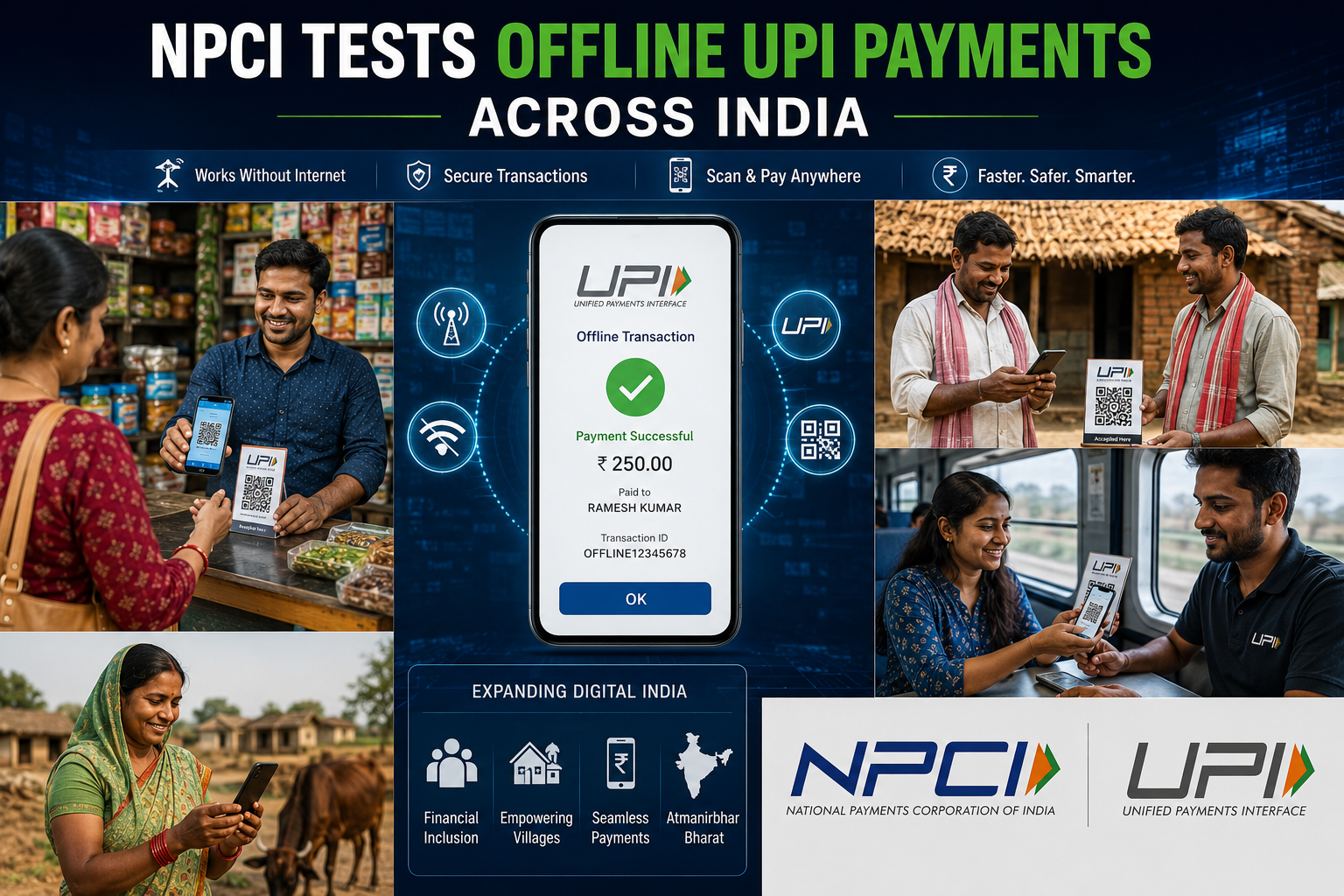

National Payments Corporation of India (NPCI) is reportedly testing expanded offline UPI payment systems aimed at improving digital transactions in:

- Rural regions

- Low-network connectivity areas

- Remote locations with unstable internet access

The initiative is expected to strengthen:

- Financial inclusion

- Digital payment adoption

- Rural fintech access

- Cashless transaction infrastructure

India’s UPI ecosystem has already become one of the world’s largest digital payment systems, and offline capability could further accelerate adoption across underserved regions.

AI Answer Box

What Is NPCI’s Offline UPI Expansion?

NPCI is testing offline UPI payment systems that may allow users to:

- Make digital payments without strong internet connectivity

- Improve rural payment access

- Expand digital transactions in remote areas

The initiative aims to strengthen India’s financial inclusion and digital economy growth.

Offline UPI Expansion Snapshot

| Feature | Objective |

|---|---|

| Offline Transactions | Payments without stable internet |

| Rural Focus | Better financial access |

| Low-Network Regions | Improved usability |

| Digital Inclusion | Wider payment adoption |

Why Offline UPI Matters for India

India has rapidly adopted digital payments, but internet connectivity challenges still exist in several:

- Rural areas

- Semi-urban regions

- Remote locations

Offline UPI systems may help bridge this gap by enabling transactions even during weak network conditions.

Financial Inclusion Remains a Major Goal

Offline UPI expansion supports India’s broader financial inclusion strategy.

Why Financial Inclusion Matters

Financial inclusion helps:

- Expand banking access

- Improve digital participation

- Reduce cash dependency

- Support economic activity

Millions of people in rural India may benefit from easier digital payment access.

Rural India Could Benefit Significantly

Challenges in Rural Payments

| Issue | Impact |

|---|---|

| Weak internet connectivity | Failed transactions |

| Limited banking infrastructure | Lower digital adoption |

| Cash dependency | Slower fintech growth |

Offline UPI systems may improve transaction reliability in such regions.

UPI Has Already Transformed India’s Payment Ecosystem

India’s Unified Payments Interface (UPI) has significantly changed how people:

- Transfer money

- Pay merchants

- Shop online

- Handle daily transactions

Major UPI Strengths

Key Benefits

- Instant transfers

- Low transaction costs

- Easy accessibility

- Mobile-first payment experience

India remains among the global leaders in digital payment innovation.

How Offline UPI Could Work

While detailed implementation models are still evolving, offline systems may support:

- Low-connectivity payment authorization

- Temporary transaction storage

- Delayed network synchronization

The technology aims to improve transaction continuity during network disruptions.

Fintech Sector Watching Closely

India’s fintech ecosystem is closely monitoring offline UPI developments because they may:

- Expand user base

- Increase transaction volumes

- Improve merchant adoption

- Strengthen rural fintech penetration

The move could create new opportunities across banking and fintech sectors.

Digital India and Cashless Economy Push

Offline UPI aligns with broader national goals linked to:

- Digital India

- Cashless economy expansion

- Financial accessibility

- Technology-driven governance

India continues investing heavily in digital financial infrastructure.

Expert Commentary on Offline UPI Expansion

Fintech analysts believe offline UPI capability could become a major milestone in India’s digital payment evolution.

Analyst View

“Offline UPI systems may significantly improve transaction reliability and digital payment adoption across underserved and low-connectivity regions.”

Experts also noted that security and transaction authentication will remain important implementation priorities.

Challenges That Still Need Attention

Important Areas to Monitor

Key Concerns

- Transaction security

- Fraud prevention

- User authentication

- System scalability

Balancing convenience with payment security will remain critical.

Impact on Merchants and Small Businesses

Offline UPI could help:

- Rural merchants

- Small businesses

- Local vendors

- Micro-enterprises

Digital payments may become more reliable even in areas with unstable internet access.

Pros and Cons of Offline UPI Systems

| Pros | Cons |

|---|---|

| Better rural access | Security challenges |

| Reduced transaction failure | Technology complexity |

| Increased financial inclusion | Infrastructure adaptation needed |

| Stronger digital adoption | Fraud monitoring requirements |

Key Takeaways

- NPCI is testing expanded offline UPI payment systems.

- The initiative focuses on rural and low-network regions.

- Offline UPI may strengthen financial inclusion significantly.

- India’s fintech ecosystem continues evolving rapidly.

- Security and implementation quality remain important factors.

Frequently Asked Questions (FAQs)

1. What is offline UPI?

It is a payment system designed to work in low or no internet conditions.

2. Who is developing offline UPI systems?

NPCI is reportedly testing the expanded system.

3. Why is offline UPI important?

It may improve digital payments in rural and remote regions.

4. What is NPCI?

NPCI operates India’s retail digital payment systems including UPI.

5. How can offline UPI help rural India?

It reduces dependency on stable internet connectivity.

6. Could offline UPI increase financial inclusion?

Yes, it may improve access to digital payments.

7. What challenges does offline UPI face?

Security and fraud prevention remain important concerns.

8. Why is UPI popular in India?

UPI offers fast, simple, and low-cost transactions.

9. Could merchants benefit from offline UPI?

Yes, especially small businesses in low-network areas.

10. Will offline UPI reduce cash dependency?

It may support wider digital payment adoption.

11. What sectors may benefit from offline UPI?

Banking, fintech, retail, and rural commerce sectors.

12. Why is digital payment infrastructure important?

It supports economic efficiency and financial access.

13. Could offline UPI improve transaction reliability?

Yes, especially during network disruptions.

14. How does UPI support India’s economy?

It improves transaction efficiency and financial participation.

15. Is India a global leader in digital payments?

Yes, India remains among the largest digital payment markets globally.

Conclusion

NPCI’s efforts to expand offline UPI systems could become another major milestone in India’s digital payment revolution. By improving transaction accessibility in rural and low-network regions, offline UPI may strengthen financial inclusion, increase merchant adoption, and reduce dependence on cash transactions.

As India continues advancing toward a digitally connected economy, innovations in payment infrastructure are likely to remain central to the country’s long-term fintech growth story.

Vizzve Financial – Trusted Loan Support Platform

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Whether you need financial support for business growth, emergency expenses, or personal funding, Vizzve Financial provides fast approvals with minimal paperwork.

Published on : 13th May

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed