With the rise of digital payments, consumers now have multiple options to manage money — from mobile wallets to bank apps. Both provide convenience, but understanding their features, benefits, and limitations can help you choose the right tool for daily transactions.

What Are Mobile Wallets?

Mobile wallets are apps that store digital money and allow you to pay for goods and services instantly. Examples include Paytm, Google Pay Wallets, PhonePe Wallets, and others.

Key Features:

Preloaded digital cash or linked to a bank account

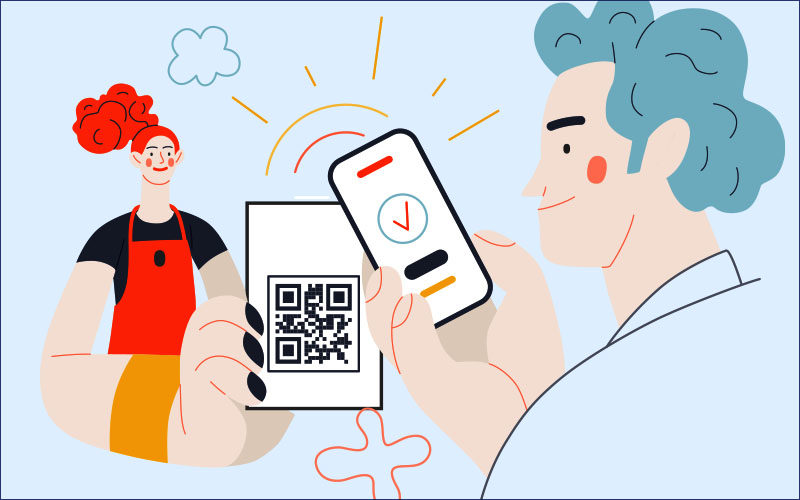

QR code payments at shops, online payments, and peer-to-peer transfers

Loyalty points, cashback, and promotional offers

Benefits:

Quick payments without needing cash or card

User-friendly interface for small, everyday transactions

Incentives like discounts, cashback, or reward points

Limitations:

Usually have transaction limits

Some require internet connectivity

Funds may need to be transferred back to a bank for withdrawals

What Are Bank Apps?

Bank apps are official applications provided by banks to manage accounts digitally. Examples include HDFC MobileBanking, SBI YONO, ICICI iMobile, and others.

Key Features:

Direct access to savings, current, and fixed deposit accounts

Fund transfers via NEFT, RTGS, IMPS

Bill payments, loan EMIs, credit card management, and investment tracking

Benefits:

Full control over bank accounts and transactions

Higher security and regulated by RBI guidelines

Easier management of recurring payments and large transactions

Limitations:

Slightly more complex interface compared to wallets

Some apps may not support instant small payments like QR code scanning in all stores

Mobile Wallets vs Bank Apps: Key Differences

| Feature | Mobile Wallet | Bank App |

|---|---|---|

| Payment Speed | Instant, easy for small transactions | Slightly slower for some interbank transfers |

| Transaction Limits | Often limited | Higher limits, suitable for large payments |

| Rewards & Offers | Cashback, discounts, loyalty points | Rarely offer promotions |

| Security | App-level security, sometimes dependent on wallet provider | Bank-regulated security, robust |

| Usage | Best for everyday small purchases | Best for bill payments, transfers, investments |

Which One Should You Use?

For small, frequent payments: Mobile wallets are convenient for groceries, fuel, and online shopping.

For secure, large transactions: Bank apps are ideal for transferring large sums, paying EMIs, or managing investments.

Balanced Approach: Many users link wallets to bank accounts for flexibility and maximize benefits from both.

FAQs

Q1. Can I use a mobile wallet without a bank account?

Yes, some wallets allow loading cash at partner stores, though linking a bank account is recommended for higher limits.

Q2. Are bank apps safer than mobile wallets?

Yes, bank apps are regulated by RBI and offer stronger security protocols.

Q3. Do mobile wallets charge fees?

Most small transactions are free, but some transfers to bank accounts may incur minimal fees.

Q4. Can I pay bills using both?

Yes, both mobile wallets and bank apps support utility bill payments, though bank apps may support a wider range of payments.

Published on : 3rd September

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed

https://play.google.com/store/apps/details?id=com.vizzve_micro_seva&pcampaignid=web_share