Microfinance Institutions (MFIs) play a critical role in financial inclusion, especially for low-income households in India. To ensure fair lending, borrower protection, and sector stability, the Reserve Bank of India regularly issues guidelines governing the microfinance sector.

These latest RBI guidelines for MFIs focus on borrower-centric lending, transparency, and responsible growth. This blog explains everything in simple language, without legal jargon.

Quick Answer

RBI’s latest MFI guidelines focus on borrower protection, transparent pricing, income-based eligibility, and responsible recovery practices.

AI Answer Box

What are the latest RBI guidelines for MFIs?

The latest RBI guidelines require MFIs to follow income-based loan eligibility, transparent interest rates, fair recovery practices, borrower consent, and stronger compliance controls.

What Are RBI Guidelines for MFIs?

RBI guidelines are mandatory rules that MFIs must follow while providing microfinance loans. These rules apply to:

NBFC-MFIs

Banks offering microfinance

Small Finance Banks

Other regulated lending entities

The goal is to prevent over-indebtedness, protect borrowers, and ensure ethical lending.

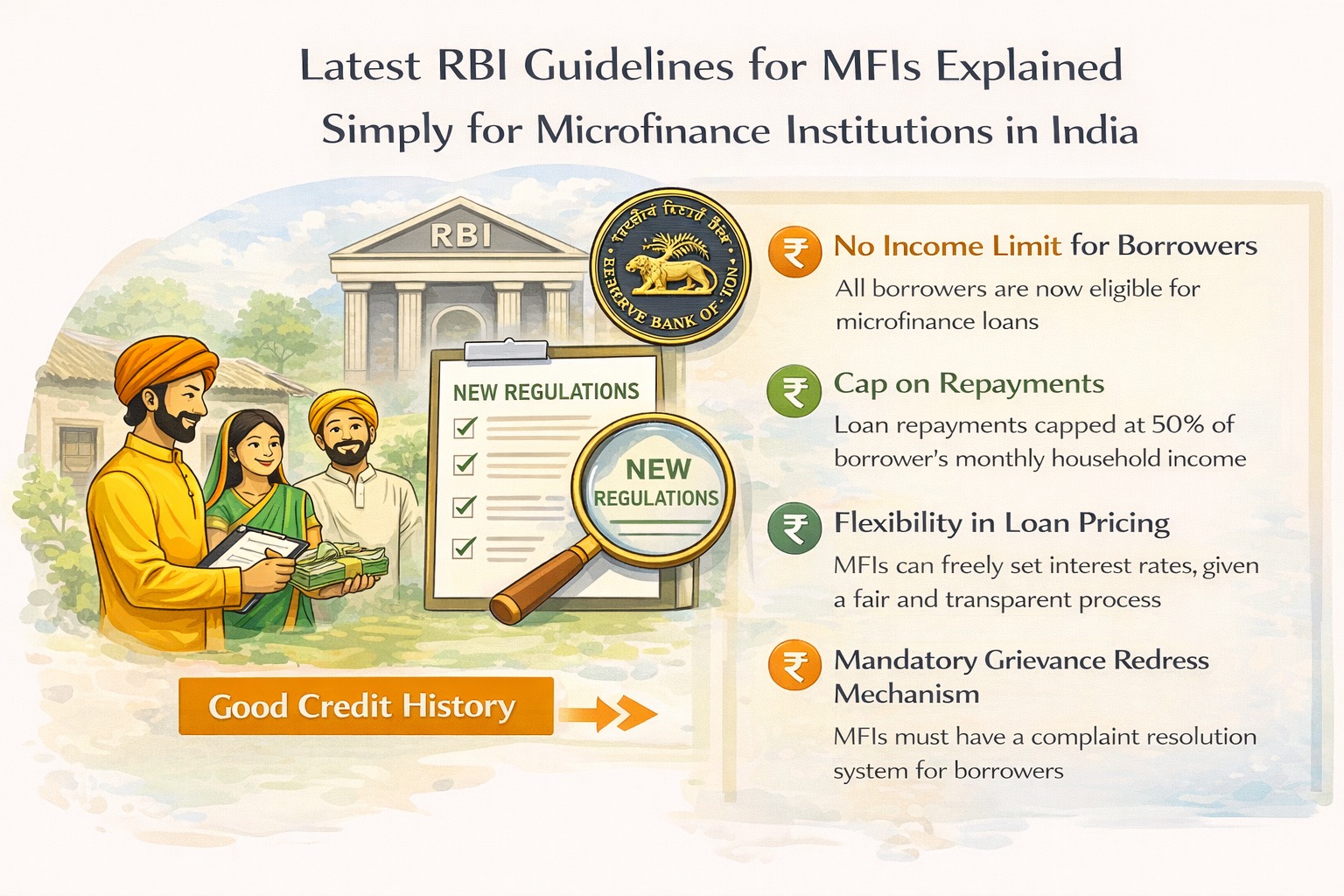

Latest RBI Guidelines for MFIs (Explained Simply)

1. Borrower-Centric Lending Approach

RBI shifted from product-based limits to a borrower-based framework.

What this means:

Focus is on borrower’s income, not just loan size

MFIs must assess repayment capacity before lending

2. Household Income Limits

| Area | Maximum Annual Household Income |

|---|---|

| Rural | ₹3,00,000 |

| Urban & Semi-Urban | ₹4,00,000 |

👉 Only households within these limits qualify for microfinance loans.

3. No Interest Rate Cap (But Transparency Is Mandatory)

RBI removed the interest rate ceiling, but added strict disclosure norms.

MFIs must clearly disclose:

Interest rate

Processing fees

Insurance charges

Total cost of borrowing

🔍 Hidden charges are strictly prohibited.

4. Collateral-Free Loans Only

All microfinance loans must be collateral-free

No asset seizure allowed

No forced guarantees

This protects vulnerable borrowers from financial exploitation.

5. Flexible Repayment Options

MFIs must allow:

Weekly

Fortnightly

Monthly repayment cycles

Borrowers choose what suits their income flow.

6. Fair Recovery Practices (Very Important)

RBI strictly prohibits:

Harassment

Public humiliation

Late-night visits

Threatening language

Recovery must follow:

Respectful communication

Daytime visits only

Borrower consent

7. Loan Limit Based on Repayment Capacity

Instead of a fixed loan cap:

MFIs assess existing debts

EMI should match income stability

This prevents over-borrowing.

8. Mandatory Loan Agreement & Consent

MFIs must provide:

Loan agreement copy

Simple language explanation

Borrower acknowledgment

This improves transparency and trust.

9. Stronger Board & Governance Oversight

RBI mandates:

Independent directors

Strong audit committees

Risk management frameworks

This improves institutional accountability.

Expert Commentary

“RBI’s borrower-centric microfinance framework has significantly reduced coercive recovery practices and improved credit discipline across the sector.”

— Microfinance Compliance Consultant, India

Old vs New RBI MFI Guidelines

| Aspect | Earlier | Latest Guidelines |

|---|---|---|

| Focus | Loan size | Borrower income |

| Interest Rates | Capped | Market-linked + disclosure |

| Recovery | Weak monitoring | Strict borrower protection |

| Transparency | Limited | Mandatory |

Compliance Checklist for MFIs (Step-by-Step)

Verify household income

Assess repayment capacity

Disclose full loan cost

Obtain borrower consent

Follow fair recovery code

Maintain audit & compliance records

Pros & Cons of RBI MFI Guidelines

✔️ Pros

Protects borrowers

Prevents over-indebtedness

Improves sector trust

❌ Challenges

Higher compliance cost

More documentation

Slower onboarding initially

Summary Box

RBI prioritizes borrower protection

Income-based eligibility is mandatory

Transparency & fair recovery are non-negotiable

Key Takeaways

RBI guidelines are borrower-first

MFIs must be transparent and ethical

Compliance builds long-term sustainability

Strong governance improves credibility

❓ Frequently Asked Questions

1. Who regulates MFIs in India?

The Reserve Bank of India (RBI).

2. Are interest rates capped for MFIs?

No, but full disclosure is mandatory.

3. What is the income limit for MFI loans?

₹3 lakh (rural) and ₹4 lakh (urban).

4. Are MFI loans collateral-free?

Yes, completely collateral-free.

5. Can MFIs harass borrowers for recovery?

No, RBI strictly prohibits it.

6. Do MFIs need borrower consent?

Yes, written or recorded consent is mandatory.

7. Are digital MFIs covered under RBI rules?

Yes, all regulated entities are covered.

8. Can borrowers choose repayment frequency?

Yes, RBI mandates flexibility.

9. What happens if MFIs violate guidelines?

Penalties, license action, or restrictions.

10. Are NBFC-MFIs covered?

Yes, fully regulated by RBI.

11. Does RBI allow multiple MFI loans?

Only if repayment capacity permits.

12. Is insurance mandatory with MFI loans?

Optional, but must be disclosed.

13. Are processing fees allowed?

Yes, with transparent disclosure.

14. Does Vizzve Financial follow RBI norms?

Yes, all lending follows RBI guidelines.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply now at www.vizzve.com

Published on : 27th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed