Prepayment charges are fees lenders may charge when you repay a loan early. They usually apply to fixed-rate or business loans, while most floating-rate home loans have zero prepayment charges. Whether prepayment makes sense depends on interest saved vs penalty paid.

AI Answer Box

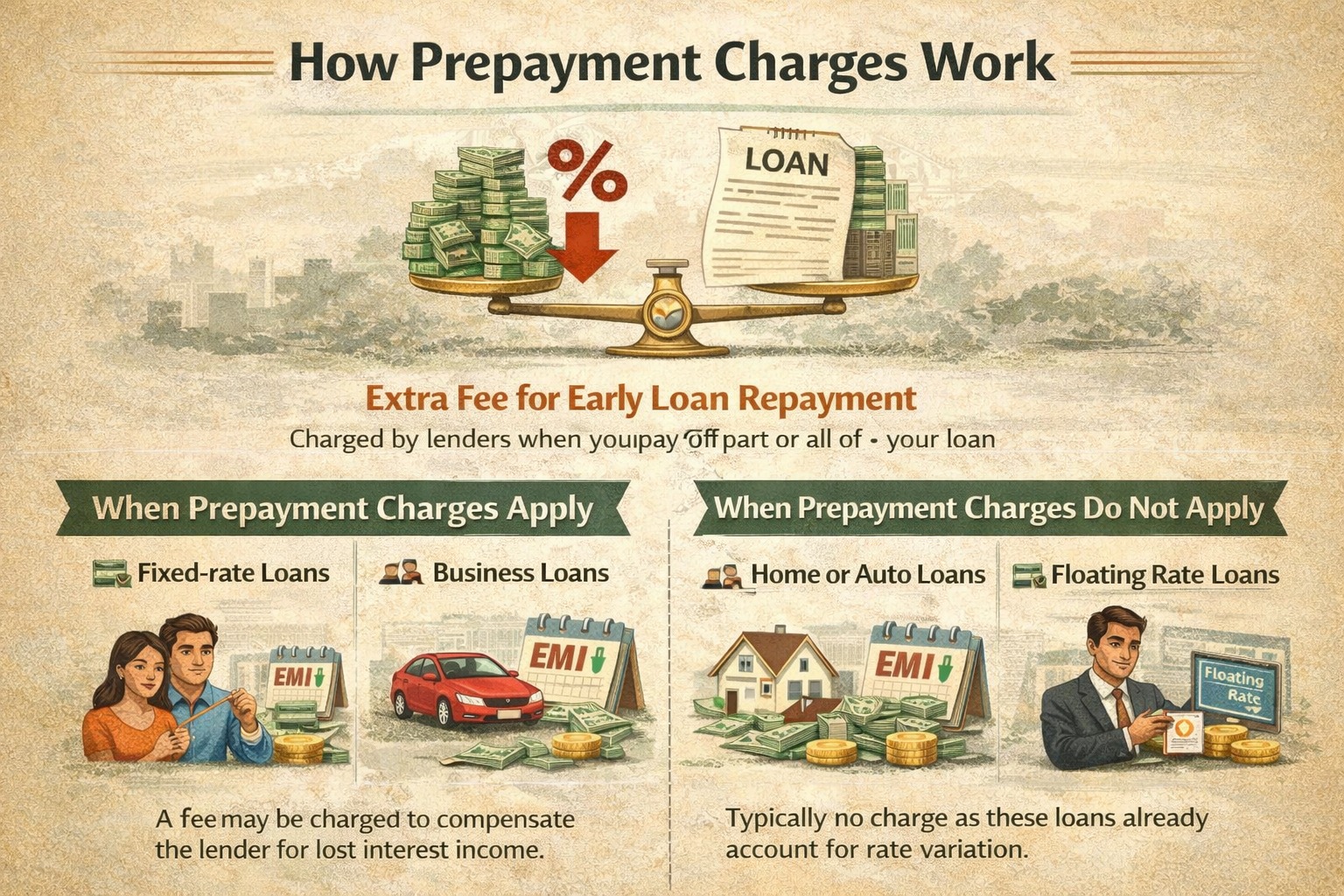

How prepayment charges work:

Charged for early loan closure or part payment

Common in fixed-rate and personal loans

Rare for floating-rate home loans

Calculated as a % of outstanding amount

Must be compared with interest savings

🔹 Introduction

Paying off a loan early feels like the smartest financial move. But many borrowers are surprised to see prepayment or foreclosure charges added to their loan statement.

So what are these charges, why do lenders apply them, and when should you actually pay them?

This guide breaks down how prepayment charges work in India, what RBI rules say, and how to decide whether prepaying your loan truly saves money.

🔹 What Is a Prepayment Charge?

A prepayment charge (also called foreclosure charge) is a fee a lender may levy when:

You repay the full loan before tenure ends, or

You make large part-payments beyond allowed limits

It compensates the lender for lost future interest income.

🔹 Types of Loan Prepayments

1. Part Prepayment

You repay a portion of the outstanding loan

EMIs reduce or tenure shortens

2. Full Prepayment (Foreclosure)

You close the entire loan early

Account is marked “Closed”

Charges may apply to either or both, depending on loan terms.

🔹 Which Loans Have Prepayment Charges?

| Loan Type | Prepayment Charges |

|---|---|

| Floating-rate home loan | ❌ Usually Nil |

| Fixed-rate home loan | ✅ Often Applicable |

| Personal loan | ✅ Common |

| Business loan | ✅ Common |

| Education loan | ❌ Mostly Nil |

| Credit card dues | ❌ Nil |

📌 Policies vary by lender and loan agreement.

🔹 RBI Rules on Prepayment Charges (Important)

The Reserve Bank of India has clarified:

No prepayment charges on floating-rate home loans for individuals

Lenders must clearly disclose charges upfront

No hidden foreclosure fees allowed

➡️ This rule protects home loan borrowers—but does not apply to all loan types.

🔹 How Prepayment Charges Are Calculated

Most lenders charge:

2%–5% of outstanding principal, plus GST

Example:

Outstanding loan: ₹5,00,000

Prepayment charge: 3%

Fee = ₹15,000 + GST

This amount must be compared with interest saved.

🔹 When Prepayment Makes Financial Sense

✅ Prepay If:

Interest rate is high

Loan tenure is long

Charges are low or zero

You have surplus funds

❌ Avoid Prepaying If:

Charges are high

Loan is near completion

You need liquidity

Funds can earn higher returns elsewhere

🔹 Prepayment vs Interest Savings (Comparison)

| Factor | Prepaying Early | Continuing Loan |

|---|---|---|

| Interest Cost | Lower | Higher |

| Liquidity | Reduced | Preserved |

| Credit Score | Neutral/Positive | Neutral |

| Flexibility | Lower | Higher |

🔹 Common Borrower Mistakes

🚫 Ignoring prepayment clauses

🚫 Prepaying small loans with high charges

🚫 Using emergency funds to prepay

🚫 Not checking minimum lock-in period

🔹 Real-World Borrower Insight

From loan behaviour analysis, borrowers who prepay high-interest personal loans early—even with small charges—save significantly, while prepaying low-interest loans late in tenure often offers minimal benefit.

➡️ Math matters more than emotion.

🔹 Step-by-Step: How to Check Your Prepayment Charges

Read your loan sanction letter

Check lock-in period

Ask lender for foreclosure statement

Calculate interest saved

Compare with charges + GST

Only then decide.

🔹 Pros & Cons of Prepayment Charges

✅ Pros (From Lender Perspective)

Compensates lost interest

Maintains revenue stability

❌ Cons (For Borrowers)

Discourages early closure

Reduces flexibility

🔹 Key Takeaways

Prepayment charges vary by loan type

Floating home loans usually have zero charges

Fixed and personal loans often attract fees

Always compare charges vs savings

Smart prepayment saves money

🔹 Frequently Asked Questions (FAQs)

1. What are prepayment charges?

Fees for closing a loan early.

2. Are prepayment charges legal?

Yes, if disclosed upfront.

3. Do all loans have prepayment charges?

No.

4. Are floating home loans charged?

Usually no.

5. How much are prepayment charges?

2%–5% typically.

6. Is GST applied?

Yes.

7. Can banks waive charges?

Sometimes, on request.

8. Does prepayment affect credit score?

Usually positive or neutral.

9. Is part prepayment better than foreclosure?

Often yes.

10. Can I prepay anytime?

After lock-in period.

11. Do NBFCs charge more?

Often yes.

12. Should I always prepay if I have money?

No—compare returns first.

🔹 Conclusion + CTA

Prepayment charges aren’t bad by default—but ignoring them can turn a smart decision into a costly one. Borrowers who understand their loan terms, do the math, and plan prepayments strategically always come out ahead.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 8th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed