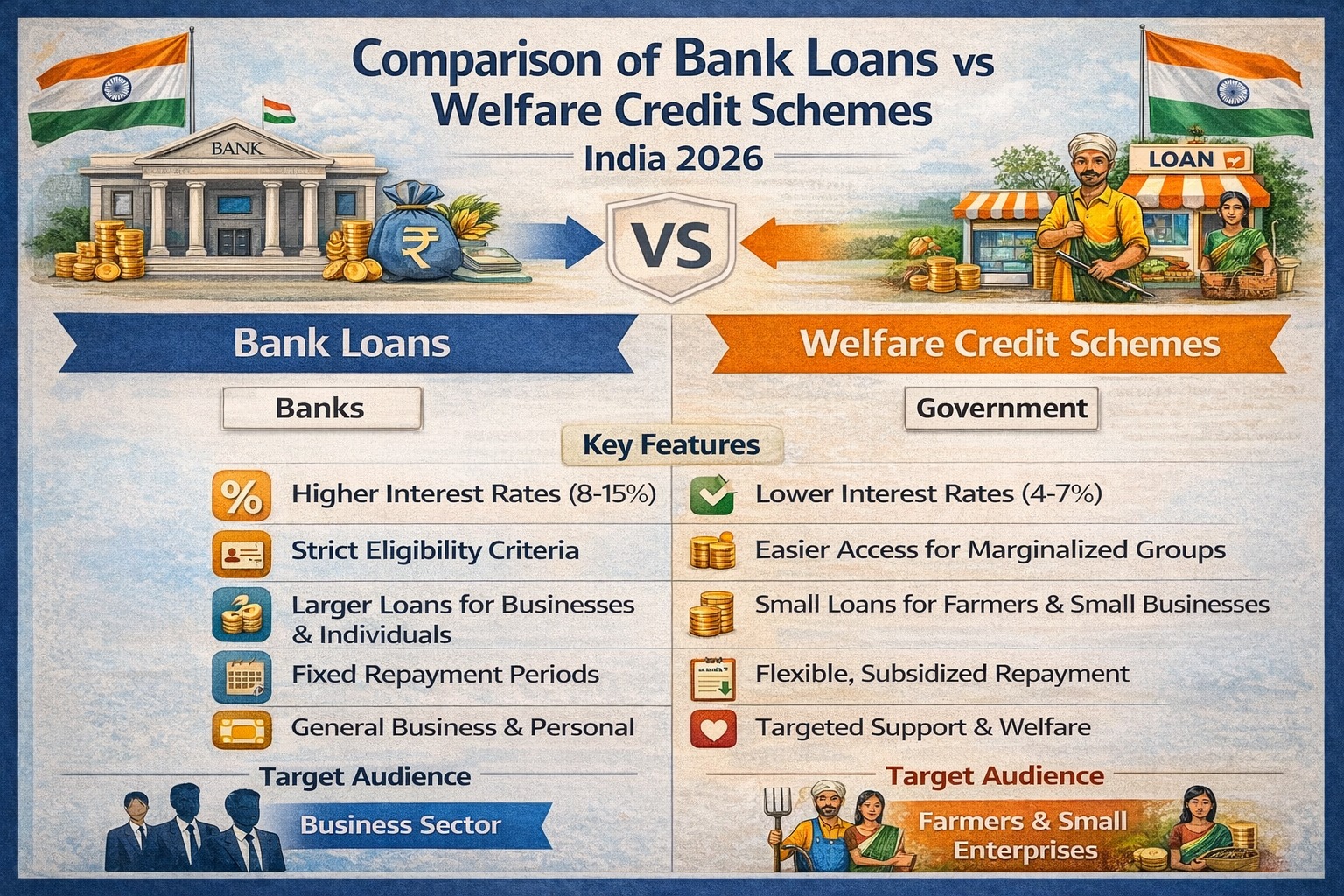

3️⃣ Government Welfare Credit Schemes

India promotes financial inclusion via schemes like:

Pradhan Mantri Mudra Yojana (MSME loans up to small amounts)

Pradhan Mantri Jan Dhan Yojana (basic banking access)

These focus on:

✔ Small entrepreneurs

✔ Rural borrowers

✔ Women-led businesses

✔ First-time borrowers

4️⃣ Microfinance & Self-Help Groups

Microfinance institutions provide:

• Small collateral-free loans

• Rural lending

• Women empowerment credit

Often used in villages and semi-urban areas.

5️⃣ Digital Credit & App-Based Lending

Digital lending platforms now assess:

• Bank transaction history

• UPI payments

• Alternative data

Faster approval, but borrowers must verify platform authenticity.

Comparison of Financing Options

| Option | Best For | Interest Rate | Speed | Documentation |

|---|---|---|---|---|

| Bank Loans | Salaried/Business | Low–Moderate | Moderate | High |

| NBFC Loans | Quick cash | Moderate–High | Fast | Medium |

| Govt Schemes | MSME/Rural | Subsidized | Moderate | Medium |

| Microfinance | Low-income | Moderate | Moderate | Low |

| Digital Apps | Small loans | High | Very Fast | Low |

How to Choose the Right Financing Option

Step 1: Check Credit Score

Higher score → cheaper loans.

Step 2: Compare Interest Rates

Don’t rush into quick but costly credit.

Step 3: Check Eligibility for Govt Schemes

Subsidized loans save money.

Step 4: Evaluate Repayment Capacity

Avoid over-borrowing.

Expert Insight

“India’s financing ecosystem in 2026 reflects a blend of formal banking strength and expanding financial inclusion efforts. The key is matching credit type to borrower profile.”

— Indian Financial Policy Analyst

Summary Box

✔ Multiple financing options available

✔ Banks offer stability

✔ NBFCs offer speed

✔ Govt schemes support inclusion

✔ Digital lending expanding

Key Takeaways

• India has diversified credit ecosystem

• Welfare credit supports low-income groups

• Banks remain primary lenders

• Fintech reshaping accessibility

• Smart borrowing ensures financial stability

❓ FAQs

1. What are financing options in India in 2026?

Banks, NBFCs, fintech apps, government schemes, and microfinance.

2. Are government loan schemes cheaper?

Often subsidized for eligible groups.

3. Who qualifies for Mudra loans?

Small business owners and entrepreneurs.

4. Are NBFC loans safe?

Yes if RBI-registered.

5. Can low-income individuals get loans?

Yes via microfinance or welfare schemes.

6. Do digital loans require credit score?

Some use alternative data.

7. What is safest financing option?

Regulated bank loans.

8. Is welfare credit permanent?

Depends on policy.

9. Can I combine multiple loans?

Possible but manage risk carefully.

10. Best way to choose financing?

Compare cost, eligibility, and repayment ability.

Conclusion

India’s financing landscape in 2026 is broader than ever — from structured bank loans to inclusive welfare credit programs.

Choosing wisely means:

✔ Understanding eligibility

✔ Comparing cost

✔ Planning repayment

Financial inclusion and digital innovation are reshaping how India borrows and grows.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 1st March

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed