You see two loan offers:

Offer A: Very low EMI

Offer B: Lower interest rate

Most borrowers instinctively pick low EMI.

And that’s exactly how many end up paying much more than expected.

In reality, low EMI and low interest are NOT the same thing—and confusing the two is one of the costliest borrowing mistakes people make.

This blog explains the real difference between low EMI and low interest, with simple examples, so you can choose loans smartly—not emotionally.

AI Answer Box

What is the difference between low EMI and low interest?

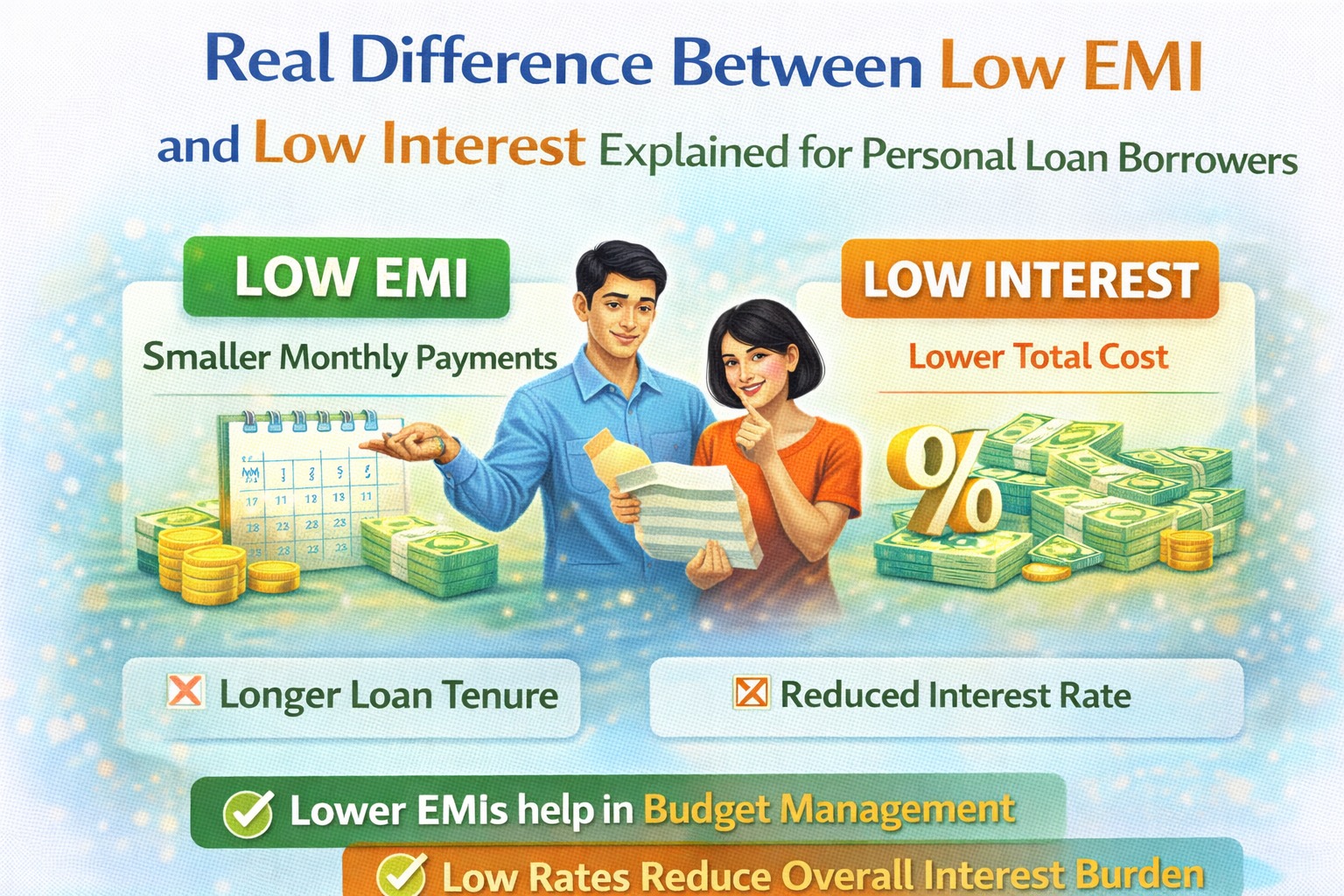

Low EMI usually results from a longer loan tenure, which can increase total interest paid. Low interest reduces the overall loan cost. A low EMI loan is easier monthly, but often more expensive overall.

Key insight:

Low EMI feels comfortable monthly—but low interest saves money long-term.

Quick Summary Box

| Term | What It Really Means |

|---|---|

| Low EMI | Lower monthly payment |

| Low interest | Lower total cost |

| Longer tenure | More interest paid |

| Shorter tenure | Higher EMI, less cost |

| Best loan | Balance of both |

WHY BORROWERS CONFUSE LOW EMI WITH CHEAP LOANS

Most people think:

“If my EMI is low, the loan must be affordable.”

But affordable monthly ≠ cheaper overall.

Lenders often reduce EMI by:

Increasing tenure

Not reducing interest rate

📌 That’s where the trap lies.

WHAT IS LOW EMI — REALLY?

A low EMI loan usually means:

Longer repayment period

Same or higher interest rate

Example:

Loan amount: ₹5,00,000

Interest rate: 14%

Tenure: 5 years instead of 3

✔ EMI reduces

❌ Total interest increases significantly

📌 Low EMI protects monthly cash flow, not total cost.

WHAT IS LOW INTEREST — REALLY?

A low interest loan means:

Lower rate applied to principal

Less interest accumulated over time

Even if:

EMI is slightly higher

Tenure is shorter

📌 You pay much less overall.

REAL COMPARISON: LOW EMI vs LOW INTEREST

Scenario: ₹5,00,000 Personal Loan

| Option | EMI | Tenure | Interest Rate | Total Paid |

|---|---|---|---|---|

| Low EMI Loan | ₹12,000 | 5 yrs | 14% | ₹7.2 lakh |

| Low Interest Loan | ₹15,800 | 3 yrs | 10% | ₹5.7 lakh |

💡 Difference paid: ₹1.5 lakh more for low EMI

📌 Same loan. Very different outcome.

❌ WHY LOW EMI LOANS CAN COST YOU MORE

Low EMI loans often:

Lock you in longer

Accumulate interest for more months

Delay financial freedom

📌 You feel comfortable monthly—but stay in debt longer.

✅ WHEN LOW EMI MAKES SENSE

Low EMI is not bad—when used correctly.

Choose low EMI if:

Income is uncertain

You need strong monthly buffer

It’s a temporary phase

📌 But always check total repayment.

✅ WHEN LOW INTEREST IS BETTER

Low interest works best if:

Income is stable

You can manage slightly higher EMI

You want to close debt faster

📌 This is usually the cheapest option long-term.

HOW SMART BORROWERS CHOOSE (2025–26 RULE)

Smart borrowers don’t ask:

“Which EMI is lowest?”

They ask:

“What is my total cost AND can I live with this EMI?”

Smart Rule:

EMI ≤ 35–40% of income

Tenure as short as comfortably possible

Always compare total amount repaid

Expert Commentary

“Low EMI loans are sold emotionally, low interest loans are chosen rationally. Smart borrowing balances both—not extremes.”

— Personal Finance Advisor, India

Getting the Balance Right With Guidance

Many borrowers overpay simply because nobody explains this difference clearly.

Vizzve Financial helps borrowers:

Compare low EMI vs low interest correctly

Choose EMI based on comfort—not temptation

Understand total cost before applying

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

❓ Frequently Asked Questions (FAQs)

1. Is low EMI always bad?

No—but it usually costs more long-term.

2. Does low interest always mean high EMI?

Not always, but often slightly higher.

3. Which is better for credit score?

Both are fine if EMIs are paid on time.

4. Why do ads highlight EMI instead of interest?

Because EMI feels easier to sell emotionally.

5. Can I prepay a low EMI loan?

Yes, if allowed—check charges.

6. Should I always choose shortest tenure?

Shortest comfortable tenure—not forced.

7. Does tenure affect interest a lot?

Yes—dramatically.

8. Can two loans with same EMI cost differently?

Yes—very often.

9. What should I compare first?

Total repayment amount.

10. Biggest borrower mistake?

Choosing EMI without checking total cost.

Key Takeaways

Low EMI ≠ cheap loan

Low interest reduces total cost

Longer tenure increases interest

EMI comfort and cost must be balanced

Smart borrowing is about clarity, not ads

Conclusion

Low EMI feels good today.

Low interest feels good for years.

The smartest loan choice sits between comfort and cost—not at either extreme.

If you want help comparing loans the right way, not the advertised way, explore borrower-first guidance at www.vizzve.com and make borrowing a confident decision.

Published on : 28th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed