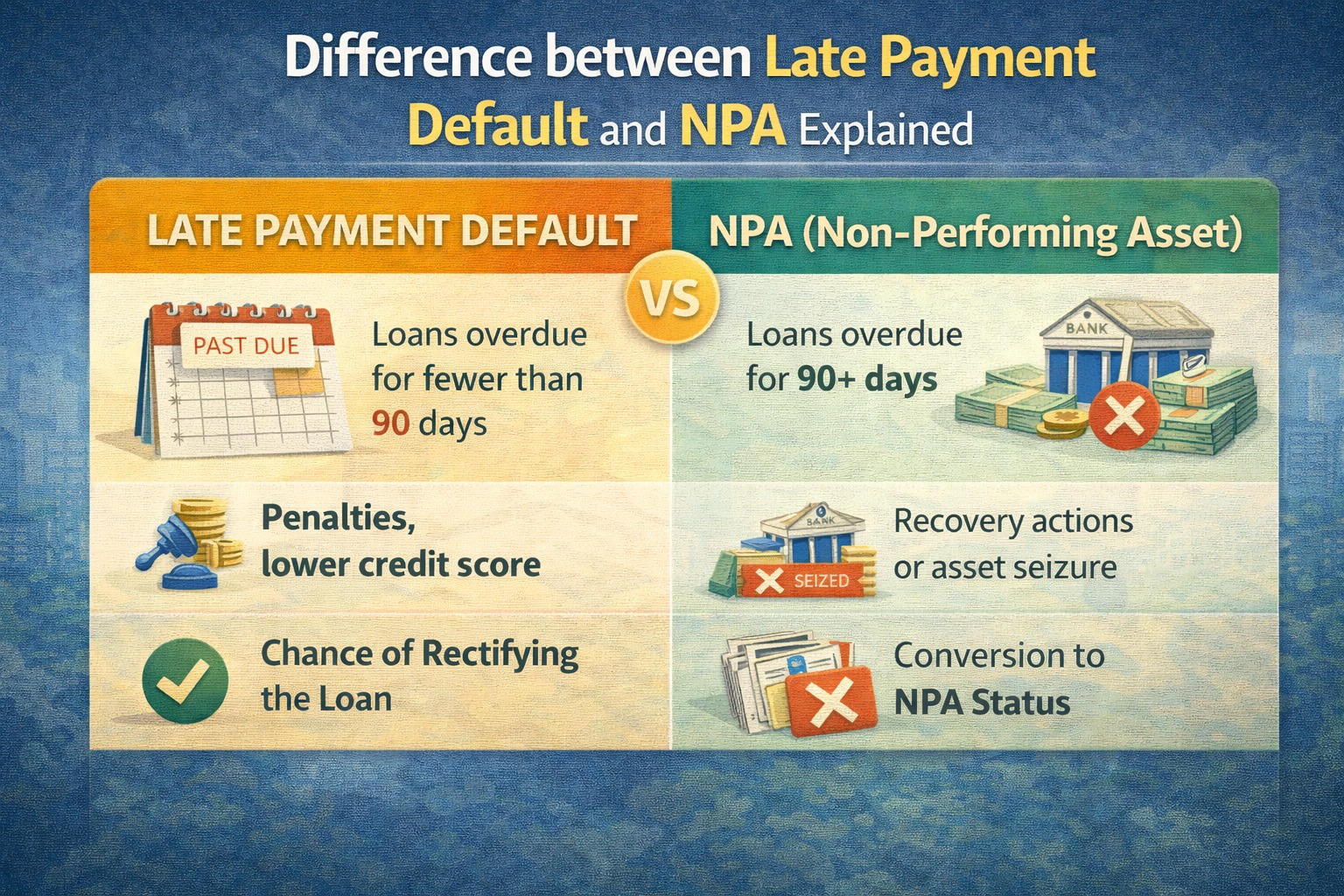

A late payment is a short delay, default is repeated non-payment, and NPA is a bank classification when a loan remains unpaid for 90 days or more. Each stage has increasing financial and credit consequences.

AI Answer Box

Late payment means a delayed EMI, default means failure to repay as agreed, and NPA (Non-Performing Asset) is a loan classified by banks after 90 days of non-payment. The impact on credit score and recovery action increases at each stage.

Why Borrowers Get Confused

Many borrowers use these terms interchangeably, but banks and credit bureaus treat them very differently.

Understanding the difference helps you act early and protect your credit score.

What Is a Late Payment?

A late payment happens when:

EMI is paid after the due date

Delay is usually 1–30 days

Key Characteristics:

EMI eventually gets paid

Late fee or penalty applies

Credit score impact is minor (initially)

Example:

EMI due on 5th → paid on 12th = Late Payment

What Is a Default?

A default occurs when:

EMIs are missed repeatedly

Payment remains unpaid for 30–90 days

Key Characteristics:

Loan is considered at risk

Credit score drops sharply

Recovery calls may start

Example:

EMI unpaid for 2 consecutive months = Default

What Is an NPA (Non-Performing Asset)?

A loan becomes NPA when:

EMI remains unpaid for 90 days or more

Bank classifies the loan as non-performing

Key Characteristics:

Severe credit score damage

Legal or recovery action may begin

Future loan approvals become difficult

Example:

EMI unpaid for 3 months = Loan becomes NPA

NPA vs Default vs Late Payment (Simple Table)

| Factor | Late Payment | Default | NPA |

|---|---|---|---|

| Delay period | 1–30 days | 30–90 days | 90+ days |

| EMI paid later? | Yes | Usually no | No |

| Bank classification | Normal | High risk | Non-performing |

| Credit score impact | Low–Moderate | High | Severe |

| Recovery action | No | Calls & reminders | Legal / recovery |

How a Loan Deteriorates (Timeline)

Due date missed → Late payment

Multiple EMIs missed → Default

90 days unpaid → NPA

👉 Early action can stop the slide.

Why NPA Is Dangerous for Borrowers

Once a loan becomes NPA:

Credit score may drop 100+ points

New loans/cards become difficult

Settlements & legal notices may follow

Recovery agencies may get involved

Expert Insight

“Most NPAs start as small delays. Borrowers who communicate early and regularize payments can avoid long-term financial damage.”

— Retail Credit Risk Analyst

How to Prevent Late Payment Turning Into NPA

Smart Borrower Actions:

Set auto-debit reminders

Maintain EMI buffer (1–2 months)

Inform lender early if facing difficulty

Avoid ignoring calls or notices

Restructure or prepay if possible

Late Payment Myths (Busted)

❌ “One missed EMI doesn’t matter”

✅ It matters if repeated

❌ “NPA happens suddenly”

✅ It takes 90 days of neglect

❌ “Credit score recovers automatically”

✅ Recovery takes months or years

Key Takeaways

Late payment is a warning

Default is a serious risk signal

NPA is a major financial setback

Early action prevents long-term damage

Discipline protects credit health

Conclusion

Late payment, default, and NPA are not the same — they are stages of worsening repayment behavior. What starts as a small delay can turn into a major financial problem if ignored. Borrowers who act early, communicate with lenders, and manage EMIs responsibly can avoid NPA and protect their financial future.

Frequently Asked Questions (FAQs)

1. Is one late EMI considered default?

No. Default usually means repeated non-payment.

2. When does a loan become NPA?

After 90 days of continuous non-payment.

3. Does late payment affect credit score?

Yes, but the impact is smaller than default or NPA.

4. Can an NPA loan be revived?

Yes, through repayment, restructuring, or settlement.

5. Is default reported to credit bureaus?

Yes, defaults significantly damage credit scores.

6. Can banks take legal action for NPA?

Yes, especially for large or secured loans.

7. Does auto-debit failure count as late payment?

Yes, unless corrected immediately.

8. How long does NPA stay on credit report?

It can affect credit history for several years.

9. Can communication prevent NPA?

Yes. Early discussion helps in restructuring.

10. What’s the safest way to avoid all three?

Maintain EMI buffer and repay on time

Published on : 16th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed