Introduction

MFI loans and bank loans may both provide credit—but they are designed for very different borrowers.

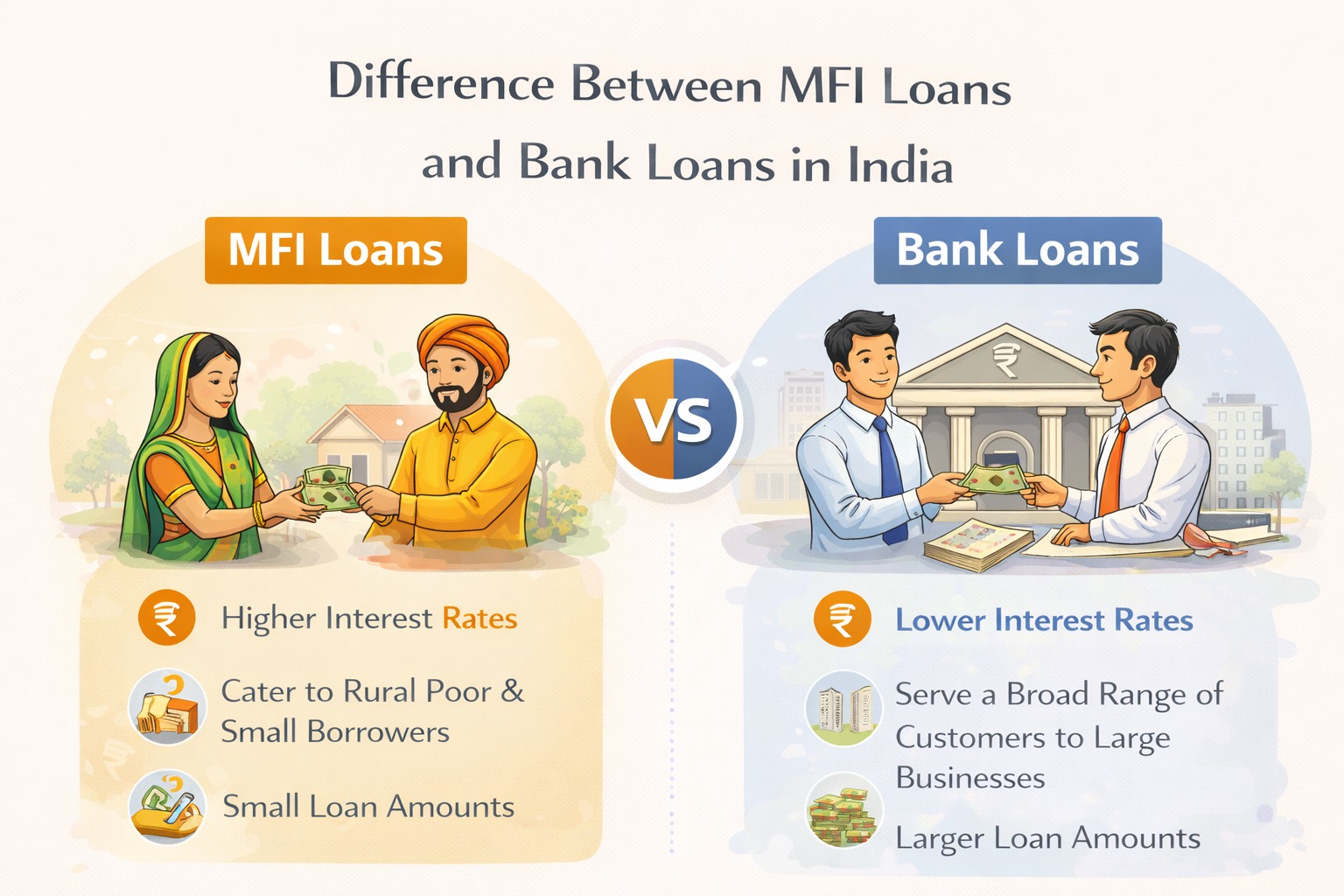

In India, Microfinance Institutions (MFIs) focus on small-ticket, short-term loans for low-income and underserved borrowers, while banks cater to a wider audience with larger, longer-term loans at lower interest rates.

Understanding this difference helps borrowers avoid over-borrowing, high costs, and repayment stress.

AI Answer Box

Short Answer:

MFI loans are small, short-term, unsecured loans meant for low-income borrowers, while bank loans are larger, cheaper, and suited for borrowers with stable income and documentation.

What Are MFI Loans?

MFI loans are provided by Microfinance Institutions, including NBFC-MFIs, to promote financial inclusion.

Key Features of MFI Loans

Small loan amounts

Short tenure

Mostly unsecured

Group-based or individual lending

Weekly or fortnightly repayments

MFIs typically serve:

Low-income households

Informal sector workers

First-time borrowers

Rural and semi-urban customers

MFIs operate under guidelines of the Reserve Bank of India.

What Are Bank Loans?

Bank loans are offered by:

Public sector banks

Private banks

Co-operative banks

Key Features of Bank Loans

Larger loan amounts

Longer tenures

Lower interest rates

Monthly EMI structure

Strong documentation and credit checks

Banks serve:

Salaried individuals

Established businesses

Borrowers with credit history

MFI Loans vs Bank Loans: Key Differences

| Feature | MFI Loans | Bank Loans |

|---|---|---|

| Loan Size | Small (₹10,000–₹1 lakh) | Medium to Large |

| Interest Rates | Higher | Lower |

| Tenure | Short | Medium to Long |

| Repayment | Weekly/Fortnightly | Monthly EMI |

| Credit Score | Often not mandatory | Mandatory |

| Documentation | Minimal | Extensive |

| Target Borrower | Low-income, informal | Salaried/business |

| Purpose | Livelihood, consumption | Assets, growth |

Why MFI Loans Cost More

MFI loans carry higher interest rates because:

No collateral

Higher servicing cost

Frequent collections

Higher borrower risk

📌 Higher rates reflect operational reality, not profiteering.

When MFI Loans Make Sense

MFI loans are suitable if you:

Lack formal income proof

Need small, quick funds

Are first-time borrowers

Live in underbanked areas

When Bank Loans Are Better

Bank loans are ideal if you:

Have stable income

Maintain good credit score

Need larger loan amounts

Prefer lower interest cost

Risks Borrowers Should Understand

MFI Loan Risks

Higher EMI frequency pressure

Loan stacking risk

Higher effective interest cost

Bank Loan Risks

Longer approval time

Strict eligibility

Penalties for defaults

Real-World Borrowing Insight

From borrower behaviour analysis, households with multiple MFI loans often face cash-flow stress, while borrowers who graduate to bank loans see lower EMI burden and better credit health.

How Borrowers Can Transition From MFI to Bank Loans

Step-by-Step Path

Repay MFI loans on time

Avoid multiple parallel loans

Build basic credit history

Open and maintain bank accounts

Apply for bank loans gradually

Impact on Credit Score

| Loan Type | Credit Impact |

|---|---|

| MFI Loans | Builds entry-level credit |

| Bank Loans | Builds long-term credit strength |

📌 Responsible MFI borrowing can be a stepping stone, not a trap.

Key Takeaways

MFI loans focus on inclusion, not scale

Bank loans are cheaper but stricter

Loan size and cost differ significantly

Borrowers should avoid loan stacking

Long-term goal should be formal banking

Frequently Asked Questions

1. Are MFI loans cheaper than bank loans?

No, they are costlier.

2. Do MFI loans need collateral?

No, mostly unsecured.

3. Can MFI borrowers get bank loans?

Yes, over time with good repayment.

4. Do banks accept first-time borrowers?

Rarely, unless income proof exists.

5. Are MFIs regulated?

Yes, by RBI.

6. What is loan stacking?

Multiple small loans simultaneously.

7. Do MFI loans affect credit score?

Yes, positively or negatively.

8. Why are MFI EMIs weekly?

To match borrower cash flow.

9. Are bank loans safer?

Cheaper and structured, yes.

10. Which is faster—MFI or bank loan?

MFI loans.

11. Should MFI loans be long-term?

No, short-term only.

12. Can MFIs offer large loans?

Generally no.

Conclusion: Choose Based on Need, Not Ease

MFI loans and bank loans serve different purposes. MFI credit supports inclusion and emergency needs, while bank loans enable stability and growth.

Smart borrowers use MFI loans as a starting point—and aim to graduate into formal, lower-cost banking credit over time.

Published on : 26th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed