In 2026, personal loan interest rates in India typically range from around 10.5% to 24% — with banks generally offering lower rates (10.5–18%) while NBFCs may charge slightly higher (12–24%) based on risk profiles and customer credit profiles.

Introduction

If you’re planning to take a personal loan in India, the interest rate difference between banks and NBFCs can significantly impact your EMIs and total repayment.

Personal loans are widely used for:

✔ Emergencies

✔ Travel & weddings

✔ Medical needs

✔ Home renovation

✔ Education

✔ Debt consolidation

Let’s break down how rates compare in 2026 and what drives the differences.

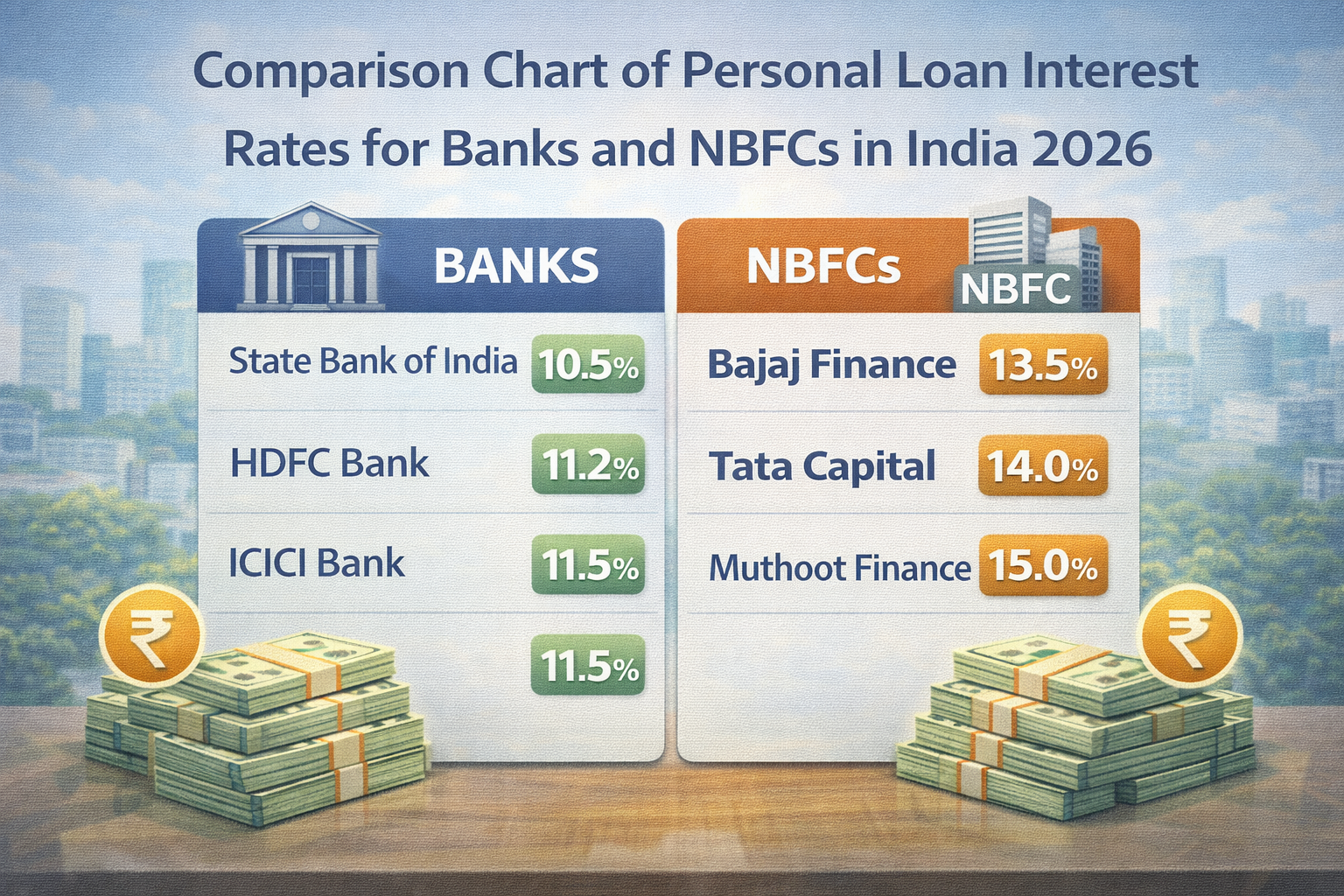

Bank vs NBFC Personal Loan Interest Rates (2026)

Average Interest Rate Range

| Lender Type | Typical Interest Range |

|---|---|

| Banks (Public & Private) | 10.5% – 18% p.a. |

| NBFCs (Fintech + Traditional) | 12% – 24% p.a. |

Note: Actual rates vary by lender, credit score, income, and tenure.

Personal Loan Rates at Major Indian Banks

Banks may offer lower rates because they:

• Have access to low-cost deposits

• Follow strict credit guidelines

• Use borrower banking history for pricing

Typical Bank Rate Range:

💰 10.5% – 16.5% p.a. (Prime borrowers)

💰 16.5% – 18% p.a. (Moderate credit profiles)

Personal Loan Rates at NBFCs

NBFCs include traditional non-bank lenders and digital fintech platforms. They:

✔ Accept alternative data

✔ Serve lower credit profiles

✔ Disburse faster

NBFC Rate Range:

📊 12% – 20% p.a. (Good profiles)

📊 20% – 24% p.a. (Higher risk or instant loans)

Why NBFC Rates Are Higher

📌 1. Risk-Based Pricing

NBFCs may lend to customers with:

Thin credit history

Less formal income proof

Gig or informal work profiles

They charge higher rates to manage risk.

📌 2. Faster Processing

Instant or minimal-document loans come at a premium.

📌 3. Technology & Convenience Fees

Some digital platforms include convenience charges.

How Banks Price Personal Loans

✔ Banking relationship benefits

✔ Better historical data

✔ Lower cost of funds

✔ Risk-assessed pricing models

Banks may offer:

• Better rates to existing customers

• Experience bonuses (salary account + loan combo)

Examples of Rates in 2026

| Borrower Type | Bank Rate | NBFC Rate |

|---|---|---|

| High credit score | 11% – 13% | 13% – 16% |

| Average score | 14% – 16% | 17% – 20% |

| Thin credit history | 16% – 18% | 20% – 24% |

How to Get Lower Personal Loan Rates

💡 1. Improve Credit Score

High scores often bring rates toward the lower band.

💡 2. Use Salary Account With Bank

Banks often give discounts to salary customers.

💡 3. Choose Longer or Shorter Tenure Smartly

Shorter tenure → lower total cost (but higher EMI).

Longer tenure → smaller EMI (but higher total interest).

💡 4. Negotiate

Banks sometimes negotiate if you have strong docs.

💡 5. Consider Balance Transfers

If rates drop later, transfer to a cheaper lender.

When NBFCs Can Be Better

✔ You need quick approval

✔ You lack formal income proofs

✔ You have limited bank history

✔ You’re a gig/freelance worker

Expert Insight

Retail Lending Analyst – Mumbai

“Banks tend to remain cheaper in most cases, but NBFCs fill an essential gap for underserved profiles — and digital platforms are bridging friction in credit access.”

Consumer Finance Advisor – Delhi

“Always compare APR — including processing fees — not just headline interest.”

Key Takeaways

✔ Banks usually offer lower personal loan rates

✔ NBFCs provide speed and flexibility but at higher rates

✔ Credit score remains the biggest driver

✔ Compare APR, fees, and tenure before signing

❓ FAQs –

1. Which has lower rates — bank or NBFC loans?

Banks usually offer lower interest.

2. Why do NBFCs charge more?

They serve wider profiles and offer faster approvals.

3. Do personal loans affect credit score?

Yes — timely payments improve scores.

4. Can I get a loan without salary account?

Yes — but rates may be higher.

5. Is the rate fixed or floating?

Most personal loans have fixed rates.

6. Do processing fees count in cost?

Yes — always check APR.

7. Are prepayment charges applicable?

Depends on lender policy.

8. Should I negotiate rate?

Worth trying — especially with strong profile.

Final Word

In 2026, banks remain the first choice for lowest interest — but NBFCs fill critical gaps with fast, flexible credit. Smart comparison, good credit, and timing can save you tens of thousands in interest.

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com

Published on : 20th February

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed