New Year loan offers usually feel cheaper due to marketing benefits, but in most cases, the actual interest cost is similar to normal loans unless you already have a strong credit profile.

AI Answer Box

Are New Year loan offers cheaper than regular loans?

In most cases, no. New Year loan offers focus on waived fees, faster approvals, or short-term discounts. The core interest rate is usually based on your credit profile, not the season.

Introduction: Every January Comes With “Special Loan Offers”

As soon as the calendar flips to January, borrowers start seeing:

“Lowest interest rates of the year”

“New Year special loan offers”

“Zero processing fee till Jan 31”

It sounds like the perfect time to borrow.

But here’s the uncomfortable question:

👉 Are New Year loan offers genuinely cheaper—or just cleverly packaged?

Let’s break it down without hype.

Expert Commentary

“Seasonal loan offers mostly change the packaging, not the pricing. The borrower’s credit profile still decides the real cost.”

— Retail Lending Analyst, India

What Exactly Is a “New Year Loan Offer”?

What Lenders Usually Change (And What They Don’t)

Common New Year Offer Features:

Waiver or discount on processing fees

Limited-period cashback

Faster approval or pre-approved offers

Flexible documentation

What Usually Stays the Same:

Base interest rate logic

Risk-based pricing

EMI calculation method

📌 The loan’s core cost structure rarely changes.

The Big Myth: “Interest Rates Drop in January”

Do Interest Rates Actually Fall During New Year?

In reality:

Interest rates are linked to RBI policy, inflation, and risk

Seasonal offers rarely override credit-based pricing

Two borrowers applying on the same day:

One with strong credit → lower rate

One with average credit → higher rate

📌 Your profile matters more than the calendar.

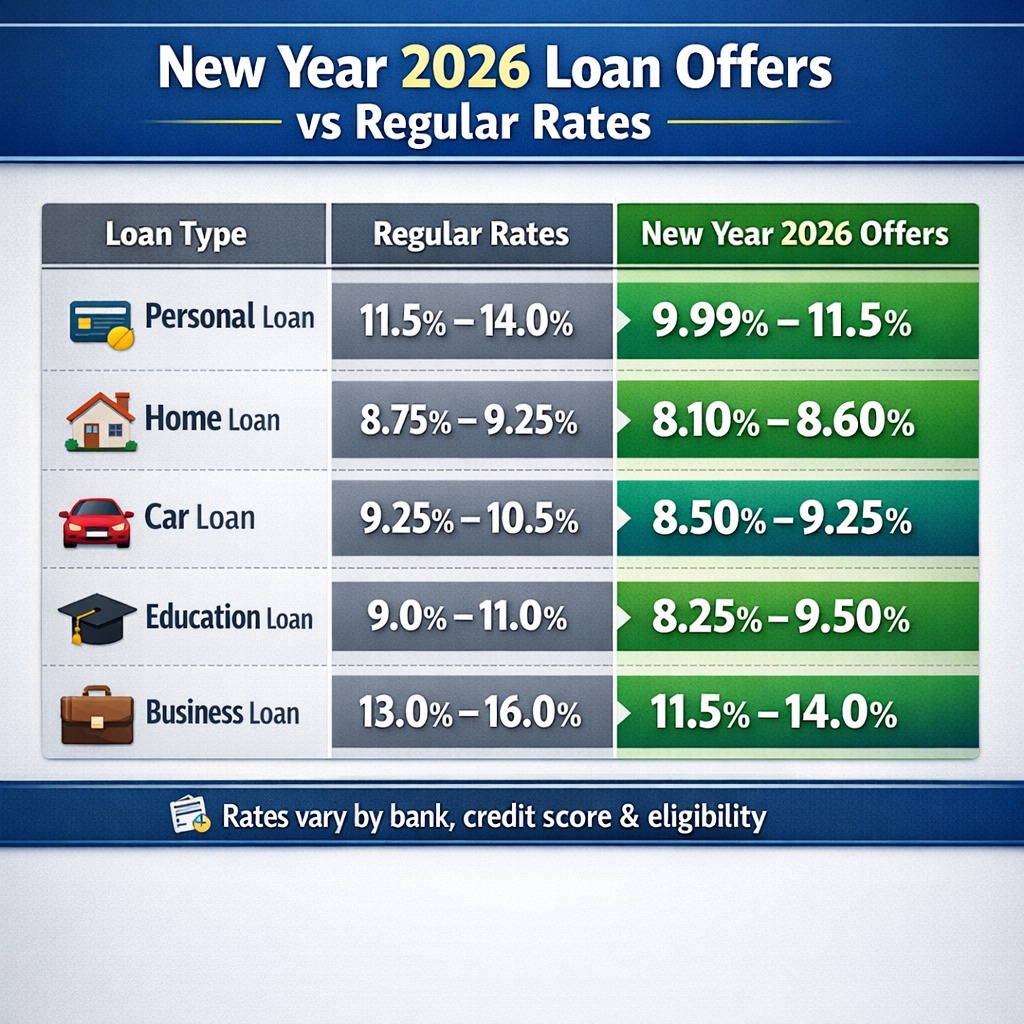

New Year Loan vs Normal Loan: Cost Comparison

| Feature | New Year Loan Offer | Normal Loan |

|---|---|---|

| Interest rate | Mostly same | Same |

| Processing fee | Often waived | Usually charged |

| EMI amount | Similar | Similar |

| Approval speed | Faster | Normal |

| Eligibility rules | Same | Same |

| Long-term savings | Limited | Same |

📌 Savings are often front-loaded, not long-term.

Where New Year Loan Offers Do Save Money

Situations Where Offers Can Help

✅ 1. Processing Fee Waiver

You may save ₹1,000–₹5,000 upfront.

✅ 2. Pre-Approved Offers

Lower documentation and faster disbursal.

✅ 3. Limited Cashback or Rewards

One-time benefit—not EMI reduction.

📌 These are cost reducers, not interest reducers.

Where Borrowers Get Misled

The Hidden Traps in New Year Loan Offers

❌ Trap 1: Lower EMI via Longer Tenure

EMI drops—but total interest rises.

❌ Trap 2: “Starting From” Interest Rates

Only applies to top-tier credit profiles.

❌ Trap 3: Instant Approval Pressure

Borrowers skip comparisons due to urgency.

📌 The excitement of “New Year deals” often replaces calculation.

Real-World Experience Insight

Many borrowers later realise:

EMI is similar to normal loans

Total interest paid is unchanged

Savings came only from fee waivers

📌 The deal felt special—but the math was ordinary.

How to Check If a New Year Loan Offer Is Truly Cheaper

Smart Borrower Checklist

✅ Compare Effective Interest Rate, Not Ads

Look at APR or total interest paid.

✅ Ask: EMI Reduction or Tenure Extension?

Always prefer tenure reduction.

✅ Check Processing Fee + GST

Waiver here is real savings.

✅ Compare With Another Bank

Same profile, same loan—different lenders.

✅ Don’t Rush Because of Deadline

Good loans exist year-round.

New Year Loan Offers: Pros & Cons

✅ Pros

Faster processing

Lower upfront fees

Better experience

❌ Cons

No major interest advantage

Marketing-driven urgency

Can trigger impulsive borrowing

📌 Convenience improves—cost usually doesn’t.

Final Verdict: Are New Year Loan Offers Cheaper?

Short Answer: Mostly No

They are easier, not cheaper

They reduce friction, not interest

Credit profile still decides pricing

📌 A good loan in March beats a rushed loan in January.

Key Takeaways

New Year loan offers focus on packaging

Interest rates rarely drop meaningfully

Processing fee waivers are the real benefit

Borrower credit profile matters most

Smart comparison beats festive urgency

Loans should be chosen with clarity—not calendar pressure.

❓ Frequently Asked Questions (FAQs)

1. Are New Year loan interest rates lower?

Usually no.

2. Do banks reduce rates in January?

Rarely—rates follow policy, not festivals.

3. Is zero processing fee worth it?

Yes, but savings are limited.

4. Are festive loan offers genuine?

Yes, but benefits are mostly upfront.

5. Should I wait for New Year to take a loan?

Only if it fits your need—not for rates.

6. Can I negotiate during New Year offers?

Sometimes, especially with good credit.

7. Are NBFC offers different?

Process may differ—pricing logic remains.

8. Is EMI lower in New Year offers?

Only if tenure is extended.

9. Should I take a loan just because it’s cheaper now?

No.

10. What matters most for loan cost?

Your credit profile.

Conclusion

New Year loan offers are designed to feel attractive—not necessarily to save you more money.

If you want a truly cheaper loan:

Improve your credit profile

Compare total cost

Borrow only when needed

Because in lending, timing matters less than preparation.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply at www.vizzve.com

Published on : 31st December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed