The biggest mistake borrowers make during New Year loan offers is focusing on festive discounts and speed instead of total loan cost, tenure, and long-term EMI pressure.

AI Answer Box

What mistakes should borrowers avoid during New Year loan offers?

Borrowers should avoid rushing decisions, ignoring total interest cost, extending tenure for lower EMI, and assuming festive loans are cheaper than regular loans.

Introduction: Why New Year Loan Offers Trigger Bad Decisions

Every January, loan marketing peaks.

Borrowers are told:

“Lowest interest of the year”

“Limited-time New Year offer”

“Instant approval—apply now”

The result?

👉 Speed replaces thinking.

And that’s exactly when most borrowing mistakes happen.

Expert Commentary

“Festive loan seasons don’t change lending math. They only change borrower psychology.”

— Consumer Credit Analyst, India

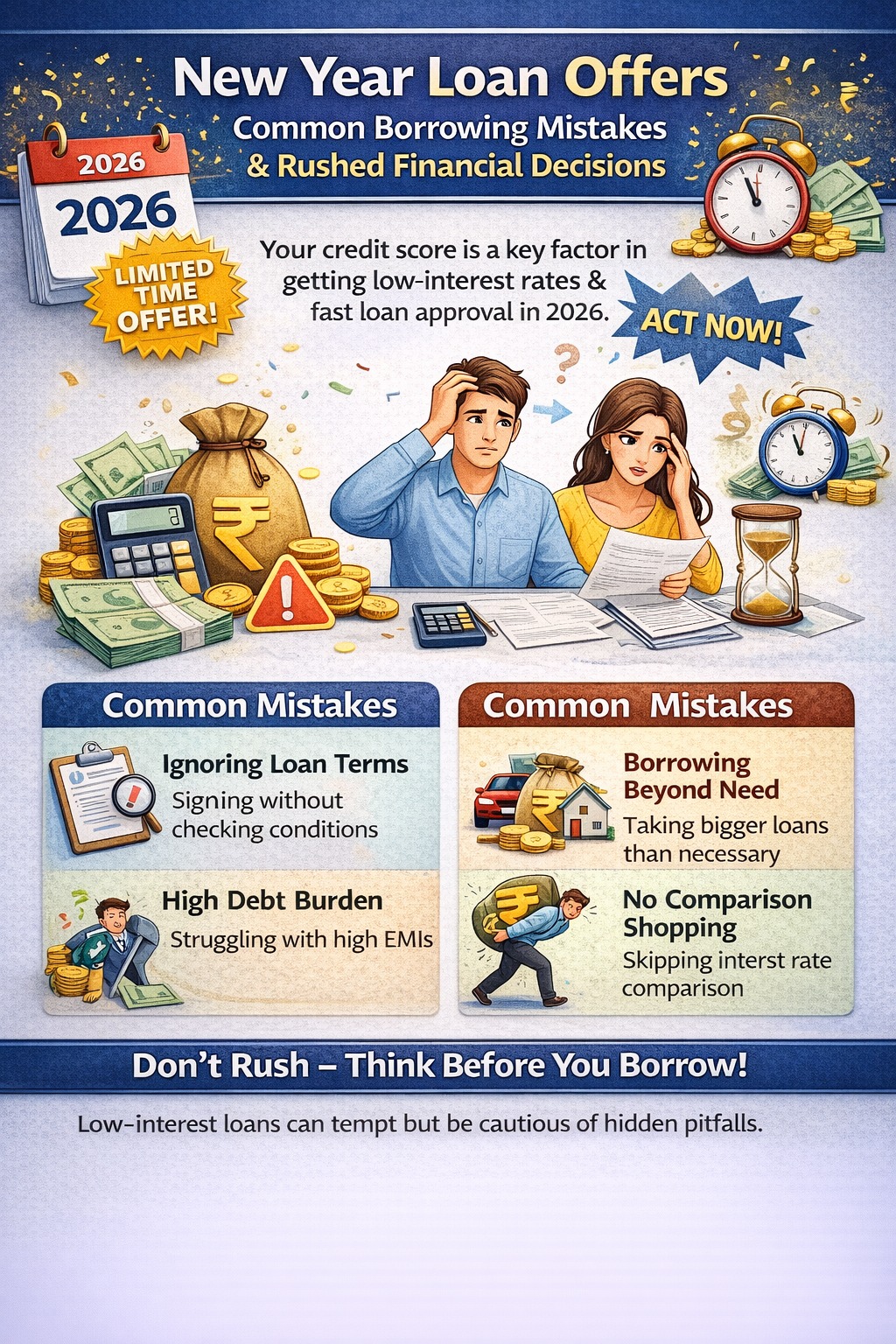

The Most Common New Year Loan Mistakes Borrowers Make

❌ Mistake #1: Assuming New Year Loans Are Automatically Cheaper

Festive Label ≠ Lower Cost

Many borrowers believe:

“It’s a New Year offer, so it must be cheaper.”

Reality:

Interest rates remain profile-based

Only fees or experience change

📌 Marketing changes faster than pricing.

❌ Mistake #2: Choosing Lower EMI by Extending Tenure

The Most Expensive Comfort Choice

Lower EMI feels good—but:

Loan runs longer

Total interest increases sharply

📌 Longer tenure = higher lifetime cost.

❌ Mistake #3: Ignoring Total Interest Paid

H2: EMI Focus Is a Trap

Borrowers often compare:

EMI amount only

Instead of:

Total interest

Effective annual cost (APR)

📌 A ₹500 EMI difference can hide ₹1–2 lakh extra interest.

❌ Mistake #4: Borrowing Just Because Approval Is Easy

Easy Credit Encourages Unnecessary Loans

During New Year:

Apps push instant loans

Pre-approved offers feel “safe”

But:

Convenience ≠ necessity

📌 Borrowing without purpose is the fastest way to regret.

❌ Mistake #5: Not Comparing Offers Properly

One Offer Is Never Enough

Many borrowers:

Accept first approved loan

Skip comparison

This often means:

Higher interest

Worse terms

📌 Same borrower, same day—different lenders = different costs.

❌ Mistake #6: Ignoring Processing Fees & Hidden Charges

“Zero Fee” Isn’t Always Zero

Festive offers may still include:

GST on fees

Insurance add-ons

Documentation charges

📌 Always check total disbursal vs total repayment.

❌ Mistake #7: Applying at Multiple Places After One Rejection

Panic Applications Hurt Eligibility

After rejection:

Borrowers apply everywhere

Credit enquiries spike

This:

Reduces approval chances further

📌 Pause > Apply smarter.

❌ Mistake #8: Assuming Credit Score Alone Guarantees Approval

Profile Matters More Than Score

Even during festive offers:

EMI load

Income stability

Credit behaviour

Still matter.

📌 A good score doesn’t cancel over-borrowing.

Real-World Borrower Insight

Many borrowers later realise:

Loan wasn’t cheaper

EMI felt manageable—but dragged on

Savings came only from fee waivers

📌 The mistake wasn’t the loan—it was the rush.

How to Borrow Smartly During New Year Offers

A Safer Borrowing Checklist

✅ Compare total interest, not ads

✅ Prefer shorter tenures

✅ Check EMI-to-income ratio (≤35%)

✅ Avoid impulse borrowing

✅ Read sanction letter carefully

📌 New Year loans should improve life—not add pressure.

Mistakes vs Smart Alternatives

| Common Mistake | Smarter Choice |

|---|---|

| Rush due to offer deadline | Take time to compare |

| Focus on EMI only | Check total interest |

| Extend tenure for comfort | Reduce tenure |

| Borrow because it’s easy | Borrow only if needed |

| Trust ads blindly | Read terms |

Key Takeaways

Festive loan offers increase urgency, not affordability

EMI comfort can hide long-term cost

Comparison is essential—even during offers

Credit discipline matters year-round

A delayed loan can be cheaper than a rushed one

Good loans come from clarity—not celebration.

❓ Frequently Asked Questions (FAQs)

1. Are New Year loan offers risky?

Not if chosen carefully.

2. What’s the biggest mistake borrowers make?

Rushing without comparing total cost.

3. Is lower EMI always better?

No—longer tenure increases interest.

4. Should I trust “limited-time” loan offers?

Verify terms before deciding.

5. Do festive loans have hidden charges?

Sometimes—read the fine print.

6. Is instant approval safe?

Only if borrowing is planned.

7. Can festive loans hurt credit score?

Yes, if mismanaged.

8. Should I take a loan just because it’s approved?

Never.

9. How many offers should I compare?

At least 2–3.

10. What matters more than festive timing?

Your credit profile and need.

Conclusion

New Year loan offers don’t create bad loans—bad decisions do.

If you slow down, calculate properly, and borrow intentionally, festive offers can be useful.

But if you rush, even the “best deal of the year” can turn expensive.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

👉 Apply at www.vizzve.com

Published on : 31st December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed