Many borrowers believe that income alone decides how much loan they will get next time.

But in microfinance, there is something even more important:

👉 Your repayment history.

How you repay your current loan strongly decides whether you get a higher loan, the same amount, or no loan at all in the future.

This blog explains how repayment history affects future loan size, in simple language, with clear examples, so borrowers know exactly what matters most.

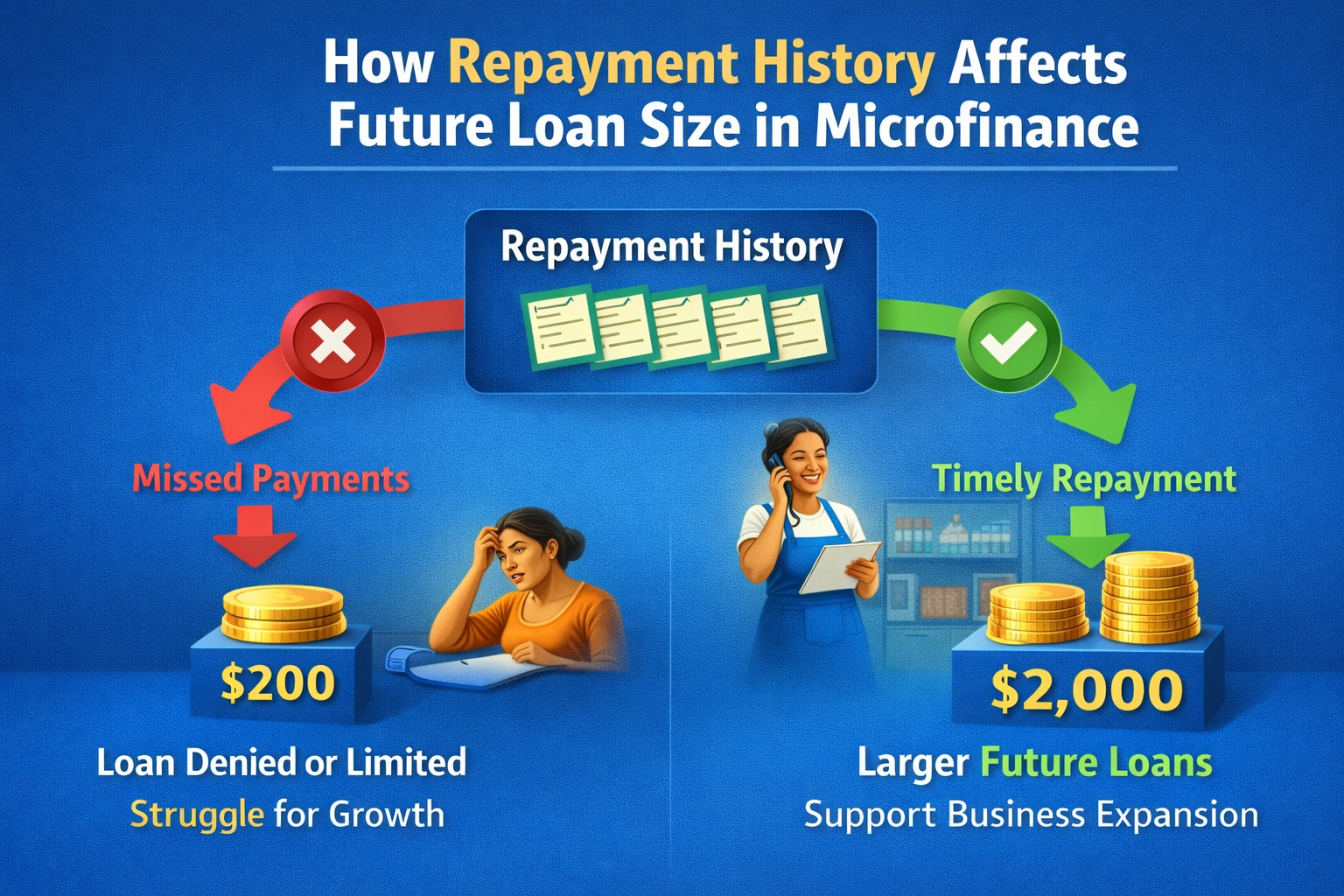

Quick Answer

In MFI loans, timely and regular repayment builds trust and directly increases eligibility for a higher loan amount in the next cycle. Missed EMIs reduce or block loan growth.

AI Answer Box

How does repayment history affect future loan size?

Repayment history shows how responsibly a borrower pays EMIs. Timely repayments increase trust and eligibility for higher loans, while delays or defaults reduce future loan size.

What Is Repayment History?

Repayment history is a record of:

EMIs paid on time

Delayed payments

Missed EMIs

Loan completion status

MFIs track this data for every borrower and use it to assess future loan eligibility.

Why Repayment History Matters So Much in MFIs

Unlike banks that rely heavily on credit scores, MFIs focus on behaviour-based lending.

Repayment history tells MFIs:

Can the borrower manage regular EMIs?

Is the borrower disciplined?

Can a higher EMI be handled safely?

This approach follows guidelines of the Reserve Bank of India, which promotes responsible lending.

How Good Repayment History Increases Future Loan Size

1. Builds Trust with the MFI

When you pay:

Every EMI on time

Without reminders

You prove reliability. Trust = eligibility for higher loan.

2. Improves Loan Cycle Progression

MFIs use loan cycles:

1st loan → small

2nd loan → bigger

3rd loan → even bigger

Good repayment allows smooth movement through these cycles.

3. Shows Higher Repayment Capacity

Consistent repayment indicates:

Stable income

Good cash-flow management

MFIs feel confident offering a higher loan amount.

Example: Repayment History vs Loan Size

| Repayment Record | Next Loan Eligibility |

|---|---|

| All EMIs on time | Higher loan amount |

| 1–2 late EMIs | Same or slightly higher |

| Frequent delays | Same or reduced |

| Defaults | Loan rejected |

How Poor Repayment History Reduces Loan Size

❌ 1. Missed EMIs Signal Risk

Missed payments suggest:

Income instability

Poor planning

MFIs reduce risk by limiting future loan size.

❌ 2. Delays Affect Credit Profile

Many MFIs now report repayment data to credit bureaus.

Poor repayment may affect future borrowing beyond MFIs.

❌ 3. May Stop Loan Cycle Growth

Even one bad cycle can:

Freeze loan amount

Reset borrower to lower cycle

Delay access to higher loans

RBI’s Role in Repayment-Based Lending

RBI requires MFIs to:

Assess repayment capacity every cycle

Avoid over-indebtedness

Increase loan only when safe

This ensures borrower protection, not punishment.

Pros & Cons of Repayment-Based Loan Growth

✔️ Pros

Rewards discipline

Prevents debt stress

Encourages financial responsibility

❌ Cons

One mistake can slow growth

Requires regular planning

Expert Commentary

“In microfinance, repayment behaviour matters more than income promises. Discipline today decides opportunity tomorrow.”

— Microfinance Credit Risk Expert, India

Summary Box

Repayment history is critical in MFIs

Timely EMIs increase loan size

Missed EMIs reduce eligibility

RBI promotes repayment-based lending

Key Takeaways

Pay every EMI on time

One good cycle builds trust

Discipline unlocks bigger loans

Repayment history travels with you

❓ Frequently Asked Questions (14 FAQs)

1. Does repayment history affect next loan?

Yes, strongly.

2. Will one late EMI stop loan increase?

It may reduce chances.

3. How many EMIs should be on time?

Ideally all.

4. Can loan amount reduce next cycle?

Yes, if repayment is poor.

5. Do MFIs check repayment every cycle?

Yes.

6. Is repayment history shared with bureaus?

Often yes.

7. Can good repayment double loan amount?

Only if income supports it.

8. Does early repayment help?

Yes, it improves profile.

9. Can I recover from a bad cycle?

Yes, with disciplined repayment.

10. Is repayment more important than income?

Often yes, in MFIs.

11. Are women borrowers treated differently?

No.

12. Is this RBI mandated?

Yes, under responsible lending.

13. Can MFIs deny loan due to repayment issues?

Yes.

14. Does Vizzve Financial follow repayment-based assessment?

Yes, responsibly.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply now at www.vizzve.com

Published on : 28th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed