RBI is not banning personal loans, but recent regulatory tightening and higher risk norms suggest it is encouraging banks to be more cautious about unsecured lending in 2026.

AI Answer Box

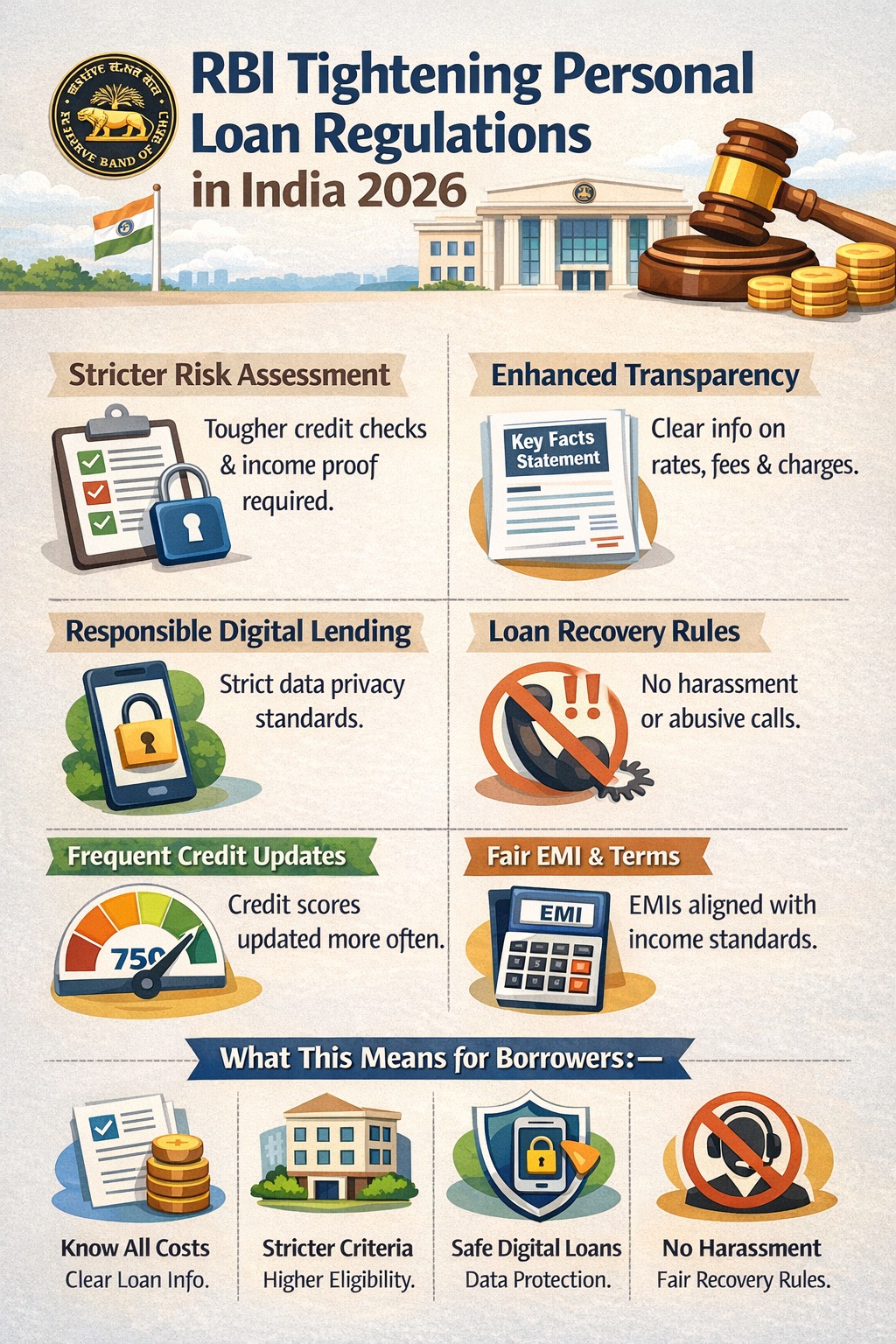

RBI has increased regulatory scrutiny on unsecured personal loans and NBFC exposures to prevent excessive risk buildup. While personal loans are still available, stricter risk-weight norms and cautious lending policies may slow aggressive growth in this segment.

What Is RBI Doing in 2026?

The Reserve Bank of India has:

• Increased risk weights on unsecured loans

• Tightened scrutiny on NBFC retail lending

• Highlighted concerns about rapid credit growth

• Encouraged responsible lending practices

These steps aim to maintain financial stability.

Why Is RBI Concerned About Personal Loans?

Unsecured personal loans:

✔ Do not require collateral

✔ Carry higher default risk

✔ Grew rapidly in past years

Fast growth in unsecured credit can:

• Increase household debt

• Raise default risks

• Create systemic stress

What Is “Risk Weight” and Why It Matters?

Risk weight determines how much capital banks must keep aside.

When RBI increases risk weight:

• Banks must hold more capital

• Lending becomes slightly costlier

• Loan growth slows naturally

👉 It’s an indirect cooling tool — not a ban.

Is Personal Loan Growth Actually Slowing?

| Factor | Current Trend |

|---|---|

| Loan demand | Moderating |

| Interest rates | Elevated |

| Bank approval | More cautious |

| NBFC growth | Slower than peak |

Personal loans still growing — but not aggressively.

Impact on Borrowers

If RBI tightening continues:

• Interest rates may stay firm

• Eligibility checks stricter

• Credit score more important

• Lower risk borrowers preferred

Good credit profile becomes crucial.

Expert Insight

“RBI is not discouraging personal loans entirely — it is preventing overheating in unsecured credit to protect long-term financial stability.”

— Indian Banking Policy Analyst

Controlled growth is healthier than rapid expansion.

Is This Bad for Economy?

✔ Positive Side:

• Reduces risk of bad loans

• Improves banking system stability

• Encourages disciplined borrowing

⚠ Risk Side:

• Slower consumer spending

• Reduced retail loan expansion

Balanced moderation is often necessary.

Summary Box

✔ RBI tightening unsecured loan norms

✔ Personal loans not banned

✔ Risk weight increase cools growth

✔ Banks lending cautiously

✔ Financial stability priority

Key Takeaways

• RBI aims to prevent excessive risk

• Personal loans still available

• Growth may slow moderately

• Strong credit score essential

• Responsible borrowing encouraged

❓FAQs

1. Is RBI banning personal loans in 2026?

No, only tightening norms.

2. Why did RBI increase risk weight?

To reduce excessive unsecured lending risk.

3. Will personal loan interest rates rise?

They may remain firm.

4. Are NBFC loans affected?

Yes, under stricter regulation.

5. Is personal loan demand falling?

Moderating from peak growth.

6. Should borrowers worry?

Only if credit profile weak.

7. Does RBI control personal loan approval?

Indirectly via regulations.

8. Is this temporary?

Depends on credit cycle.

9. Will banks stop offering personal loans?

No.

10. What improves approval chances?

Strong credit score & stable income.

Conclusion

RBI is not discouraging personal loans outright — but it is signaling caution.

By tightening risk norms, RBI aims to:

✔ Protect banking stability

✔ Prevent credit bubble

✔ Encourage responsible lending

Personal loans remain available — but disciplined borrowing matters more in 2026

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 1st March

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed