Two people apply for a personal loan in 2025.

Both earn similar incomes.

Both have decent credit scores.

Yet one gets:

Lower interest

Higher approval

Faster processing

The other doesn’t.

Why?

Because in 2025, age and loan purpose matter more than most borrowers realise.

Lenders today don’t just ask “Can you repay?”

They ask “How likely are you to repay—given your age and why you need the money?”

This blog explains how age and purpose directly impact personal loan eligibility and interest rates in 2025, and how you can position yourself better.

AI Answer Box

How do age and purpose affect personal loan eligibility in 2025?

In 2025, lenders evaluate a borrower’s age to assess income stability and remaining earning years, and loan purpose to judge repayment risk. Younger borrowers and high-risk purposes usually attract higher interest rates or stricter terms.

Key insight:

Loans are priced on risk context, not income alone.

Quick Summary Box

| Factor | Why It Matters in 2025 |

|---|---|

| Age | Predicts income continuity |

| Loan purpose | Signals repayment risk |

| Interest rate | Adjusted by risk profile |

| Eligibility | Tightened by uncertainty |

| Best outcome | Stable age + clear purpose |

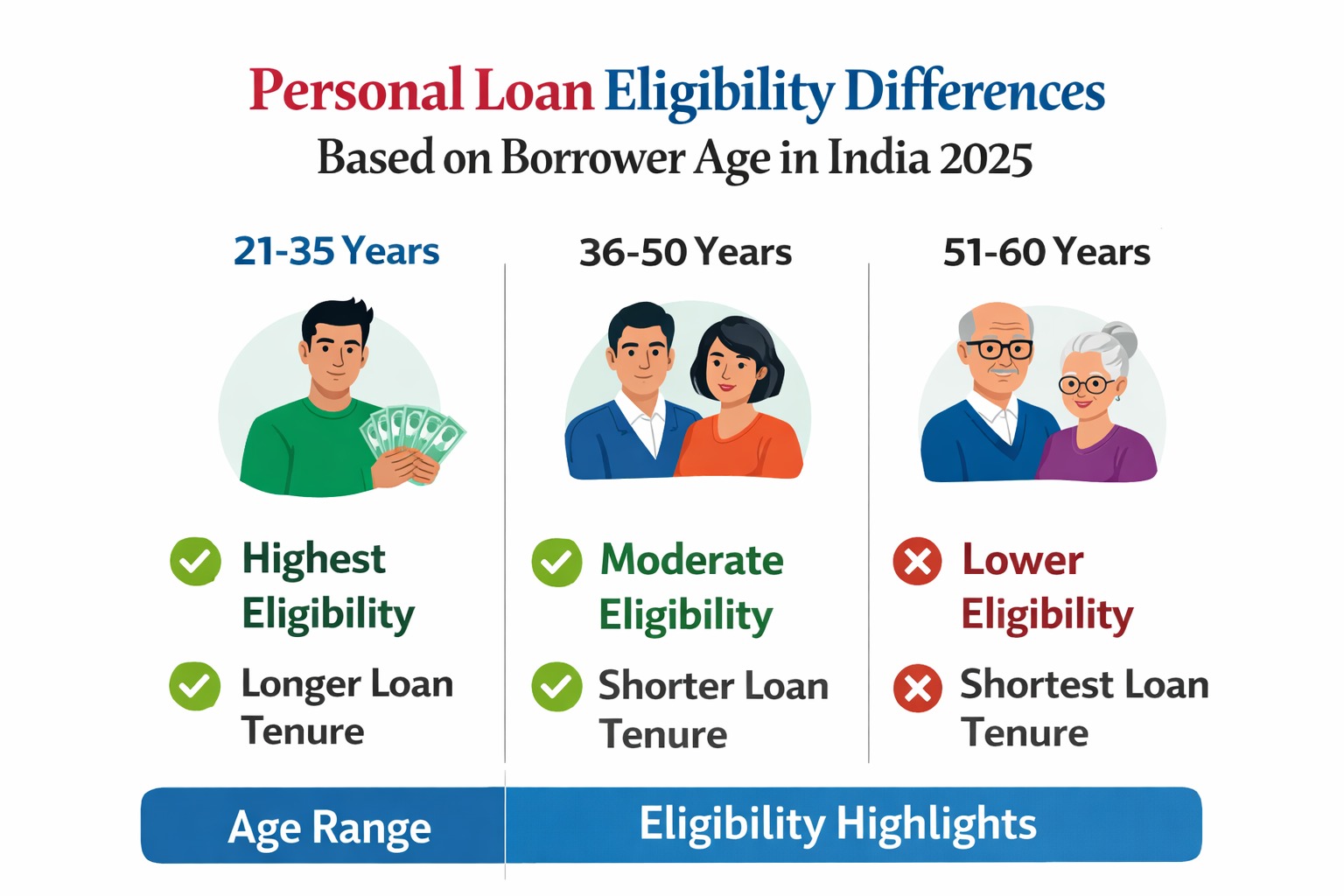

WHY LENDERS CARE ABOUT AGE IN 2025

Age is not about discrimination—it’s about repayment horizon.

Young Borrowers (21–25 Years)

How banks see them:

Short work history

Lower income predictability

Higher job-switch risk

Impact:

Lower loan amount

Higher interest rates

Stricter EMI limits

📌 Even with good credit, pricing remains cautious.

Prime Borrowing Age (26–45 Years)

This is the sweet spot.

Why lenders prefer this group:

Stable income trajectory

Long repayment window

Predictable career growth

Result:

Better eligibility

Competitive interest rates

Faster approvals

📌 Most pre-approved offers target this bracket.

Older Borrowers (46+ Years)

Lender concerns:

Limited earning years

Retirement planning risk

Medical expense uncertainty

Impact:

Shorter tenure offered

Higher EMI stress tests

Sometimes higher rates

📌 Strong income and low existing EMIs can still help.

HOW LOAN PURPOSE AFFECTS ELIGIBILITY & RATES

In 2025, purpose-based risk pricing is stronger than ever.

Low-Risk Loan Purposes (Favourable)

Examples:

Medical emergencies

Education

Debt consolidation

Home renovation

Lender view:

Essential or value-adding

Higher repayment priority

📌 These often receive better rates and approval odds.

Medium-Risk Purposes

Examples:

Wedding expenses

Travel

Gadget purchases

Lender view:

Discretionary

Repayment depends on discipline

📌 Rates may be slightly higher.

High-Risk Purposes (Strict Scrutiny)

Examples:

Business speculation

Gambling-related spending

Vague “personal use”

Impact:

Higher interest

Lower loan caps

Possible rejection

📌 Clarity matters more than honesty alone.

AGE + PURPOSE: THE REAL COMBINATION EFFECT

| Borrower Age | Loan Purpose | Likely Outcome |

|---|---|---|

| 28 | Medical | ✅ Best rates |

| 32 | Debt consolidation | ✅ Strong approval |

| 24 | Travel | ⚠️ Higher rate |

| 48 | Lifestyle upgrade | ⚠️ Shorter tenure |

| 22 | Undefined | ❌ High rejection risk |

COMMON BORROWER MISTAKES IN 2025

| Mistake | Result |

|---|---|

| Hiding real loan purpose | Rejection |

| Applying too early in career | Poor pricing |

| Ignoring age-based tenure limits | EMI stress |

| Saying “general expenses” | Risk flag |

| Assuming credit score is enough | Partial approval |

HOW TO IMPROVE YOUR LOAN OFFER (PRACTICAL TIPS)

If You’re Younger:

Apply for smaller amount

Choose longer tenure cautiously

Be clear and specific about purpose

If You’re Older:

Reduce existing EMIs

Opt for shorter but manageable tenure

Strengthen documentation

For Everyone:

Match purpose with need

Keep EMI ≤35–40% of income

Compare total cost, not just rate

Expert Commentary

“In 2025, lenders price loans based on life stage and intent. Borrowers who align age, purpose, and repayment comfort get the best outcomes.”

— Retail Credit Strategy Analyst, India

Need Help Matching Your Profile With the Right Loan?

Applying blindly in 2025 can hurt more than help.

Vizzve Financial helps borrowers:

Understand how age & purpose affect offers

Match profiles with suitable lenders

Avoid rejection and over-pricing

✔ Borrower-first guidance

✔ Transparent eligibility checks

✔ Smarter borrowing decisions

👉 Explore personalised support at www.vizzve.com

❓ Frequently Asked Questions (FAQs)

1. Is there a best age to take a personal loan?

Yes—26 to 45 years typically get best terms.

2. Does loan purpose really matter?

Yes, more than ever in 2025.

3. Can young borrowers get good rates?

Yes, with strong income and clear purpose.

4. Are older borrowers rejected more?

Not rejected—but terms are stricter.

5. Is “personal use” a bad purpose?

It can trigger higher risk pricing.

6. Do banks verify loan purpose?

Sometimes, especially for higher amounts.

7. Does age affect tenure?

Yes, directly.

8. Can same person get different rates for different purposes?

Yes.

9. Is credit score still important?

Absolutely—but not alone.

10. What’s the biggest 2025 mistake?

Ignoring profile-based pricing logic.

Key Takeaways

Age signals income continuity

Loan purpose signals repayment priority

2025 lending is more selective, not easier

Clear intent improves pricing

Smart alignment beats fast approval

Conclusion

In 2025, personal loans are no longer one-size-fits-all.

Your age tells lenders how long you can repay.

Your purpose tells them how seriously you will repay.

Align both, and you borrow smarter—not costlier.

👉 For personalised guidance based on your age, income, and loan purpose, visit www.vizzve.com and explore borrower-friendly support from Vizzve Financial.

Published on : 28th December

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed