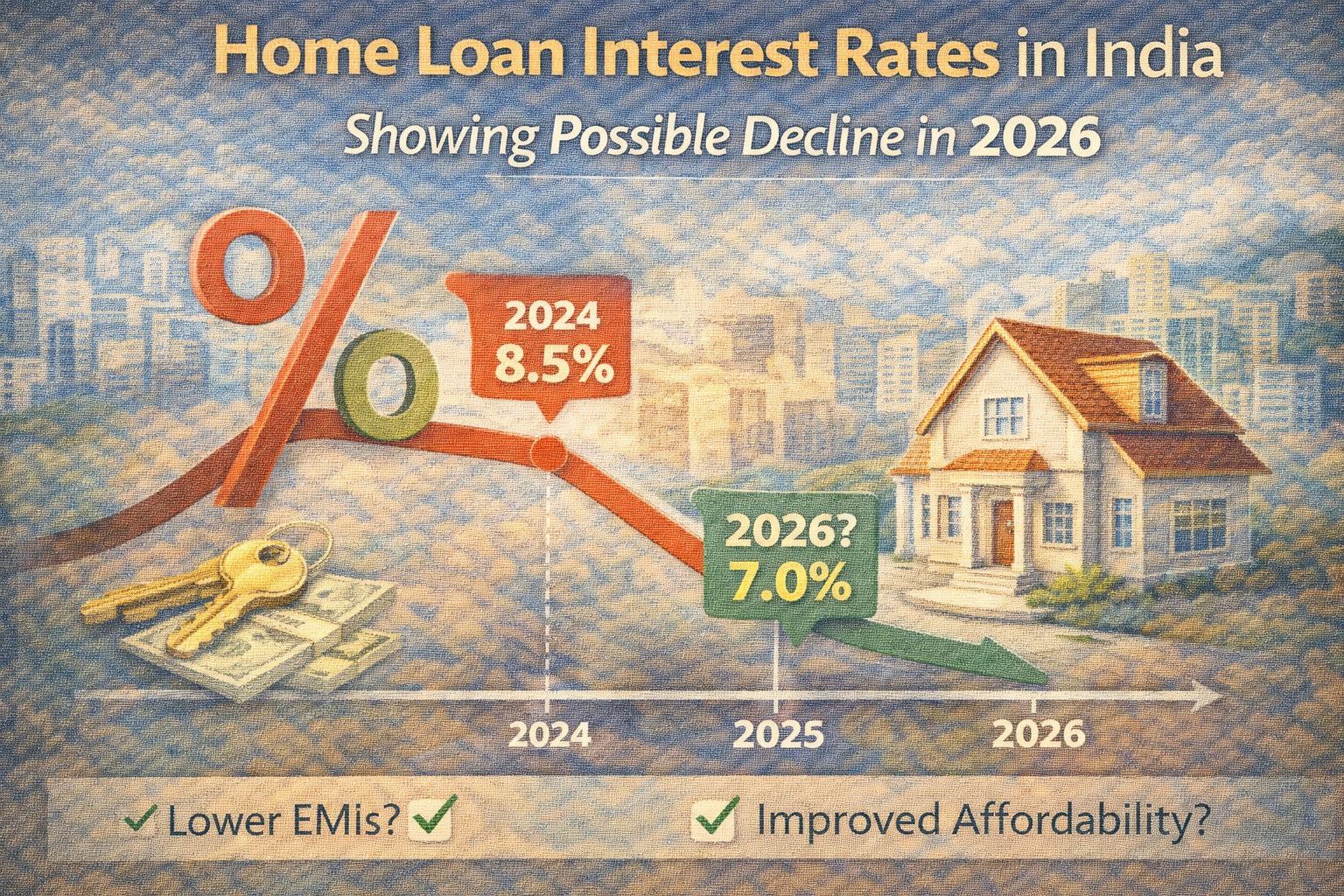

Home loan borrowers are watching 2026 closely—and for good reason.

After years of elevated interest rates, early signs point toward gradual easing, but not everyone will benefit equally.

Lower home loan rates in 2026 will reward prepared borrowers, not patient ones. This guide explains when rate cuts may happen, how much you can save, and exact actions that maximise benefits.

AI Answer Box

Short Answer:

Home loan rates in 2026 may decline gradually if inflation stays controlled. Borrowers can save most by refinancing early, prepaying strategically, and maintaining strong credit profiles.

Why Home Loan Rates Haven’t Fallen Yet

Even as inflation cools, the Reserve Bank of India remains cautious.

Key reasons:

Inflation stability still needs confirmation

Global interest rates remain tight

RBI prioritises financial stability over quick relief

📌 Rate cuts happen after confidence, not expectation.

When Home Loan Rates May Fall in 2026

Likely Timeline (If Conditions Hold)

| Period | Expected Trend |

|---|---|

| Early 2026 | Rates largely unchanged |

| Mid 2026 | Mild cuts possible |

| Late 2026 | Clearer downward cycle |

Cuts, if any, are expected to be gradual—not dramatic.

How Much Can Borrowers Really Save?

EMI Impact Illustration

| Loan Amount | Tenure | Rate Cut | Monthly EMI Savings |

|---|---|---|---|

| ₹50 lakh | 20 years | 0.50% | ₹1,500–₹1,800 |

| ₹75 lakh | 20 years | 0.75% | ₹3,000+ |

| ₹1 crore | 25 years | 1.00% | ₹6,000+ |

💡 Small rate cuts create massive long-term savings.

Who Benefits Most From Lower Rates?

Biggest Winners

Repo-linked home loan borrowers

High credit score (750+) profiles

Long-tenure borrowers

Recent loan takers (less principal repaid)

Limited Benefit

Fixed-rate loan holders

Loans nearing maturity

Borrowers with weak credit signals

Smart Ways Borrowers Can Save Big in 2026

1. Switch to Repo-Linked Loans

They pass rate cuts faster than MCLR loans.

2. Refinance at the Right Time

Even a 0.5% difference justifies switching—if charges are reasonable.

3. Prepay Strategically

Partial prepayments early in tenure:

Reduce interest burden

Shorten tenure dramatically

4. Improve Credit Score Before Cuts

Banks reward strong profiles first.

Fixed vs Floating Home Loans in 2026

| Feature | Fixed Rate | Floating Rate |

|---|---|---|

| Stability | High | Medium |

| Benefit from cuts | No | Yes |

| Risk | Lower | Market-linked |

| Best for | Short tenures | Long tenures |

📌 Floating wins during easing cycles.

Expert Commentary

“Borrowers who act before rate cuts—by improving credit and reducing balance—save more than those who simply wait.”

From real-world lending experience, borrowers who prepay early + refinance smartly gain disproportionately during easing cycles.

Common Mistakes Borrowers Make

Waiting too long to refinance

Ignoring processing & legal fees

Assuming banks auto-reduce EMIs

Focusing only on EMI, not total interest

Pros & Cons of Lower Home Loan Rates

✅ Pros

Lower EMIs

Faster principal repayment

Improved affordability

❌ Cons

Property prices may rise

Banks become selective

Fixed-rate borrowers miss out

Key Takeaways

Home loan rates may ease gradually in 2026

Early action beats passive waiting

Credit profile decides benefit level

Small cuts = large lifetime savings

Strategy matters more than timing

Frequently Asked Questions

1. Will home loan rates fall in 2026?

Possibly, if inflation remains controlled.

2. When is the best time to refinance?

Soon after the first confirmed rate cut.

3. How much difference does 0.5% make?

It can save lakhs over long tenures.

4. Should I switch from fixed to floating?

Yes, if allowed and cost-effective.

5. Do banks reduce EMIs automatically?

Not always—tenure reduction is common.

6. Is prepayment better than waiting?

Yes, especially early in the loan.

7. Are processing fees negotiable?

Often yes, for strong profiles.

8. Will property prices rise if rates fall?

Historically, yes—especially in metros.

9. Do NBFC home loans benefit equally?

Usually slower than banks.

10. Is balance transfer risky?

No, if documentation and costs are clear.

11. What credit score is ideal?

750+ for best rates.

12. Can first-time buyers benefit?

Yes, if credit discipline is strong.

Conclusion: Preparation Creates Savings

Lower home loan rates in 2026 are likely—but selective.

Borrowers who prepare early, act decisively, and optimise their loans will save far more than those who simply wait.

CTA: Smarter Home Loan Decisions Start Here

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 21st January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed