For years, financial success was often mistaken for easy access to credit.

More cards. Bigger limits. Faster loans.

But 2026 flips that thinking.

With higher interest rates, tighter credit checks, and visible credit behaviour, the focus is shifting from how much you can borrow to how well your debt is structured.

In today’s environment, debt quality matters more than debt quantity.

AI Answer Box

In 2026, borrowers should focus on debt quality rather than borrowing more. A healthy balance between loans and savings improves financial stability, reduces EMI stress, and protects long-term credit health.

Quick Summary Box

Borrowing more is not financial strength

Quality of debt matters more than volume

Savings protect EMI stability

Poor debt structure increases risk

2026 rewards disciplined borrowers

Why “Borrowing Capacity” Is No Longer the Goal

Earlier, borrowers aimed to:

Maximise loan eligibility

Use full credit limits

Stack multiple loans

In 2026, this approach backfires because:

EMIs face inflation pressure

Credit scores update faster

Lenders monitor repayment capacity closely

Borrowing capacity without savings is fragile.

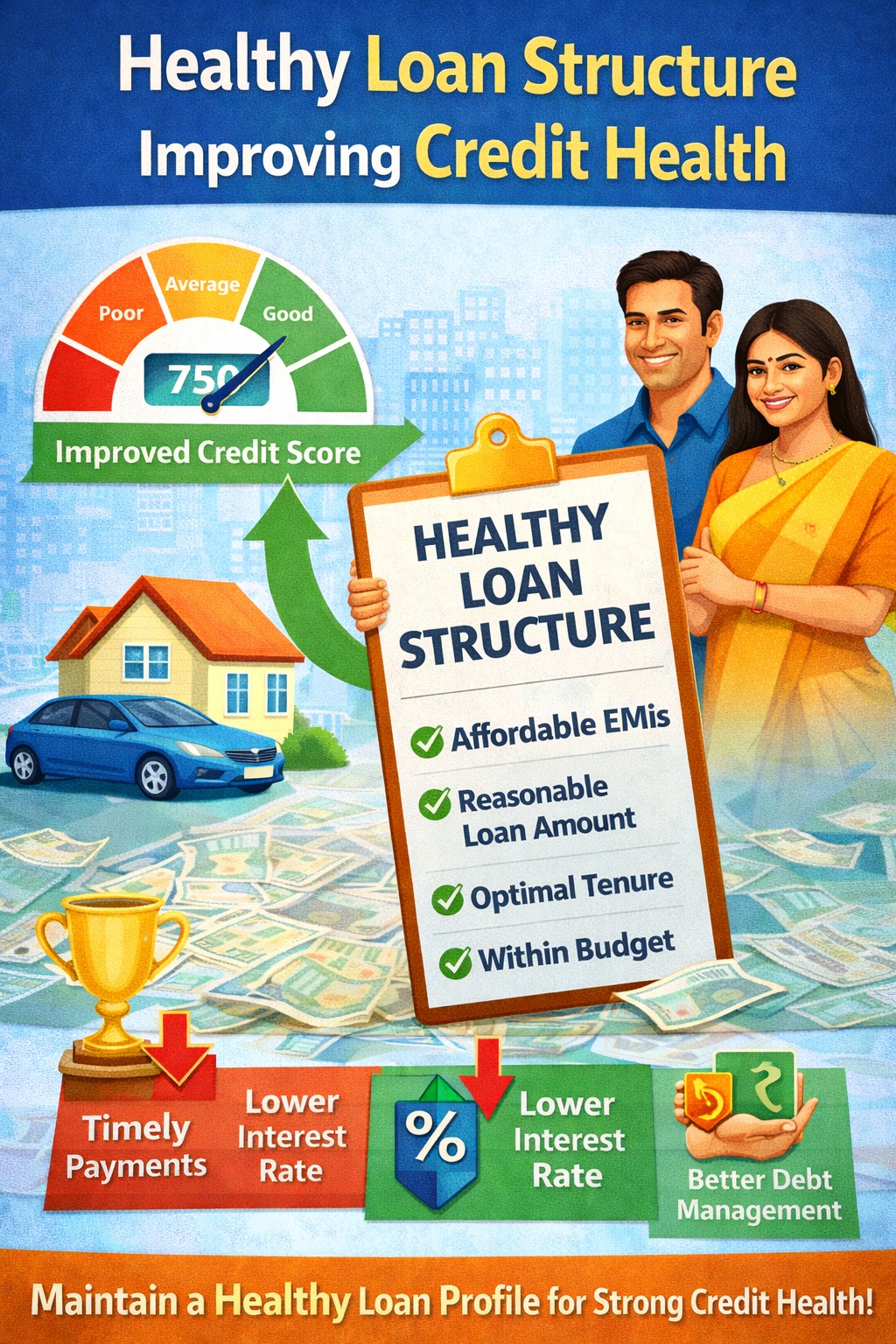

What Is Debt Quality?

Debt quality refers to how healthy your borrowing is, not how much it is.

High-Quality Debt Looks Like:

Affordable EMIs

Clear purpose

Shorter or optimised tenure

Prepayment flexibility

Backed by savings buffer

Low-Quality Debt Looks Like:

Overlapping EMIs

Lifestyle-driven loans

Minimum-only payments

No emergency fund

Debt Quantity vs Debt Quality

| Aspect | Debt Quantity | Debt Quality |

|---|---|---|

| Focus | How much borrowed | How well structured |

| EMI stress | High | Controlled |

| Savings buffer | Weak | Strong |

| Credit health | Volatile | Stable |

| Financial resilience | Low | High |

Why Savings Matter More in 2026

With:

Sticky interest rates

Inflation pressure

Currency uncertainty

savings act as:

EMI shock absorbers

Credit profile stabilisers

Negotiation power with lenders

A borrower with moderate debt + strong savings is safer than one with high borrowing and no buffer.

The Hidden Risk of Borrowing “Just Because You Can”

Many borrowers fall into the trap of:

Pre-approved loan offers

High credit card limits

Easy digital approvals

This creates:

Artificial affordability

Long-term EMI stress

Reduced flexibility during emergencies

In 2026, easy credit is not cheap credit.

How to Balance Loans and Savings in 2026

Smart Financial Framework:

Maintain 6 months of expenses as emergency savings

Keep EMIs below 35–40% of income

Avoid overlapping personal loans

Prefer prepayable, flexible loans

Increase savings before increasing borrowing

Ideal Loan–Savings Balance Checklist

| Area | Healthy Range |

|---|---|

| EMI-to-income | < 40% |

| Emergency fund | 6 months |

| Loan purpose | Need-based |

| Credit utilisation | < 30% |

| Savings growth | Ongoing |

Expert Commentary: Strong Borrowers Are Liquid Borrowers

“In today’s economy, liquidity matters more than leverage. Borrowers with savings survive shocks better than borrowers with high limits.”

— Personal Finance & Credit Analyst

What Happens If You Ignore Debt Quality?

Rising EMI stress

Credit score volatility

Reduced loan flexibility

Forced borrowing during emergencies

Long-term financial fatigue

Poor debt quality doesn’t fail immediately—it erodes stability quietly.

Key Takeaways

2026 rewards disciplined borrowing

Debt quality matters more than loan size

Savings protect both EMIs and credit score

Borrowing should support life, not strain it

Financial strength = balance, not leverage

❓ Frequently Asked Questions (FAQs)

1. What does debt quality mean?

It means how affordable, planned, and flexible your loans are.

2. Is borrowing bad in 2026?

No—over-borrowing is bad, not borrowing itself.

3. How much EMI is safe?

Ideally below 35–40% of monthly income.

4. Should I save or repay loans first?

Maintain emergency savings, then balance repayment.

5. Are pre-approved loans safe?

Only if they fit your budget and purpose.

6. Does savings affect loan approval?

Indirectly, yes—liquidity improves risk profile.

7. Is having no debt better?

Not always—healthy debt can support goals.

8. What’s the biggest mistake borrowers make?

Borrowing without a savings buffer.

Conclusion: In 2026, Quality Beats Quantity

The financial lesson of 2026 is clear:

It’s not about how much debt you can carry—it’s about how well you carry it.

Borrowers who balance loans with savings, structure debt wisely, and leave room for uncertainty will stay ahead—financially and mentally.

📌 In the new borrowing era, stability is the new success metric.

Published on : 2nd January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed