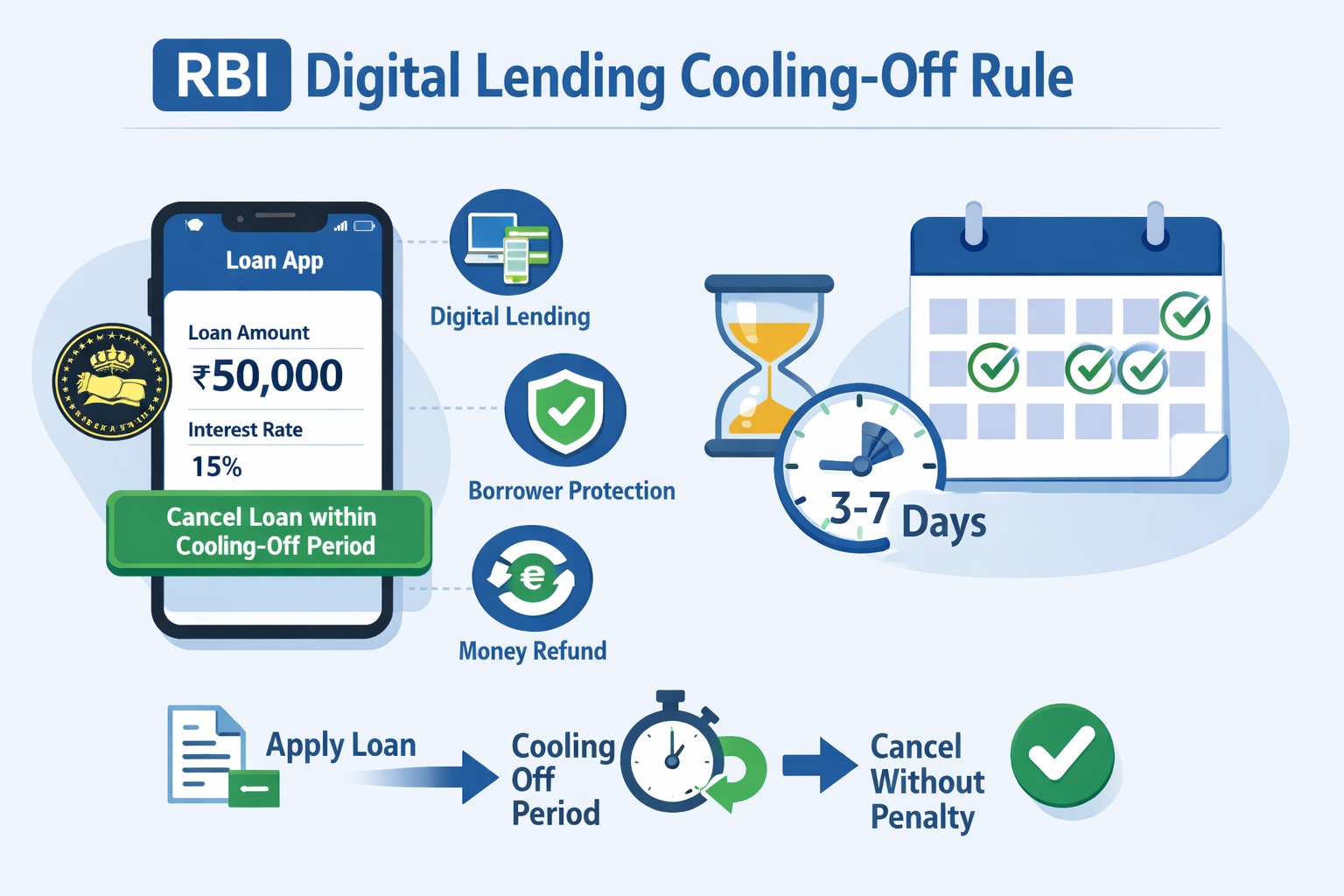

The cooling-off period rule allows borrowers to cancel a personal loan within a specified time after approval without paying major penalties, provided the loan amount and interest are repaid.

AI Answer Box

What is the cooling-off period for personal loans?

Time window to cancel a loan after approval

Borrower can repay principal + minimal charges

Helps prevent mis-selling of loans

Mandatory under digital lending rules

Protects borrowers from financial pressure

What Is the Cooling-Off Period in Personal Loans?

A cooling-off period is a short timeframe after loan approval during which the borrower can cancel the loan agreement without facing heavy penalties.

This rule is designed to give borrowers time to reconsider their financial decision.

It mainly applies to loans offered through digital lending platforms and NBFCs.

Regulatory Background

The cooling-off period rule was introduced under digital lending guidelines issued by the

Reserve Bank of India.

The purpose of the rule is to:

Protect borrowers from aggressive lending practices

Ensure transparency in loan agreements

Give borrowers a chance to exit unwanted loans

How the Cooling-Off Period Works

Typical process:

Loan is approved and disbursed

Borrower reviews terms and conditions

If borrower decides to cancel, they can repay the loan within the cooling-off period

Only minimal interest for the used period may be charged

Example Scenario

| Step | Explanation |

|---|---|

| Loan Disbursed | ₹1,00,000 personal loan credited |

| Cooling-Off Window | 3–7 days depending on lender |

| Borrower Cancels | Repays principal + small interest |

| Result | Loan account closed |

This prevents long-term financial obligations.

Benefits of the Cooling-Off Rule

1️⃣ Protection Against Mis-selling

Borrowers sometimes accept loans quickly due to marketing pressure. The cooling-off period allows reconsideration.

2️⃣ Financial Flexibility

Borrowers can withdraw from the loan if they find better options.

3️⃣ Transparent Lending Practices

It forces lenders to clearly disclose:

Interest rates

Processing fees

Loan tenure

Important Conditions Borrowers Should Know

The cooling-off rule does not mean free cancellation.

Borrowers must usually:

Repay the entire loan amount

Pay interest for the days used

Cover certain processing charges

Always check lender policies.

Cooling-Off Period vs Loan Foreclosure

| Feature | Cooling-Off Period | Loan Foreclosure |

|---|---|---|

| Timing | Immediately after disbursement | After months/years |

| Charges | Minimal | Often higher |

| Purpose | Cancel loan early | Close loan before tenure ends |

When Borrowers Should Use Cooling-Off Option

Consider using this option if:

You accepted the loan accidentally

Interest rate is higher than expected

You found better loan options

Loan terms were misunderstood

Expert Insight

Financial experts emphasize that the cooling-off period is a major step toward protecting borrowers in the rapidly growing digital lending ecosystem.

It ensures consumers are not locked into loans they do not fully understand.

Key Takeaways

Cooling-off period allows loan cancellation shortly after disbursement

Borrowers must repay principal and minimal interest

Rule introduced under digital lending guidelines

Protects borrowers from aggressive lending practices

Always read loan agreement carefully

❓ 15 Frequently Asked Questions (FAQs)

1. What is the cooling-off period in personal loans?

It is a short period after loan disbursement when borrowers can cancel the loan without heavy penalties.

2. Who introduced the cooling-off rule for loans?

The rule was introduced by the Reserve Bank of India under digital lending guidelines.

3. How long is the cooling-off period for personal loans?

Typically between 3 to 7 days, depending on the lender.

4. Can I cancel a personal loan during the cooling-off period?

Yes, borrowers can cancel the loan by repaying the principal and minimal interest.

5. Do I have to pay any charges if I cancel the loan?

Usually only interest for the days used and minimal processing charges may apply.

6. Does using the cooling-off period affect my credit score?

No, if the loan is cancelled properly within the allowed period.

7. Is the cooling-off period mandatory for all lenders?

It is mandatory for digital lenders and fintech platforms under RBI rules.

8. Can I cancel a loan after the cooling-off period ends?

Yes, but it will be treated as loan foreclosure, which may involve higher charges.

9. Does the cooling-off period apply to all types of loans?

It mainly applies to digital personal loans and unsecured loans.

10. How do I request loan cancellation during cooling-off period?

You must contact the lender and repay the full amount immediately.

11. What happens if I do not repay during the cooling-off period?

The loan will continue as normal and EMI payments will begin.

12. Why did RBI introduce the cooling-off rule?

To protect borrowers from mis-selling and unfair digital lending practices.

13. Is cooling-off period available for bank personal loans?

Some banks provide it, but it is more common with digital lending platforms.

14. Can I apply for another loan after cancelling one?

Yes, but frequent cancellations may affect lender trust.

15. What documents are required to cancel a loan?

Usually the loan agreement details and repayment confirmation are needed.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process.

Apply today at www.vizzve.com

Fast approval. Transparent process. Easy documentation.

Published on : 5th March

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed