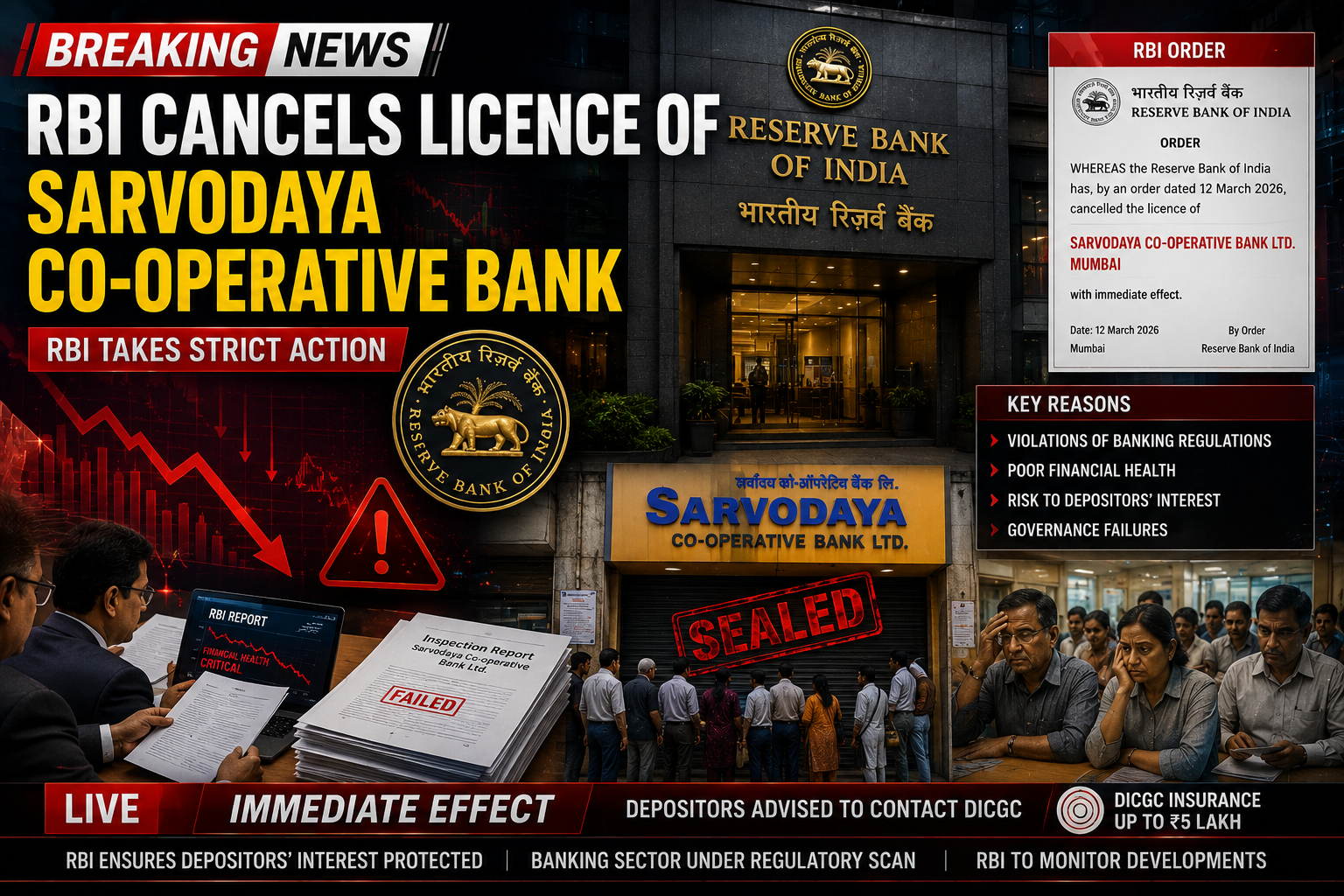

Reserve Bank of India has cancelled the licence of Sarvodaya Co-operative Bank citing:

- Inadequate capital

- Weak future earnings prospects

- Concerns over financial sustainability

The move highlights RBI’s continued focus on maintaining financial stability and protecting depositors within India’s banking system.

Importantly, deposits up to ₹5 lakh remain insured under the Deposit Insurance and Credit Guarantee Corporation (DICGC) framework, providing relief to eligible customers.

AI Answer Box

Why Did RBI Cancel Sarvodaya Co-operative Bank’s Licence?

RBI cancelled Sarvodaya Co-operative Bank’s licence due to:

- Inadequate capital levels

- Weak earning prospects

- Concerns over long-term viability

Depositors are protected up to ₹5 lakh under DICGC deposit insurance coverage.

RBI Action Snapshot

| Area | RBI Observation |

|---|---|

| Capital Position | Inadequate |

| Earnings Outlook | Weak |

| Financial Sustainability | Concern |

| Depositor Protection | Up to ₹5 lakh insured |

Why RBI Cancelled the Licence

According to RBI, the bank lacked sufficient:

- Capital adequacy

- Financial strength

- Sustainable earnings capability

Why Capital Adequacy Matters

Banks require strong capital buffers to:

- Absorb financial losses

- Protect depositors

- Maintain operational stability

- Support future lending activity

Weak capital levels increase financial risk within the banking system.

Weak Earnings Prospects Raised Concerns

RBI also highlighted concerns about the bank’s ability to:

- Generate sustainable profits

- Maintain operational viability

- Improve long-term financial health

Banks with weak earnings often struggle to:

- Build reserves

- Expand operations

- Maintain customer confidence

Deposits Up to ₹5 Lakh Remain Insured

One of the most important protections for customers is the DICGC insurance framework.

What Depositors Should Know

| Protection Type | Coverage |

|---|---|

| Deposit Insurance | Up to ₹5 lakh |

| Applicable Institution | DICGC |

| Coverage Includes | Savings, FD, Current Accounts |

This means eligible depositors can claim insured amounts up to ₹5 lakh.

What Is DICGC?

The Deposit Insurance and Credit Guarantee Corporation (DICGC) provides deposit insurance protection for bank customers in India.

DICGC Coverage Includes

- Savings accounts

- Fixed deposits

- Current accounts

- Recurring deposits

The insurance framework helps improve public confidence in the banking system.

Co-operative Banks Remain Important in India

Co-operative banks play a significant role in:

- Local banking services

- Small business financing

- Community banking

- Rural financial inclusion

However, some co-operative banks continue facing challenges related to:

- Governance

- Capital adequacy

- Risk management

- Operational efficiency

RBI’s Focus on Banking Stability

Reserve Bank of India has increasingly strengthened oversight of:

- Co-operative banks

- Financial institutions

- Banking governance

- Risk management systems

RBI’s Objectives

Major Priorities

- Financial stability

- Depositor protection

- Banking transparency

- Risk reduction

The regulator continues taking action against financially weak institutions when necessary.

Impact on Depositors and Customers

Customers may experience:

- Temporary operational disruption

- Claims process for insured deposits

- Banking transition arrangements

However, insured deposit protection significantly reduces risk for small depositors.

Why Banking Regulation Matters

Strong banking regulation helps:

- Protect public money

- Maintain trust in financial institutions

- Reduce systemic risk

- Improve long-term financial stability

India’s banking system relies heavily on public confidence and regulatory oversight.

Expert Commentary on RBI’s Action

Banking analysts believe RBI’s decision reflects stricter regulatory enforcement.

Analyst View

“Protecting depositor interests and maintaining financial discipline remain key priorities for RBI, especially within the co-operative banking sector.”

Experts also noted that proactive regulatory intervention can reduce larger financial risks later.

Co-operative Banking Sector Challenges

Common Challenges

| Challenge | Impact |

|---|---|

| Weak governance | Operational risks |

| Limited capital | Lower resilience |

| Poor profitability | Sustainability concerns |

| Compliance gaps | Regulatory pressure |

The sector continues evolving under tighter regulatory supervision.

Public Confidence and Banking Safety

The DICGC insurance system remains important for maintaining:

- Depositor confidence

- Banking stability

- Financial security

Public awareness regarding insured deposit limits has increased significantly in recent years.

Pros and Cons of Strict Banking Regulation

| Pros | Cons |

|---|---|

| Better depositor protection | Operational disruption for customers |

| Improved financial discipline | Market uncertainty |

| Stronger banking stability | Temporary inconvenience |

| Reduced systemic risk | Banking consolidation pressure |

Key Takeaways

- RBI cancelled Sarvodaya Co-operative Bank’s licence.

- Weak capital and earnings outlook were major reasons.

- Deposits up to ₹5 lakh remain insured under DICGC.

- RBI continues strengthening banking sector oversight.

- Depositor protection remains a major regulatory priority.

Vizzve Financial – Trusted Loan Support Platform

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Apply at www.vizzve.com.

Whether you need emergency financial support, business funding, or personal loan assistance, Vizzve Financial provides fast approvals with minimal paperwork.

Frequently Asked Questions

1. Why did RBI cancel Sarvodaya Co-operative Bank’s licence?

Due to inadequate capital and weak future earnings prospects.

2. Are depositors protected after the licence cancellation?

Yes, deposits up to ₹5 lakh remain insured.

3. What is DICGC?

It is India’s deposit insurance agency.

4. How much deposit insurance is available in India?

Up to ₹5 lakh per depositor per bank.

5. What accounts are covered under deposit insurance?

Savings, fixed deposits, current accounts, and recurring deposits.

6. Why is capital adequacy important for banks?

It helps banks absorb losses and maintain stability.

7. What role does RBI play in banking regulation?

RBI supervises banks and maintains financial stability.

8. Are co-operative banks important in India?

Yes, they support local banking and financial inclusion.

9. What risks do weak banks face?

Liquidity, profitability, and operational sustainability challenges.

10. How does deposit insurance help customers?

It protects small depositors during banking failures.

11. Could more regulatory action happen in the future?

RBI continues monitoring banking sector stability actively.

12. Why do banks need sustainable earnings?

Profits support reserves, growth, and operational stability.

13. What happens after a bank licence cancellation?

Banking operations stop and depositor settlement processes begin.

14. How does banking regulation protect the economy?

It reduces financial system risks and maintains confidence.

15. Why are banking reforms important?

They improve financial stability and governance standards.

Conclusion

RBI’s cancellation of Sarvodaya Co-operative Bank’s licence highlights the importance of strong financial governance, capital adequacy, and depositor protection within India’s banking system. While the action may create temporary concerns for customers, the DICGC insurance framework ensures protection for eligible deposits up to ₹5 lakh.

The development also reflects RBI’s increasingly proactive approach toward strengthening financial stability and improving regulatory discipline across India’s banking sector.

Published on : 13th May

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed