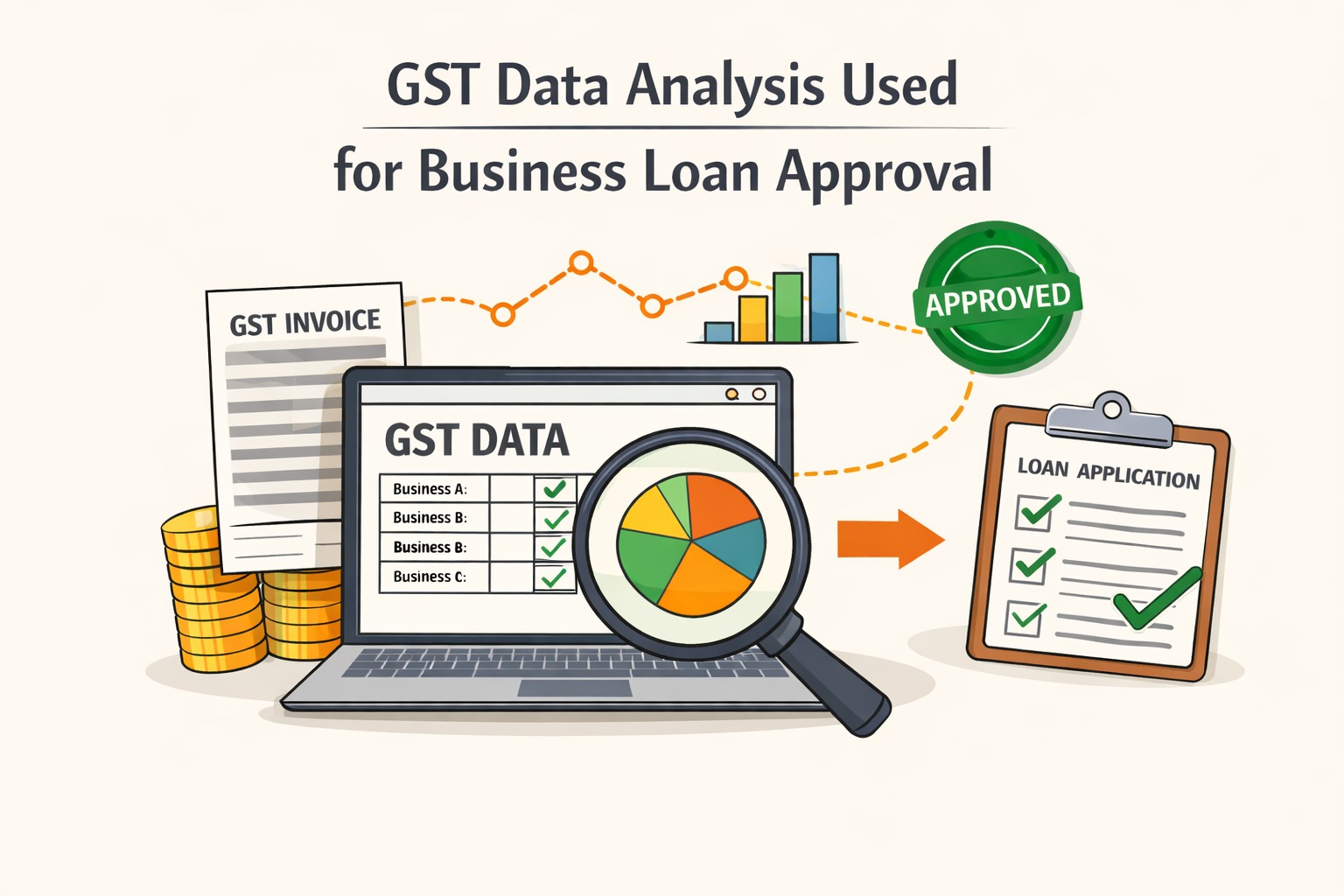

GST has quietly become one of the most powerful tools in business lending.

In 2026, banks and NBFCs are no longer relying only on collateral or balance sheets—they are approving (or rejecting) business loans based on GST data visibility.

For MSMEs, this shift can mean faster approvals or instant rejection, depending on how clean and consistent their GST filings are.

AI Answer Box

Short Answer:

GST data is changing business loan approvals by giving lenders real-time visibility into turnover, cash flow, and compliance, enabling faster, risk-based lending decisions.

Why GST Data Matters So Much to Lenders

GST data provides lenders with verified, third-party business performance signals, including:

Monthly turnover

Sales consistency

Buyer concentration

Tax compliance discipline

Unlike self-declared income, GST data is hard to manipulate.

What GST Data Lenders Analyse

Key GST Metrics Used in Loan Approval

| GST Data Point | What Banks Infer |

|---|---|

| GSTR-1 Filings | Sales stability |

| GSTR-3B Returns | Tax discipline |

| Turnover Trends | Growth or stress |

| Filing Delays | Operational risk |

| Buyer Diversity | Revenue concentration risk |

📌 Clean GST data often substitutes for collateral in small business loans.

How Loan Approvals Have Changed Post-GST

Before GST

Manual balance sheets

Collateral-heavy lending

Long approval cycles

After GST

Cash-flow based underwriting

Faster digital approvals

Reduced reliance on property collateral

GST Data and MSME Loan Speed

Businesses with:

Regular filings

Stable monthly turnover

Low variance in GST payments

often receive:

Instant or same-day approvals

Higher loan eligibility

Lower risk premiums

Role of Banks, Fintechs & Regulators

Under supervision from the Reserve Bank of India, lenders are increasingly encouraged to adopt data-driven credit models.

Fintech lenders leverage APIs from the Goods and Services Tax Network to automate:

Loan underwriting

Limit setting

Fraud detection

GST-Based Lending: What Helps Approval

Positive Signals

Consistent turnover growth

On-time GST filing

Clean mismatch records

Stable buyer base

Negative Signals

Frequent nil returns

High sales volatility

Filing gaps

Heavy dependence on 1–2 buyers

GST Data vs Traditional Documents

| Parameter | Traditional Method | GST-Based Method |

|---|---|---|

| Verification | Manual | Automated |

| Approval Speed | Weeks | Days or hours |

| Collateral Dependence | High | Lower |

| Risk Accuracy | Medium | High |

| MSME Accessibility | Limited | Wider |

Expert Commentary

“GST data has done what collateral couldn’t—it made cash flow visible.”

From real-world lending experience, MSMEs with average credit scores but strong GST data often get approved faster than asset-rich but opaque businesses.

Common Myths About GST and Loans

| Myth | Reality |

|---|---|

| Higher GST = automatic approval | Consistency matters more |

| Nil returns are harmless | They raise red flags |

| One bad month ruins eligibility | Patterns matter, not exceptions |

| Only banks use GST | NBFCs & fintechs rely heavily on it |

How Businesses Can Use GST to Improve Loan Eligibility

Step-by-Step

File GST returns on time

Avoid sharp turnover fluctuations

Diversify customer base

Reconcile mismatches quickly

Keep GST and bank inflows aligned

Who Benefits Most From GST-Based Lending?

MSMEs without property collateral

Traders and manufacturers

Service businesses with invoice trails

Digitally compliant enterprises

Key Takeaways

GST data is now central to loan approvals

Clean filings improve speed and eligibility

Cash-flow visibility beats collateral

Inconsistency hurts more than low turnover

Compliance directly impacts credit access

Frequently Asked Questions

1. Can GST data replace collateral for loans?

For small-ticket loans, often yes.

2. How many months of GST data do banks check?

Usually 6–12 months.

3. Do filing delays affect loan approval?

Yes, significantly.

4. Are GST-based loans cheaper?

Often, due to lower risk perception.

5. Can new GST registrations get loans?

Yes, but limits are lower initially.

6. Is GST mandatory for business loans?

Increasingly yes, for MSMEs.

7. What turnover qualifies for GST-based loans?

Depends on lender, not fixed.

8. Do nil returns hurt eligibility?

Yes, if frequent.

9. Can fintech lenders approve faster than banks?

Yes, due to automation.

10. Does GST mismatch cause rejection?

Unresolved mismatches do.

11. Is GST data checked for renewals?

Yes, continuously.

12. Will GST-based lending grow further?

Yes, it’s now a core credit model.

Conclusion: GST Is the New Balance Sheet

GST data has fundamentally changed how business credit works in India.

For MSMEs, compliance is no longer just a tax obligation—it’s a credit passport.

Those who maintain clean, consistent GST records will find credit faster, cheaper, and more accessible.

CTA: Smarter Business Borrowing Starts Here

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 21st January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed