Introduction

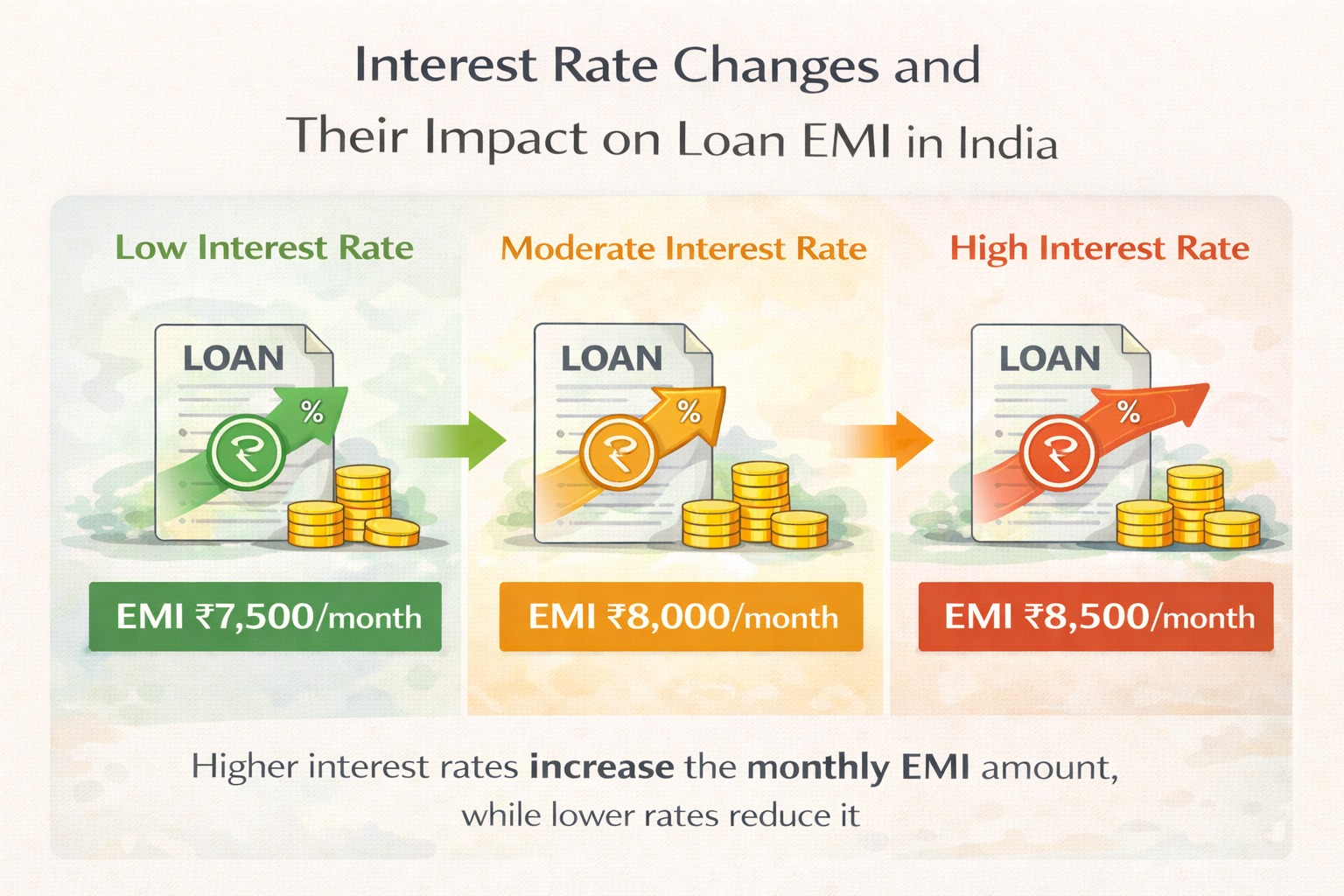

Interest rates may look like small numbers, but even a 1% change can significantly impact your monthly EMI, total loan cost, and repayment period.

In India, interest rates are influenced by policies set by the Reserve Bank of India. Whether you are a personal loan borrower, home loan customer, or microfinance borrower, understanding interest rate changes helps you borrow smarter and avoid financial stress.

This blog explains interest rate changes in simple language, with real examples and practical borrower tips.

Quick Answer

Interest rate changes directly affect your loan EMI, total interest paid, and borrowing affordability—especially for floating-rate loans.

AI Answer Box

What should borrowers know about interest rate changes?

Borrowers should know that interest rate hikes increase EMIs and total loan cost, while rate cuts reduce repayment burden, mainly affecting floating-rate loans.

What Are Interest Rates?

An interest rate is the cost you pay for borrowing money. It is usually expressed as a percentage per year.

Interest rates depend on:

RBI policy decisions

Inflation levels

Economic growth

Banking liquidity

How RBI Interest Rate Changes Work

RBI uses tools like the repo rate to control money supply.

When RBI increases rates:

Borrowing becomes expensive

EMIs increase

Spending slows down

When RBI cuts rates:

Loans become cheaper

EMIs reduce

Spending and growth increase

How Interest Rate Changes Affect Borrowers

1. Impact on Loan EMIs

Even a small increase can raise EMIs significantly.

Example:

| Loan Amount | Interest Rate | EMI |

|---|---|---|

| ₹5,00,000 | 10% | ₹10,624 |

| ₹5,00,000 | 11% | ₹10,870 |

👉 Over time, this adds thousands in extra interest.

2. Effect on Home Loans

Home loans are usually long-term & floating-rate, making them highly sensitive to rate changes.

Rate hike → Higher EMI or longer tenure

Rate cut → Lower EMI or faster closure

3. Personal & Microfinance Loans

Mostly short-term

Interest rates already higher

Rate hikes impact cash flow immediately

This is critical for low-income and small business borrowers.

4. Fixed vs Floating Interest Rates

| Feature | Fixed Rate | Floating Rate |

|---|---|---|

| EMI Stability | Stable | Changes |

| Rate Benefit | Limited | High |

| Risk | Low | Medium–High |

👉 Floating rates benefit more from rate cuts but suffer during hikes.

5. Total Loan Cost Increases

Higher rates don’t just raise EMI—they increase total interest paid over the loan’s life.

Long-term impact:

More interest

Slower principal reduction

Delayed financial goals

What Borrowers Should Do When Rates Change

✅ 1. Review Your Loan Type

Floating or fixed?

Short or long tenure?

🔁 2. Consider EMI vs Tenure Adjustment

Increase EMI to save interest

Or extend tenure to reduce pressure

💰 3. Avoid New Loans During Rate Hikes

Unless necessary, postpone borrowing.

🔍 4. Compare Lenders

Banks, NBFCs, and MFIs offer different rates.

📉 5. Prepay When Possible

Partial prepayments reduce interest burden.

Expert Commentary

“Borrowers who actively manage their loans during interest rate cycles save significantly more than those who ignore rate changes.”

— Retail Lending Advisor, India

Common Borrower Mistakes

Ignoring RBI announcements

Assuming EMI won’t change

Taking multiple loans during hikes

Not reading loan terms

Pros & Cons of Interest Rate Changes

✔️ Benefits (Rate Cuts)

Lower EMIs

Affordable loans

Faster repayments

❌ Risks (Rate Hikes)

EMI stress

Higher debt burden

Reduced savings

Summary Box

Interest rates control loan affordability

Floating loans are most affected

Awareness helps reduce repayment stress

Key Takeaways

Small rate changes have big effects

Floating-rate borrowers must stay alert

EMI planning is crucial

Smart borrowers adapt quickly

❓ Frequently Asked Questions (14 FAQs)

1. Who decides interest rates in India?

The Reserve Bank of India.

2. Do interest rate hikes affect all loans?

Mostly floating-rate loans.

3. Can EMI increase suddenly?

Yes, after rate revisions.

4. Are microfinance loans affected?

Yes, especially new loans.

5. What is repo rate?

The rate at which RBI lends to banks.

6. Is fixed rate always better?

Not always—it depends on cycles.

7. Can I switch lenders?

Yes, via balance transfer.

8. Do rate cuts reduce EMI automatically?

Usually, yes for floating loans.

9. Should I prepay during hikes?

Yes, if affordable.

10. Does credit score affect interest rate?

Yes, strongly.

11. Can NBFC rates differ from banks?

Yes, often higher.

12. How often do rates change?

Based on RBI policy reviews.

13. Are EMIs revised immediately?

Usually within 1–3 months.

14. Does Vizzve Financial adjust rates fairly?

Yes, as per lending norms.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply now at www.vizzve.com

Published on : 27th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed