Introduction

Many microfinance borrowers ask one common question:

“How is interest calculated on my MFI loan?”

Because MFI loans are small and repayments are frequent, interest calculation can feel confusing. Understanding this is important because it helps borrowers know the true cost of the loan, avoid misunderstandings, and plan repayments better.

This blog explains how interest is calculated in MFI loans in simple language, with examples anyone can understand.

Quick Answer

MFI loan interest is usually calculated using either the flat rate method or the reducing balance method, and EMIs are fixed based on loan amount, tenure, and interest rate.

AI Answer Box

How is interest calculated in MFI loans?

In MFI loans, interest is calculated using flat or reducing balance methods. The borrower repays the principal and interest in fixed EMIs over the loan tenure.

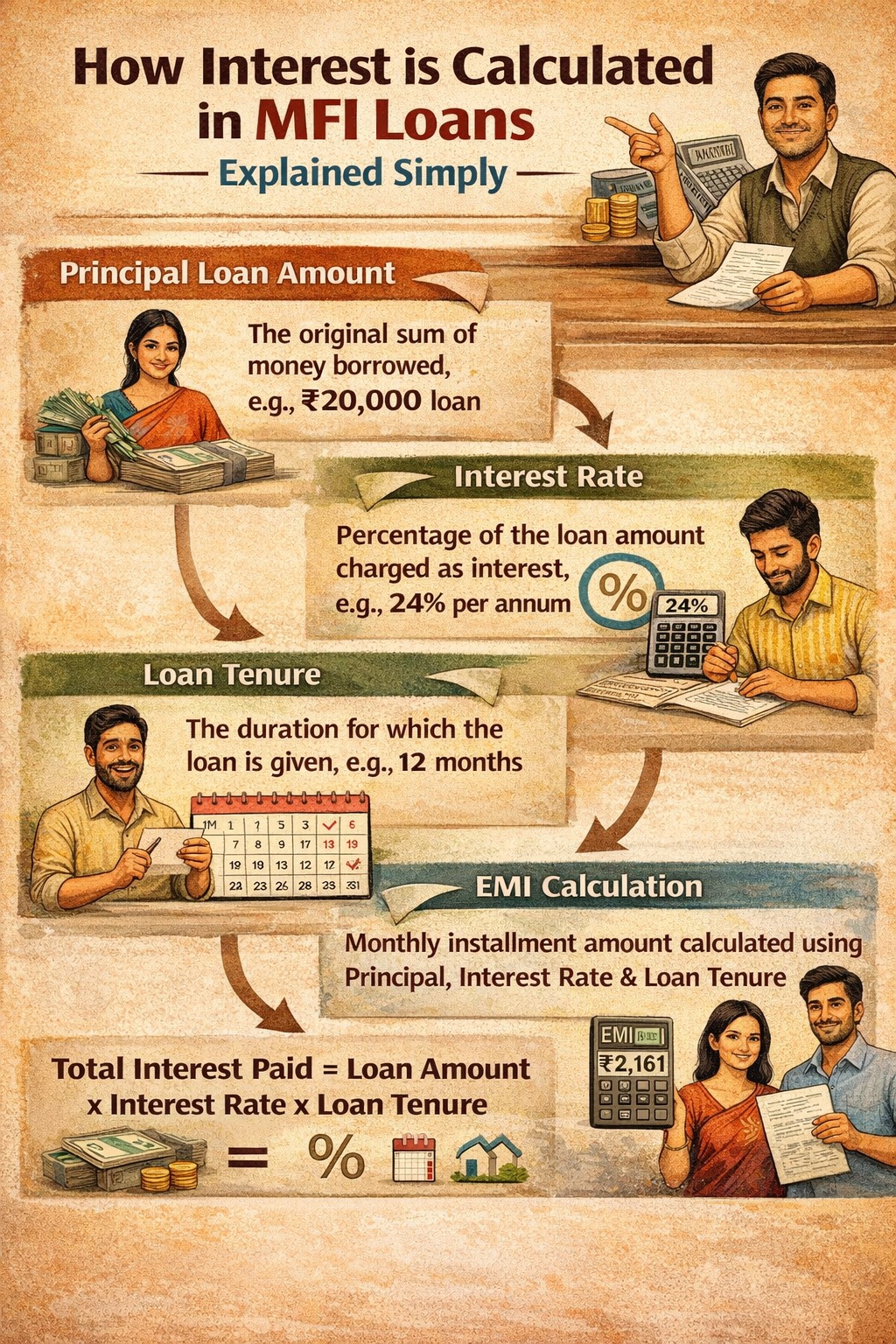

What Is an MFI Loan?

An MFI (Microfinance Institution) loan is a small, collateral-free loan given to borrowers who may not have access to traditional bank credit.

In India, MFI lending is regulated by the Reserve Bank of India, which mandates transparency, borrower consent, and fair practices.

Methods Used to Calculate Interest in MFI Loans

1. Flat Interest Rate Method (Most Common)

Under the flat rate method, interest is calculated on the entire loan amount for the full tenure, even though the principal reduces with each EMI.

Example (Flat Method)

| Details | Amount |

|---|---|

| Loan Amount | ₹20,000 |

| Interest Rate | 24% per year |

| Tenure | 1 year |

| Total Interest | ₹4,800 |

| Total Repayment | ₹24,800 |

👉 EMI = ₹24,800 ÷ 52 weeks ≈ ₹477 per week

🔍 Important:

Even though the principal reduces weekly, interest remains fixed.

2. Reducing Balance Method (Less Common but Fairer)

Here, interest is calculated only on the outstanding principal, which reduces after every EMI.

Example (Reducing Method)

| Details | Amount |

|---|---|

| Loan Amount | ₹20,000 |

| Interest Rate | 24% |

| Tenure | 12 months |

| Interest Charged | Lower than flat |

| EMI | Slightly higher initially |

👉 Borrowers pay less total interest compared to the flat method.

Flat vs Reducing Interest (Simple Comparison)

| Feature | Flat Rate | Reducing Balance |

|---|---|---|

| Interest Calculation | On full amount | On outstanding |

| Transparency | Looks simple | More accurate |

| Total Interest | Higher | Lower |

| Borrower Friendly | ❌ | ✅ |

Why MFIs Use Flat Interest Rates

MFIs often use flat rates because:

Loans are small and short-term

Weekly repayments are easier to manage

Field operations are simplified

Borrowers prefer fixed EMIs

However, RBI requires full disclosure of the effective interest rate.

What Is Effective Interest Rate (EIR)?

The Effective Interest Rate (EIR) shows the actual cost of the loan, including:

Flat interest

Processing fees

Insurance charges (if any)

👉 EIR is always higher than the flat rate and must be disclosed to borrowers.

EMI Structure in MFI Loans

Each EMI includes:

A portion of principal repayment

A portion of interest

Example EMI Split (Weekly)

| EMI Component | Amount |

|---|---|

| Principal | ₹300 |

| Interest | ₹177 |

| Total EMI | ₹477 |

Additional Charges Borrowers Should Know

MFIs may charge:

Processing fees

Insurance premium (optional)

GST on services

⚠️ All charges must be disclosed upfront as per RBI norms.

Expert Commentary

“Borrowers often focus only on EMI amount, but understanding the interest method helps them compare loans and avoid confusion later.”

— Microfinance Training & Compliance Expert, India

Common Misunderstandings About MFI Interest

“Interest reduces every week” (Not in flat method)

“Flat rate is cheaper” (Usually not)

“EMI equals interest only” (Wrong)

Education helps avoid disputes.

Pros & Cons of MFI Interest Structure

✔️ Pros

Fixed EMI

Easy budgeting

Simple repayment

❌ Cons

Higher effective interest

Flat rate can be misleading

Summary Box

MFI interest is usually flat-rate

Reducing balance is fairer but rare

EIR shows true loan cost

Transparency is mandatory

Key Takeaways

Always ask for effective interest rate

Understand flat vs reducing method

Fixed EMI doesn’t mean low cost

Awareness = better borrowing decisions

❓ Frequently Asked Questions (14 FAQs)

1. How do MFIs calculate interest?

Using flat or reducing balance methods.

2. Which method is most common?

Flat interest method.

3. Is flat interest bad?

Not bad, but costlier than reducing.

4. What is effective interest rate?

Actual cost including all charges.

5. Do MFIs disclose interest clearly?

Yes, RBI mandates disclosure.

6. Are EMIs fixed in MFI loans?

Yes, usually fixed.

7. Is interest charged weekly?

Interest is annual but repaid weekly.

8. Can borrowers ask for EMI breakup?

Yes, they have the right to know.

9. Are processing fees allowed?

Yes, with disclosure.

10. Is insurance compulsory?

Usually optional.

11. Can interest rates differ between MFIs?

Yes.

12. Does credit score affect MFI interest?

Sometimes, for repeat borrowers.

13. Are MFI loans regulated?

Yes, by RBI.

14. Does Vizzve Financial follow RBI norms?

Yes, fully compliant.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply now at www.vizzve.com

Published on : 27th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed