Applying for a home loan, personal loan or education loan jointly with a spouse or a parent has become increasingly common.

A joint loan can help increase your loan amount, reduce EMI pressure and improve approval chances — but it can also create shared liabilities that may affect the entire family.

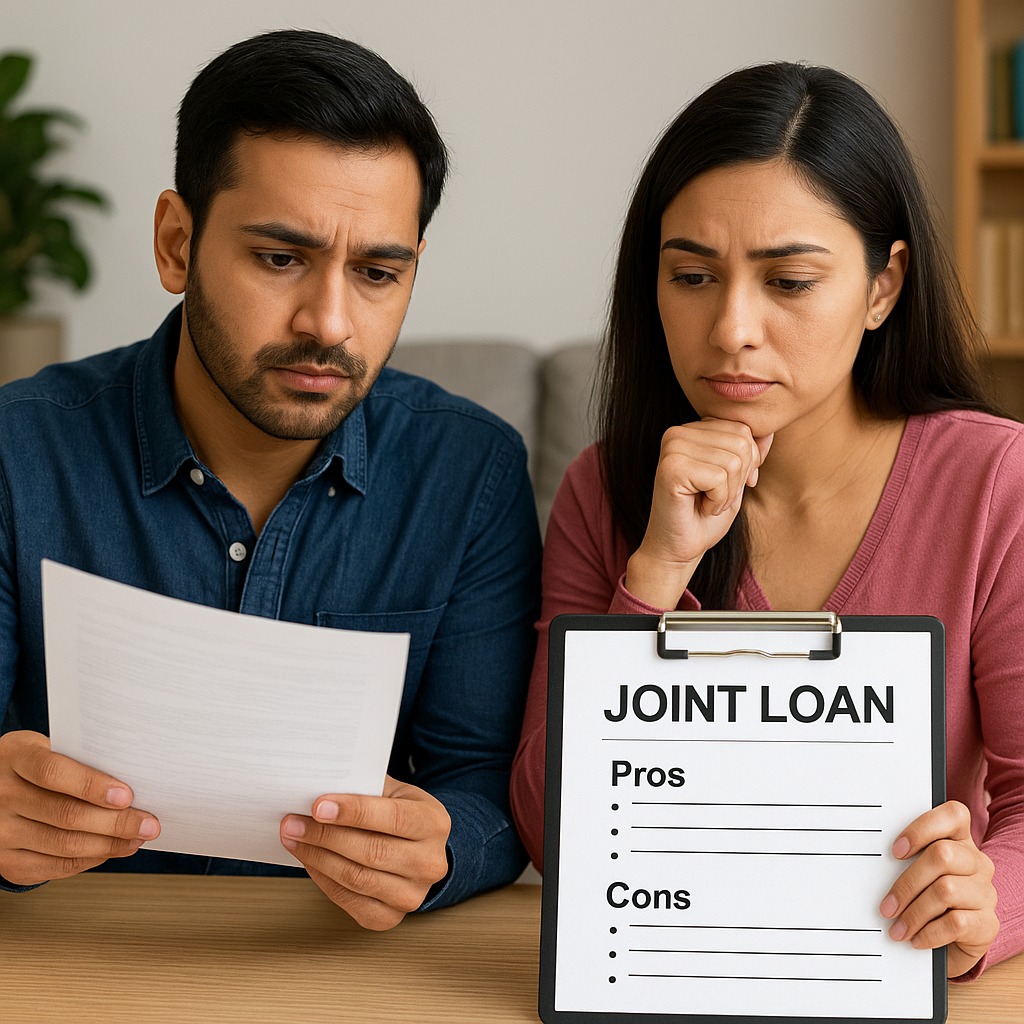

Before signing a joint loan document, it’s essential to understand whether it truly benefits you.

Here’s a complete breakdown.

What Is a Joint Loan?

A joint loan is when two people apply for one loan together.

Both co-applicants share:

EMI responsibility

Liability for defaults

Credit score impact

Loan ownership benefits

Common joint loan types:

✔ Home Loan

✔ Personal Loan

✔ Education Loan

✔ Car Loan

Most joint loans involve spouse, parents, or sometimes siblings.

Pros of Taking a Joint Loan

1. Higher Loan Eligibility

When two incomes are combined, the bank approves a higher loan amount.

Useful for:

Buying a bigger home

Reducing down payment

Getting better property options

2. Lower EMI Burden

If both contribute, monthly EMIs become easier to manage.

Some families split EMIs 50-50.

3. Better Approval Chances

A co-applicant with stable income or strong credit score increases approval probability, especially if your credit score is low.

4. Tax Benefits (Specifically for Home Loans)

If both co-applicants are co-owners:

Each can claim tax benefits on principal (Sec 80C)

And interest (Sec 24)

This can reduce total tax liability significantly.

5. Stronger Financial Backup

If one borrower faces job loss or illness, the other can temporarily handle EMIs.

This reduces the risk of default.

Cons of Taking a Joint Loan

1. Both Are 100% Liable

Even though two people share the loan, each one is fully responsible for EMI payment.

If your spouse or parent misses their share — YOU must pay the entire EMI.

2. Credit Score Risk for Both

Any one of these situations will damage both credit scores:

Late EMI

Missed payment

Outstanding dues

Default affects the entire household financially.

3. Emotional & Family Conflicts

Money + family = friction potential.

Disagreements about EMI contribution, sudden financial changes or loan burden can strain relationships.

4. Reduced Loan Eligibility in Future

Banks consider existing joint EMIs while approving new loans — even if YOU are not paying them.

This reduces personal loan or credit card eligibility later.

5. If One Applicant Dies, Liability Stays

The surviving borrower must continue full EMI payments.

Unless you have credit life insurance, this can become a major financial shock.

Joint Loan: Spouse vs Parents — Which Is Better?

Joint Loan With Spouse

Best When:

✔ Both are working

✔ Stable dual income

✔ Buying a home together

✔ Looking for tax benefits

Risk:

Marital disputes or job loss can complicate repayment.

Joint Loan With Parents

Best When:

✔ Parents have stable pension/income

✔ You need higher loan eligibility

✔ Parents want to be co-owners of property

Risk:

If parents are older, banks may:

Shorten tenure

Increase EMI

Increase insurance cost

Also, liability may fall entirely on you if they cannot pay.

When You SHOULD Take a Joint Loan

✔ Buying a home where both will share ownership

✔ Both incomes are stable

✔ Credit score needs strengthening

✔ You want maximum tax benefits

✔ You need higher loan eligibility

When You SHOULD NOT Take a Joint Loan

✘ If the co-applicant has unstable income

✘ If their credit score is poor

✘ If you expect difficulty in repaying EMIs

✘ If the co-applicant is elderly

✘ If taking higher loan will strain your finances

FAQs

Q1. Does taking a joint loan improve loan approval?

Yes, combining two incomes increases approval chances.

Q2. Will default by one person affect the other?

Absolutely. Both credit scores will drop.

Q3. Can we split EMIs?

Yes, but banks treat the loan as a shared 100% responsibility.

Q4. Do both applicants get tax benefits?

Only if both are co-owners of the property.

Q5. Is a joint loan mandatory for higher home loan eligibility?

Not mandatory, but often the easiest way to increase eligibility.

Published on : 15th November

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed