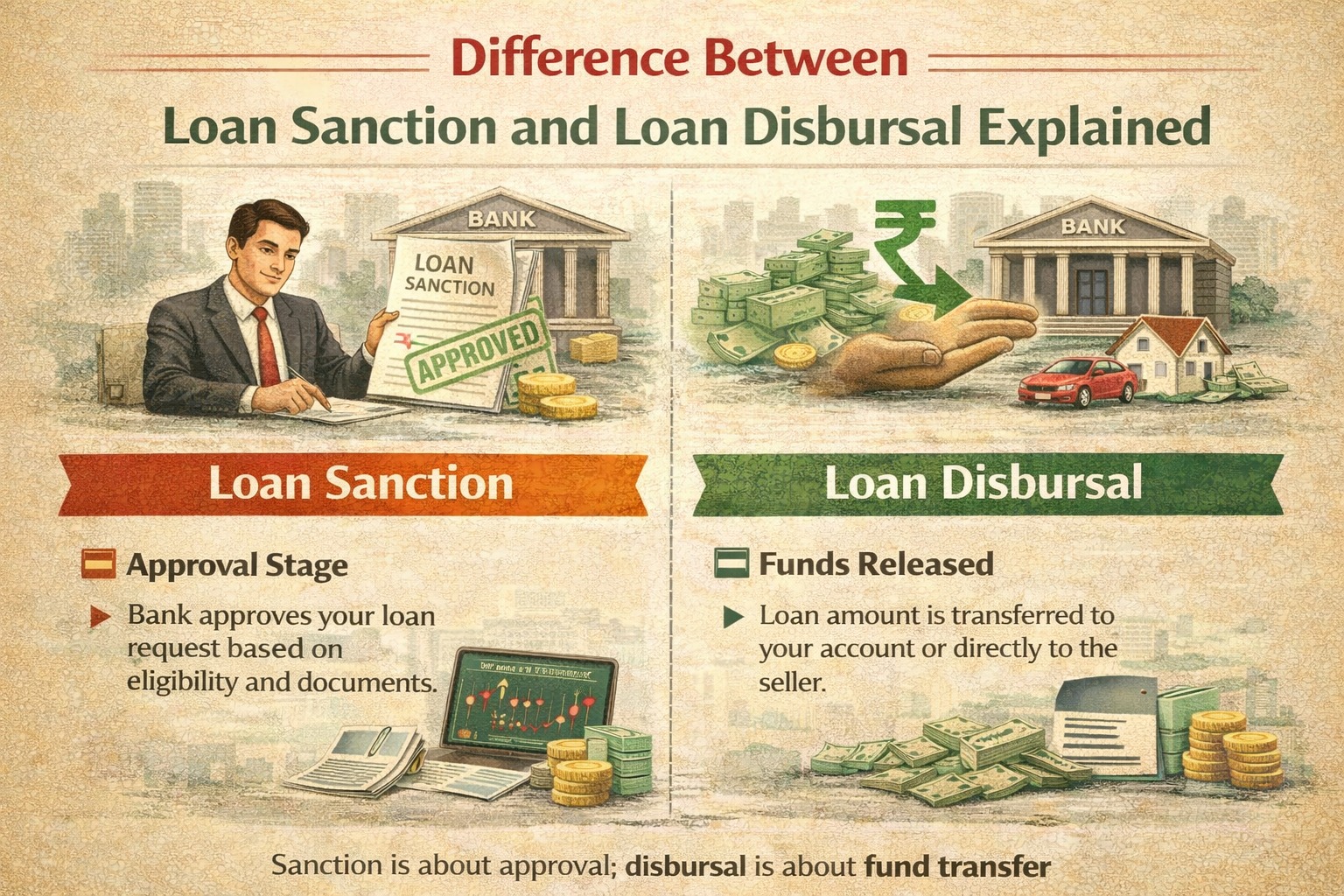

Loan sanction means the lender has approved your loan amount and terms, while loan disbursal means the actual money is released to you or the seller. Sanction is a promise, disbursal is the payment.

AI Answer Box

Loan sanction vs loan disbursal:

Sanction = approval of loan

Disbursal = release of funds

Sanction comes first

Disbursal depends on conditions

Money is received only after disbursal

🔹 Introduction

Many borrowers assume that once a loan is sanctioned, the money will immediately reach their bank account. This is one of the most common misunderstandings in the loan process.

In reality, loan sanction and loan disbursal are two very different stages. Knowing the difference can help you avoid delays, stress, and poor financial planning—especially for home loans, education loans, and business loans.

Let’s clearly understand how both work.

🔹 What Is Loan Sanction?

Loan sanction is the stage where the lender:

Approves your loan application

Confirms the loan amount

Fixes interest rate, tenure, and EMI

Issues a sanction letter

What a Sanction Letter Includes:

Approved loan amount

Interest rate (fixed/floating)

Tenure and EMI

Conditions to be fulfilled

Validity period (usually 3–6 months)

📌 Important:

Loan sanction does not mean money is credited.

🔹 What Is Loan Disbursal?

Loan disbursal is the stage where:

The lender releases the loan amount

Funds are credited to your bank account or directly to the seller/builder

The loan officially starts

Only after disbursal:

EMIs begin

Interest starts accruing

🔹 Loan Sanction vs Loan Disbursal: Key Differences

| Aspect | Loan Sanction | Loan Disbursal |

|---|---|---|

| Meaning | Loan approval | Release of funds |

| Money received | ❌ No | ✅ Yes |

| Documents | Income, credit check | Legal & final docs |

| EMI start | ❌ No | ✅ Yes |

| Can be cancelled | Yes | Difficult |

| Stage | First | Final |

🔹 Why There Is a Gap Between Sanction & Disbursal

Common Reasons:

Pending documents

Property legal verification (home loans)

Down payment not paid

Agreement not signed

Disbursal conditions not met

This gap can range from a few hours to several months, depending on loan type.

🔹 Example: Home Loan Scenario

Loan sanctioned for ₹50 lakh

Builder agreement pending

Property registration incomplete

➡️ Loan is sanctioned but disbursal is delayed until documents are completed.

🔹 Example: Personal Loan Scenario

Loan sanctioned instantly

KYC and mandate completed

Disbursal happens within hours or same day

➡️ Shorter gap compared to secured loans.

🔹 Can a Sanctioned Loan Be Cancelled?

Yes, if:

Borrower changes mind

Better loan offer found

Conditions not fulfilled

📌 No EMI or interest applies if loan is not disbursed.

🔹 Does Credit Score Matter After Sanction?

Yes. If there is a long delay between sanction and disbursal:

Fresh credit checks may happen

New loans or missed EMIs can affect final disbursal

Lenders follow guidelines influenced by the Reserve Bank of India for risk management.

🔹 Borrower Mistakes to Avoid

🚫 Spending assuming loan is credited

🚫 Ignoring sanction validity

🚫 Taking new loans after sanction

🚫 Delaying document submission

🔹 Real-World Borrower Insight (EEAT Boost)

From loan processing trends, many disbursal delays happen not due to banks, but due to incomplete borrower documentation or property-related formalities. Prepared borrowers receive faster disbursals—even with average income.

🔹 Pros & Cons (Borrower Perspective)

Loan Sanction

Pros: Certainty of approval

Cons: No cash in hand

Loan Disbursal

Pros: Funds available

Cons: EMI obligation starts

🔹 Key Takeaways

Sanction ≠ money received

Disbursal is the actual loan payout

Sanction comes first, disbursal later

EMIs start only after disbursal

Planning between stages is crucial

🔹 Frequently Asked Questions (FAQs)

1. Is loan sanction the same as approval?

Yes.

2. Will I get money after sanction?

No, only after disbursal.

3. Can disbursal be delayed after sanction?

Yes.

4. Do EMIs start after sanction?

No, after disbursal.

5. Can bank reject loan after sanction?

Rare, but possible if conditions fail.

6. How long does disbursal take?

Hours to months, depending on loan type.

7. Can I cancel a sanctioned loan?

Yes, before disbursal.

8. Is sanction letter legally binding?

It’s conditional.

9. Does interest start after sanction?

No.

10. Is disbursal automatic?

Only after conditions are met.

11. Can partial disbursal happen?

Yes, especially in home loans.

12. Should I spend before disbursal?

No.

🔹 Conclusion + CTA

Understanding the difference between loan sanction and loan disbursal helps you plan cash flow better and avoid last-minute surprises. Remember—approval is not money. Funds come only after final disbursal.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Published on : 8th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed