Loan balance transfer is worth it when the new lender offers a significantly lower interest rate with minimal fees — helping you save money and reduce EMIs. It’s not beneficial if charges cancel out the savings.

Introduction

Are your loan EMIs feeling too heavy?

Many Indian borrowers in 2026 are shifting loans from one lender to another through loan balance transfer — mainly to get lower interest rates and better repayment terms.

This process operates under consumer-friendly lending rules supervised by the Reserve Bank of India.

But is it really a smart move for everyone?

Let’s break it down in the simplest way possible.

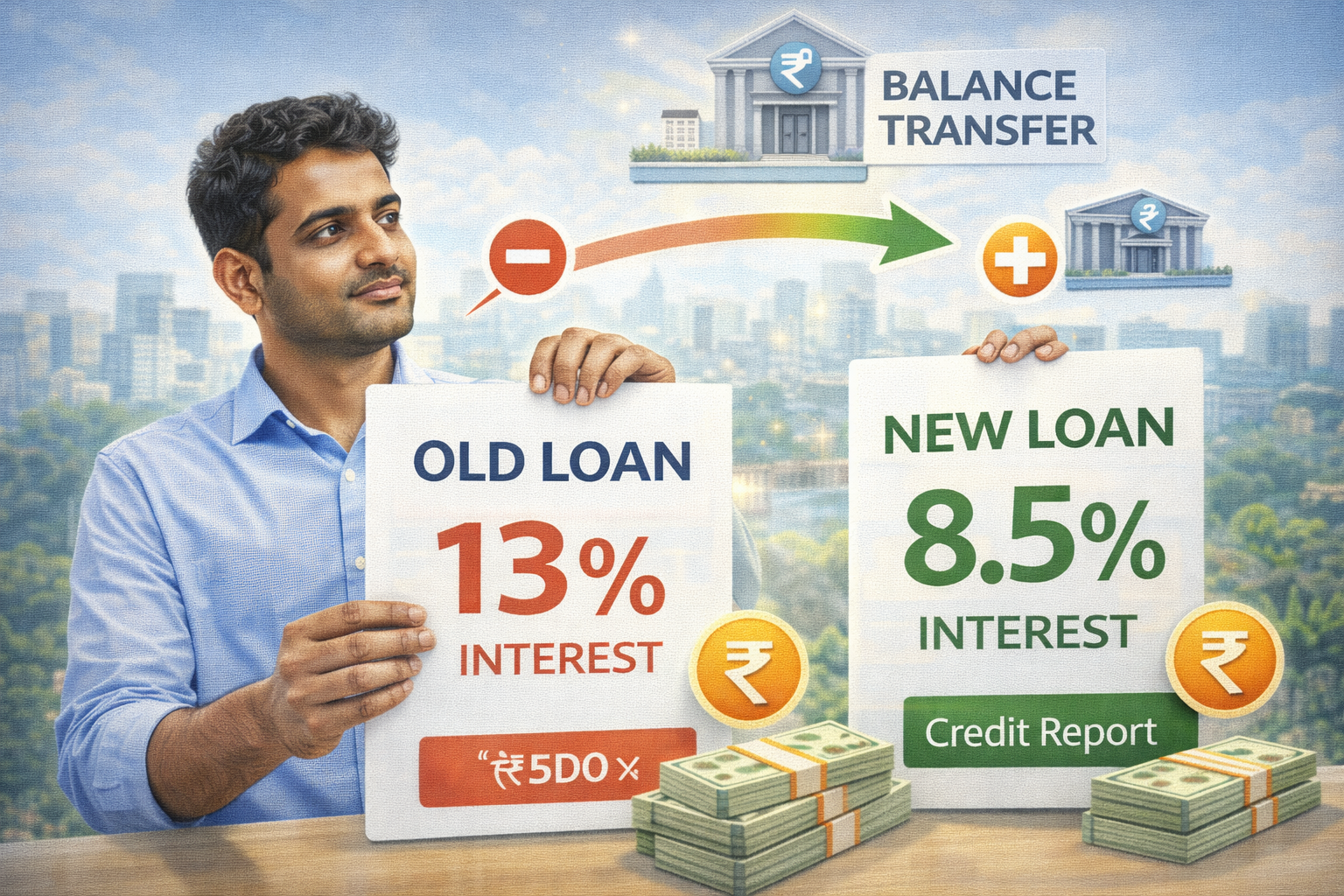

What Is a Loan Balance Transfer?

A balance transfer means:

➡ Moving your existing loan to a new bank or NBFC offering better terms.

Usually done for:

✔ Home loans

✔ Personal loans

✔ Business loans

Goal: Lower interest + smaller EMIs + interest savings

When Balance Transfer Is a Smart Choice

1. Interest Rate Is At Least 2% Lower

This usually creates real savings.

2. EMI Becomes Comfortable

Better cash flow every month.

3. Long Tenure Remaining

Earlier transfer = more interest saved.

4. Your Credit Score Has Improved

Better profile = better offers.

When It’s NOT Worth It

❌ High foreclosure charges

❌ Small interest difference

❌ Near loan completion

❌ Heavy processing fees

In these cases, savings disappear.

Simple Example (Real Impact)

| Situation | Old Loan | New Loan |

|---|---|---|

| Interest rate | 14% | 11% |

| Balance left | ₹5 lakh | ₹5 lakh |

| Tenure | 3 years | 3 years |

| Savings | — | ₹35,000+ |

Benefits of Loan Balance Transfer

✔ Lower total interest

✔ Reduced EMI

✔ Better service & flexibility

✔ Possibility of top-up loan

✔ Improved financial comfort

Hidden Costs to Check Carefully

| Charge Type | Typical Range |

|---|---|

| Foreclosure fee | 1%–5% |

| Processing fee | 0.5%–2% |

| Legal/admin charges | Varies |

| GST | Extra |

👉 Always calculate net savings after fees.

Smart Balance Transfer Checklist

✅ Compare new interest rate

✅ Ask about foreclosure charges

✅ Add all processing costs

✅ Check tenure impact

✅ Avoid borrowing extra money unnecessarily

Expert Insight

Home Loan Advisor – Mumbai

“Most savings come when you transfer early in the loan period — late transfers rarely help.”

Retail Banking Consultant – Bengaluru

“A 2% interest drop is usually the tipping point for meaningful benefit.”

Simple Step-by-Step Transfer Process

1️⃣ Check current outstanding balance

2️⃣ Compare lender offers

3️⃣ Apply for new loan

4️⃣ New lender pays old lender

5️⃣ Loan shifts with fresh EMI plan

Key Takeaways

Balance transfer can save big money

Works best early in loan tenure

Needs 2%+ interest drop to matter

Hidden fees must be calculated

Smart move when savings are real

❓ FAQs –

1. Is balance transfer allowed for all loans?

Mostly home, personal, and business loans.

2. Does it affect credit score?

Small temporary dip — improves later if managed well.

3. Can I get extra money during transfer?

Yes — top-up loans may be offered.

4. Are foreclosure charges mandatory?

Depends on lender and loan type.

5. Is paperwork heavy?

Usually moderate — easier than new loan.

6. How long does transfer take?

7–15 days typically.

7. Can I transfer multiple times?

Yes — but frequent shifts may affect credit health.

8. Should I transfer near loan end?

Usually not worth it.

Final Verdict

👉 Yes — balance transfer is worth it when interest drops significantly and fees are low.

👉 No — it’s not useful when savings are small or charges are high.

In 2026, smart borrowers use balance transfer as a money-saving tool — not an emotional escape from EMIs.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com

Published on : 21st February

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed