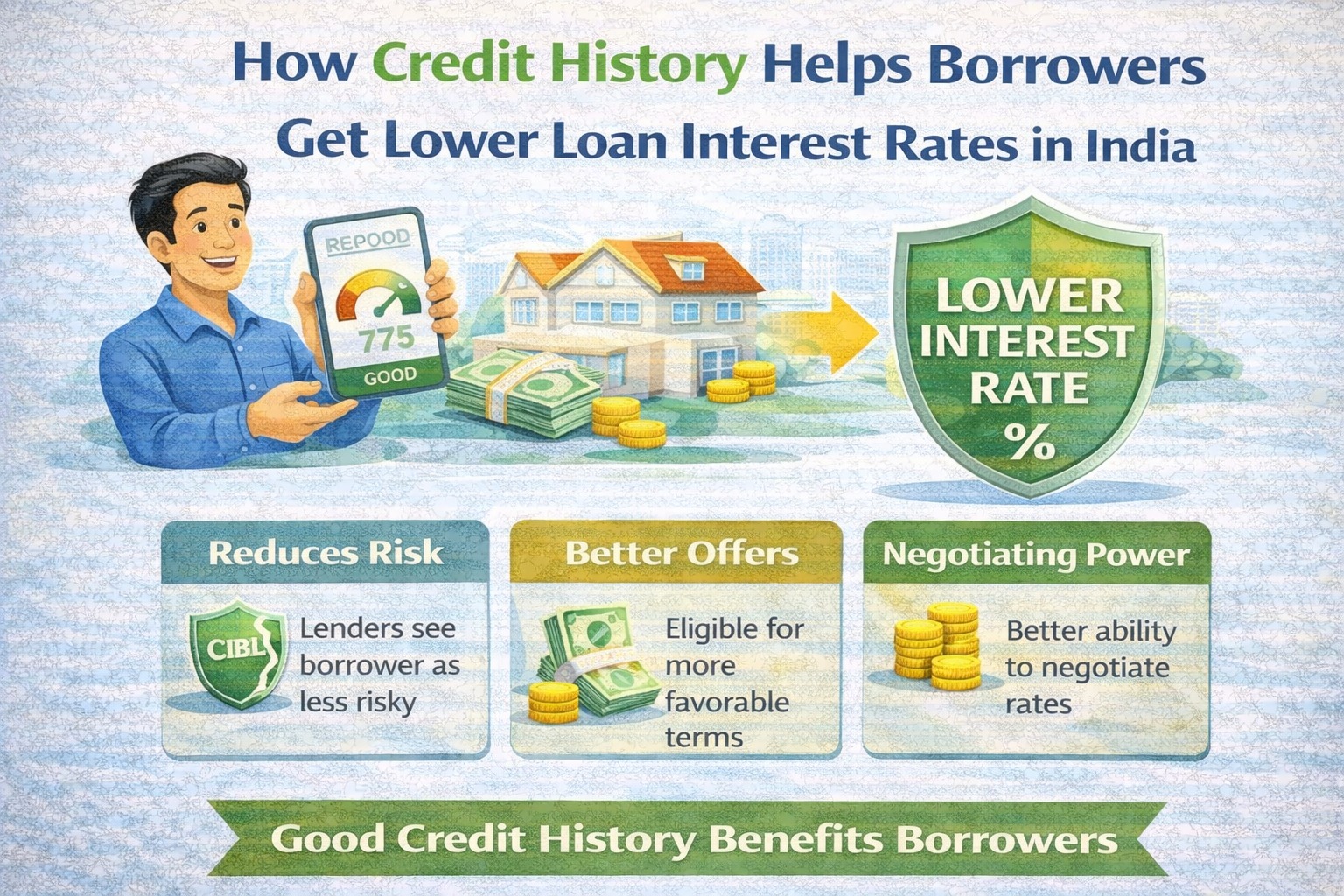

A strong credit history helps you get lower interest rates because it proves reliable repayment behaviour.

Banks reward low-risk borrowers with better pricing, faster approval, and flexible terms.

AI ANSWER BOX

How does credit history help get lower interest rates?

Credit history shows how responsibly a borrower has repaid loans in the past. A clean, long credit history signals low risk, allowing lenders to offer lower interest rates.

INTRODUCTION

Many borrowers think loan interest rates depend only on bank policies or RBI rates. In reality, your credit history plays a major role in deciding how expensive or affordable your loan will be.

Two people applying for the same loan from the same bank can receive very different interest rates—simply because their credit histories differ.

This blog explains:

What credit history really means

How lenders use it to price loans

Why good history gets lower rates

Real examples of rate difference

How to build credit history smartly

Written with lender-side insight and real borrower experience, this guide helps you borrow at the lowest possible cost.

WHAT IS CREDIT HISTORY?

Credit history is a detailed record of how you’ve handled credit over time, including:

Loan repayments

Credit card usage

EMI delays or defaults

Loan closures and settlements

📌 It is different from credit score:

Credit history = behaviour over time

Credit score = numerical summary of that behaviour

HOW BANKS USE CREDIT HISTORY TO DECIDE INTEREST RATES

Banks follow risk-based pricing.

Simple logic:

Lower risk borrower → lower interest rate

Higher risk borrower → higher interest rate

📌 Credit history is the biggest indicator of risk.

CREDIT HISTORY & INTEREST RATE RELATIONSHIP

| Credit Profile | Typical Interest Rate Impact |

|---|---|

| Long, clean history | Lowest rates |

| Minor past delays | Slightly higher |

| Recent DPD/default | High rates |

| Settlement / write-off | Very high or rejection |

📌 Even a 1–2% difference in rate can mean lakhs over time.

REAL-WORLD EXAMPLE (INTEREST SAVING)

Home Loan Example

| Borrower | Credit Score | Interest Rate |

|---|---|---|

| Borrower A | 790 | 8.45% |

| Borrower B | 650 | 9.75% |

Loan amount: ₹40 lakh | Tenure: 20 years

👉 Borrower B pays ₹6–8 lakh more in interest over the tenure.

WHAT PARTS OF CREDIT HISTORY MATTER MOST?

🔹 1. Repayment Discipline

On-time EMIs = biggest positive signal

🔹 2. Length of Credit History

Older accounts = more trust

🔹 3. Credit Utilisation

Below 30% usage preferred

🔹 4. Type of Credit

Mix of secured + unsecured is healthy

🔹 5. Recent Behaviour

Recent delays hurt more than old ones

❌ COMMON MYTHS ABOUT CREDIT HISTORY & INTEREST RATES

❌ “Only income decides interest rate”

❌ “Same bank gives same rate to everyone”

❌ “Old defaults don’t matter”

✅ Truth: Credit history heavily influences pricing.

HOW POOR CREDIT HISTORY INCREASES INTEREST COST

Borrowers with weak history often face:

Higher base interest

Additional risk premium

Stricter loan terms

Lower negotiation power

📌 Lenders price uncertainty, not just money.

EXPERT COMMENTARY

“Interest rate is the price of trust. Borrowers with consistent credit history are rewarded with the best pricing.”

— Retail Lending Risk Head, India

HOW TO BUILD CREDIT HISTORY FOR LOWER RATES

Practical steps:

Pay EMIs before due date

Avoid loan settlements

Keep credit cards active but controlled

Don’t close old credit lines unnecessarily

Monitor credit report regularly

📌 Consistency over time beats shortcuts.

HOW LONG DOES IT TAKE TO SEE INTEREST RATE BENEFIT?

6–12 months: noticeable score improvement

12–24 months: better loan offers

3+ years: premium borrower category

📌 Credit history is a long-term asset.

❓ FREQUENTLY ASKED QUESTIONS (FAQs)

1. Does good credit history reduce interest rate?

Yes.

2. Is credit score or history more important?

Both matter, history more.

3. What score gets lowest rates?

750+ generally.

4. Can banks change rate based on credit?

Yes.

5. Do NBFCs also check credit history?

Yes.

6. Can interest rate be negotiated?

Yes, with strong profile.

7. Does settlement affect interest?

Severely.

8. Do old defaults still matter?

Yes, but less over time.

9. Can co-applicant help reduce rate?

Yes.

10. How often should I check credit report?

Every 6 months.

11. Does income override credit history?

No.

12. Is credit card history important?

Very.

13. Can prepayment improve rate?

Indirectly, yes.

14. Can credit history be rebuilt?

Yes, with discipline.

KEY TAKEAWAYS

Credit history directly impacts interest rates

Clean history = lower loan cost

Small rate difference means big savings

Recent behaviour matters most

Credit history is a financial asset

CONCLUSION

Your credit history doesn’t just decide whether you get a loan—it decides how expensive that loan will be. By maintaining disciplined repayment habits, you unlock lower interest rates and long-term savings.

For easy loan options with transparent guidance, explore solutions with Vizzve Financial.

👉 Apply now at www.vizzve.com

Published on : 12th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed