Many people assume money stored in old or inactive bank accounts is permanently lost once the account becomes dormant. However, the Reserve Bank of India has clarified that customers can still recover funds from dormant accounts by following the proper banking procedures.

Dormant or inoperative accounts are common in India due to:

- Job changes

- Salary account closures

- Forgotten savings accounts

- Relocation

- Multiple bank accounts

The RBI’s guidelines are designed to protect customer money and simplify account reactivation.

AI Answer Box

Can money be recovered from a dormant bank account?

Yes. According to the RBI, customers can still claim and reactivate dormant bank accounts after completing verification and KYC procedures.

What is a dormant bank account?

A bank account becomes dormant or inoperative when there are no customer-initiated transactions for a long period, usually over two years.

Introduction

Millions of bank accounts across India eventually become inactive because users stop operating them for long periods.

Common reasons include:

- Switching jobs

- Opening new salary accounts

- Relocation

- Forgotten savings accounts

- Limited account usage

Under RBI banking rules, banks classify such accounts as “dormant” or “inoperative” after prolonged inactivity.

The important point, however, is that:

✅ Your money does not disappear.

The Reserve Bank of India allows customers to reclaim funds and reactivate dormant accounts through a standard verification process.

What Is a Dormant Bank Account?

A bank account generally becomes dormant when:

- No customer-initiated transactions occur for over 24 months.

This includes:

- Savings accounts

- Current accounts

Examples of customer transactions:

- Cash withdrawals

- Deposits

- Online transfers

- ATM usage

- Cheque activity

Dormant vs Inactive Account

| Type | Meaning |

|---|---|

| Inactive Account | No transactions for 12 months |

| Dormant/Inoperative Account | No transactions for 24 months |

Banks may restrict certain services once accounts become dormant.

Can You Still Claim the Money?

Yes — RBI Says Customers Retain Full Rights

The money inside dormant accounts still legally belongs to the account holder.

Banks cannot permanently seize customer funds simply because the account became inactive.

Customers can:

- Reactivate the account

- Withdraw funds

- Transfer balances

- Update KYC information

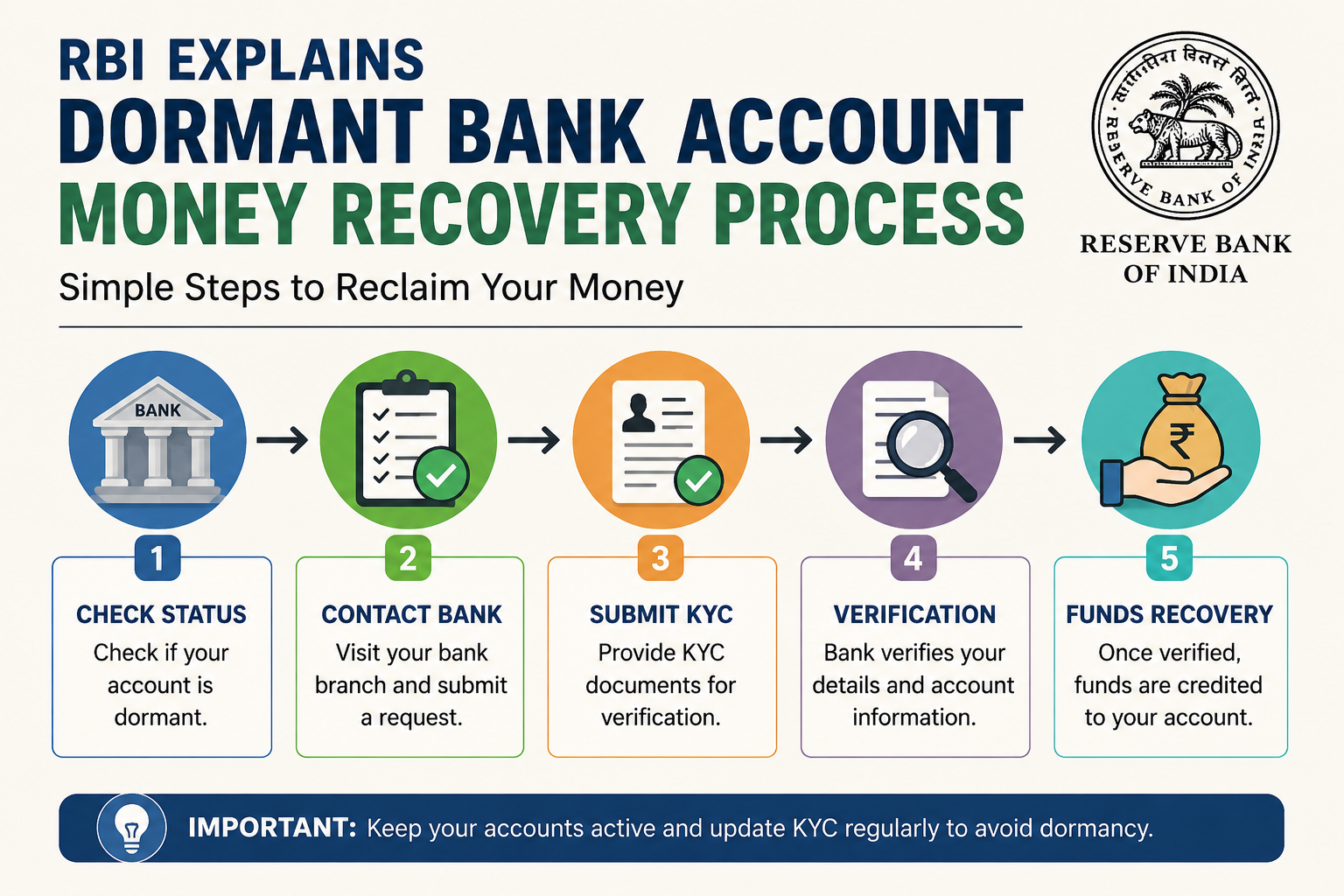

How To Claim Money From a Dormant Account

Step-by-Step Process

Step 1: Visit the Bank Branch

Visit your bank’s home branch or nearest branch.

Step 2: Submit KYC Documents

Banks usually require:

- Aadhaar card

- PAN card

- Address proof

- Passport-size photo

Step 3: Fill Reactivation Form

You may need to complete:

- Account reactivation request

- KYC update form

Step 4: Verification Process

The bank verifies:

- Identity

- Signature

- Account ownership

Step 5: Reactivate the Account

After successful verification:

- The account becomes active again

- Funds become accessible

Documents Usually Required

| Document Type | Examples |

|---|---|

| Identity Proof | Aadhaar, PAN |

| Address Proof | Utility bill, Aadhaar |

| Photographs | Passport-size photos |

| Signature Verification | Bank records |

Requirements may vary slightly across banks.

Why Accounts Become Dormant

Common Reasons Include:

- Unused salary accounts

- Migration to digital banking

- Multiple savings accounts

- Forgotten old accounts

- Lack of regular transactions

Dormant accounts have increased significantly due to rising banking penetration.

RBI Rules for Dormant Accounts

The Reserve Bank of India requires banks to:

- Protect customer funds

- Maintain account records

- Provide reactivation facilities

- Ensure customer verification

Banks are also expected to help customers recover unclaimed deposits.

Are Dormant Accounts Safe?

Dormant accounts are generally protected through:

- Banking regulations

- KYC verification

- Fraud-monitoring systems

Banks may temporarily limit transactions to prevent unauthorized access.

What Happens to Unclaimed Deposits?

If accounts remain inactive for many years:

- Balances may eventually move to RBI’s Depositor Education and Awareness Fund (DEAF).

However:

✅ Customers can still claim the money later.

Dormant Account Reactivation: Quick Summary

| Process | Status |

|---|---|

| Money Lost? | No |

| Reactivation Possible? | Yes |

| KYC Needed? | Usually yes |

| Bank Visit Required? | Often yes |

| RBI Protection Exists? | Yes |

Expert Commentary on Dormant Accounts

Banking experts advise customers to:

- Periodically review old accounts

- Keep KYC details updated

- Close unused accounts if unnecessary

Experts also warn that dormant accounts may become vulnerable to:

- Fraud attempts

- Forgotten balances

- Communication issues

Regular monitoring helps improve financial security.

Tips To Avoid Dormant Account Problems

Best Practices:

- Use accounts occasionally

- Enable SMS/email alerts

- Update KYC regularly

- Monitor bank statements

- Close unused accounts

Digital banking apps now make account monitoring easier.

Impact on Customers

RBI’s clarification is important because many people mistakenly believe dormant-account money becomes inaccessible forever.

The rules help:

- Protect customer rights

- Improve financial awareness

- Simplify banking access

Key Takeaways

- Dormant bank-account money can still be claimed.

- RBI allows account reactivation through verification procedures.

- Accounts usually become dormant after 24 months of inactivity.

- KYC updates are often required.

- Customers retain ownership of the account balance.

Pros & Cons of Dormant Account Rules

Pros

- Protects customer funds

- Prevents unauthorized transactions

- Supports fraud control

- Allows later recovery of funds

Cons

- Reactivation paperwork required

- Branch visits may be needed

- Forgotten accounts create inconvenience

Future Outlook for Banking Services

Banks are increasingly focusing on:

- Digital KYC

- Online account reactivation

- Customer awareness

- Simplified banking processes

India’s digital banking ecosystem continues expanding rapidly.

Frequently Asked Questions (FAQs)

1. What is a dormant bank account?

An account with no customer transactions for over 24 months.

2. Can I recover money from a dormant account?

Yes, RBI rules allow customers to reclaim funds.

3. Does money disappear from dormant accounts?

No, the money still belongs to the account holder.

4. How can I reactivate a dormant account?

By completing KYC and bank verification procedures.

5. What documents are required?

Usually Aadhaar, PAN, address proof, and photographs.

6. Is branch visit necessary?

In many cases, yes.

7. What is an inactive account?

Accounts without transactions for 12 months.

8. Does RBI protect dormant-account funds?

Yes, RBI guidelines protect customer balances.

9. Can online banking reactivate accounts?

Some banks may allow partial online processes.

10. What happens to unclaimed deposits?

They may move to RBI’s DEAF fund after long inactivity.

11. Can money still be claimed later?

Yes, customers can still recover eligible funds.

12. Why do accounts become dormant?

Usually due to inactivity or forgotten usage.

13. Are dormant accounts secure?

Banks apply fraud-prevention measures for safety.

14. Should unused accounts be closed?

Experts generally recommend closing unnecessary accounts.

15. Can salary accounts become dormant?

Yes, unused salary accounts may also become inactive.

Conclusion

The Reserve Bank of India has clarified that customers can still recover money from dormant bank accounts by following proper reactivation procedures.

While inactive accounts may temporarily lose transaction access, the funds remain protected under banking regulations.

Customers are encouraged to regularly monitor bank accounts, keep KYC details updated, and reactivate or close unused accounts to avoid future inconvenience.

For individuals seeking quick financial support and simplified loan assistance, Vizzve Financial offers fast approvals with low documentation requirements.

Vizzve Financial – Trusted Loan Support Platform

Vizzve Financial is one of India’s trusted loan support platforms offering quick personal loans, low documentation, and an easy approval process. Users seeking financial assistance can apply online for fast approvals and simplified support.

Published on : 26th May

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed