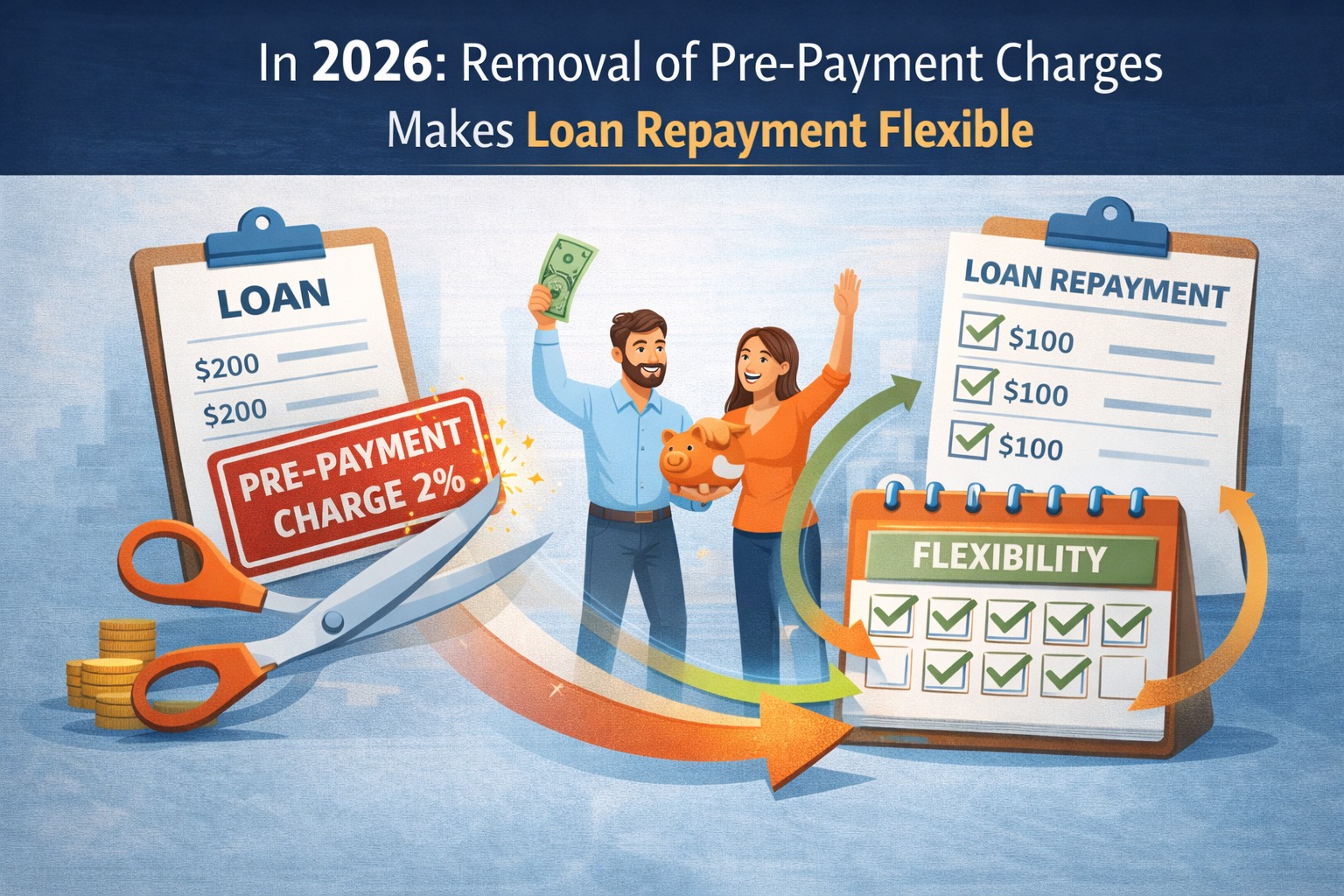

For years, borrowers faced a frustrating barrier: pre-payment charges. Even when you had extra money and wanted to close a loan early, penalties often discouraged smart repayment.

In 2026, that changes.

The removal of pre-payment charges marks a reset in India’s loan landscape, giving borrowers more control, flexibility, and long-term savings. But what does this actually mean for your EMIs, interest costs, and credit health?

Let’s break it down clearly.

AI Answer Box

The removal of pre-payment charges in 2026 allows borrowers to repay loans early without penalties. This reduces interest burden, improves financial flexibility, strengthens credit health, and gives borrowers greater control over loan repayment decisions.

Quick Summary Box (Fast Indexing)

No penalty for early loan repayment

Significant interest savings over time

More control over EMIs and tenure

Encourages disciplined borrowing

Benefits salaried and self-employed borrowers

What Are Pre-payment Charges?

Pre-payment charges are penalties charged when a borrower:

Pays off a loan before its scheduled tenure

Makes large lump-sum repayments

These charges were meant to protect lender interest income—but often punished responsible borrowers.

What Has Changed in 2026?

Removal of Pre-payment Penalties

In 2026, many loan products now allow:

Full foreclosure without penalty

Part-prepayment without extra cost

Greater repayment flexibility

This shift aligns lending with borrower-first principles rather than lender convenience.

How Borrowers Benefit from This Change

1. Massive Interest Savings

Interest is front-loaded in most loans. Early repayment means:

Less interest paid overall

Faster principal reduction

Example:

| Loan Detail | Without Prepayment | With Prepayment |

|---|---|---|

| Loan Amount | ₹5,00,000 | ₹5,00,000 |

| Tenure | 5 years | 3.5 years |

| Interest Paid | High | Much lower |

2. Greater EMI & Tenure Control

Borrowers can now:

Reduce tenure without penalty

Lower EMIs mid-loan

Adjust repayment as income grows

This creates adaptive loan planning, not rigid debt.

3. Improved Credit Health

Early or partial repayment:

Lowers outstanding debt

Improves credit capacity

Builds positive repayment behaviour

Responsible prepayment can strengthen long-term credit profiles.

Who Benefits the Most?

Borrower Groups That Gain Maximum Advantage:

Salaried professionals with bonuses

Self-employed individuals with variable income

Borrowers with multiple loans

Those planning early debt-free goals

Old Loan System vs 2026 Reset

| Aspect | Earlier System | 2026 System |

|---|---|---|

| Pre-payment | Penalised | Free |

| Borrower flexibility | Limited | High |

| Interest savings | Restricted | Significant |

| Loan planning | Fixed | Dynamic |

| Borrower power | Low | High |

Does This Mean You Should Always Prepay?

Not always.

Prepayment Makes Sense If:

You have surplus funds

Emergency fund is intact

Interest rate is high

Prepayment May Not Be Ideal If:

Funds are needed for liquidity

Loan interest is very low

Better investment returns exist

Smart borrowers balance repayment with liquidity.

How to Use This Change Wisely in 2026

Step-by-Step Smart Strategy:

Review loan interest rate

Calculate interest saved via prepayment

Maintain emergency fund first

Prepay in chunks, not all at once

Choose tenure reduction over EMI cut (usually better)

Expert Commentary: A Borrower-First Era

“Removing pre-payment charges shifts power back to borrowers. It rewards discipline instead of penalising it.”

— Retail Lending Analyst

Key Takeaways

2026 removes a major borrower penalty

Early repayment becomes cost-effective

Interest savings can be substantial

Loan planning becomes flexible

Discipline is finally rewarded

❓ Frequently Asked Questions (FAQs)

1. What does removal of pre-payment charges mean?

You can repay loans early without penalties.

2. Does this apply to all loans?

Mostly personal and retail loans; terms may vary by product.

3. Will prepayment improve credit score?

It can improve credit capacity and repayment profile.

4. Should I prepay or invest?

Depends on interest rate vs investment returns.

5. Is partial prepayment allowed?

Yes, without penalty in most cases.

6. Does this reduce EMI or tenure?

You can usually choose either.

7. Is foreclosure now cheaper?

Yes, significantly.

8. Who gains the most?

Borrowers with surplus or variable income.

Conclusion: A Fairer Loan System for Borrowers

The 2026 loan landscape reset marks a turning point. By removing pre-payment charges, the system finally aligns with what borrowers want: freedom, fairness, and financial control.

Loans no longer have to be long-term burdens—they can be shortened, reshaped, and closed on your terms.

📌 In 2026, smart repayment isn’t punished—it’s empowered.

Published on : 2nd January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed