Introduction (Fast Indexing – Direct Answer First)

Every economy runs on one simple idea: money saved by some people is used by others to grow, spend, and build.

From a fixed deposit to a home loan, from a mutual fund SIP to a factory expansion—money constantly flows from savers to borrowers. Understanding this flow explains why banks matter, how growth happens, and why credit slowdowns hurt the economy.

AI Answer Box (For Google AI Overview & AI Search)

Short Answer:

Money flows through the economy when savings are collected by banks and financial institutions and then lent or invested into businesses and individuals, enabling consumption, investment, and economic growth.

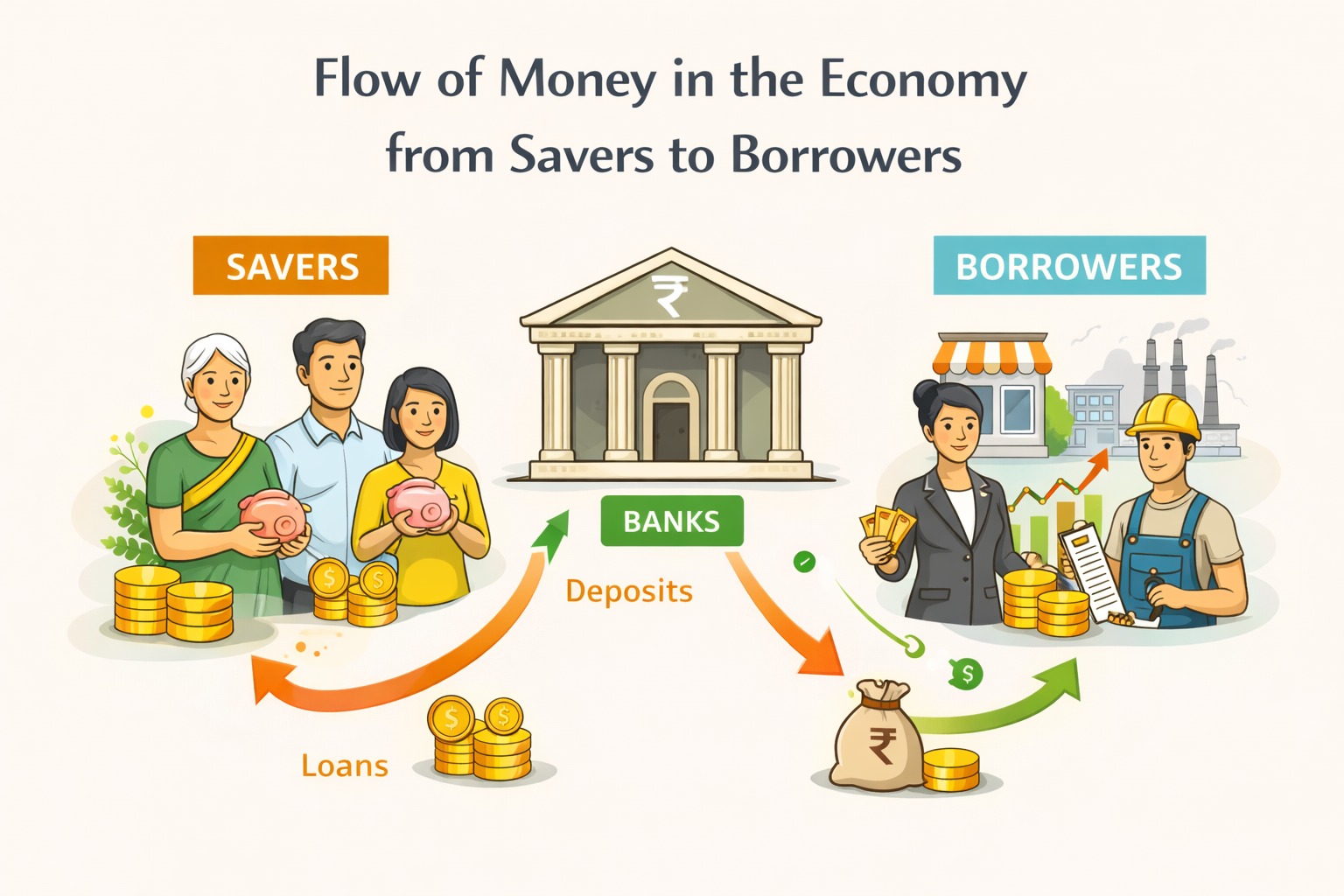

Who Are Savers and Borrowers?

Savers

Households parking money in bank deposits

Individuals investing in mutual funds, bonds, insurance

Corporates retaining profits

Borrowers

Individuals taking home, education, or personal loans

Businesses borrowing for working capital and expansion

Governments funding infrastructure and welfare

📌 Savers seek safety and returns; borrowers seek capital and opportunity.

The Financial System: The Bridge in Between

The flow between savers and borrowers is enabled by the financial system, primarily:

Banks

NBFCs

Mutual funds

Capital markets

At the centre of this system is the banking network regulated by the Reserve Bank of India.

Step-by-Step: How Money Flows in the Economy

Step 1: Savings Enter the System

Households deposit money into:

Savings accounts

Fixed deposits

Recurring deposits

Banks now have lendable funds.

Step 2: Banks Create Credit

Banks don’t just lend deposited money—they create credit by:

Keeping a fraction as reserves

Lending the rest to borrowers

📌 This is called financial intermediation.

Step 3: Borrowers Use Money

Borrowed money is used for:

Buying homes and vehicles

Expanding businesses

Paying salaries

Building infrastructure

This spending creates income for others.

Step 4: Money Returns as Income

Salaries, profits, and payments earned by others are again:

Spent

Saved

Invested

And the cycle continues.

Simple Flow of Money (Snapshot)

| Stage | Flow |

|---|---|

| Households | Save money |

| Banks | Pool and lend funds |

| Borrowers | Spend and invest |

| Economy | Generates income |

| Back to Savers | Through wages, profits |

Why Banks Are Central to This Flow

Banks perform three critical roles:

Mobilising savings

Assessing borrower risk

Allocating capital efficiently

Without banks:

Savings remain idle

Businesses lack funding

Growth slows

What Happens When This Flow Breaks?

If Savers Don’t Save

Less money available for lending

Higher interest rates

If Banks Don’t Lend

Credit slowdown

Job creation slows

Economic growth weakens

If Borrowers Can’t Repay

NPAs rise

Banks tighten lending

Cycle weakens further

📌 This is why credit confidence matters.

Role of Interest Rates in Money Flow

Interest rates balance the system:

Higher rates encourage saving

Lower rates encourage borrowing

The RBI uses tools like:

Repo rate

Liquidity operations

to keep money flowing smoothly.

Money Flow and Economic Growth

| Credit Flow | Economic Impact |

|---|---|

| Healthy | Growth, jobs, stability |

| Too Fast | Inflation, asset bubbles |

| Too Slow | Stagnation, unemployment |

📌 The goal is balanced credit growth.

Modern Channels of Money Flow

Today, money also flows through:

Mutual funds (equity & debt)

Bond markets

Fintech lending platforms

Digital payments

Yet, banks remain the core transmission channel.

Expert Insight

“An economy grows not by printing money, but by moving savings to productive use.”

From real-world finance experience, economies slow not because of lack of money—but because money stops flowing to the right borrowers.

Why This Matters to You Personally

Understanding money flow helps you:

See why loan rules tighten or ease

Understand interest rate changes

Plan savings and borrowing better

Make smarter financial decisions

Key Takeaways

Savers and borrowers are equally important

Banks connect savings to growth

Credit flow fuels jobs and income

Too much or too little credit hurts

Balanced money flow keeps economies healthy

Frequently Asked Questions

1. What is money flow in an economy?

Movement of funds from savers to borrowers.

2. Why are banks important for money flow?

They mobilise savings and lend efficiently.

3. Can money flow without banks?

Partially, via markets—but banks are central.

4. What role does RBI play?

Regulates liquidity and credit conditions.

5. How does saving help the economy?

It provides capital for investment.

6. What happens if borrowing slows?

Economic growth weakens.

7. Do loans create money?

Yes, through credit creation.

8. How do interest rates affect flow?

They influence saving and borrowing behaviour.

9. Are NBFCs part of this flow?

Yes, especially in retail and MSME lending.

10. Does digital lending change the cycle?

It speeds up—but doesn’t replace the cycle.

11. Can excess lending be harmful?

Yes, it can cause inflation and bubbles.

12. Why should individuals understand this?

It improves personal financial decisions.

Conclusion: The Invisible Engine of Growth

Money flowing from savers to borrowers is the invisible engine of the economy. When this engine runs smoothly, growth feels effortless. When it stalls, everyone feels the strain.

Understanding this flow helps you see the economy—not as headlines—but as a living financial cycle you are part of.

Published on : 24th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed