Introduction

Most money problems don’t come from earning too little—they come from confusing saving, investing, and spending.

Each plays a different role in personal finance. When used correctly, they work together. When mixed up, they cause stress, debt, and stalled wealth.

This blog clearly explains the difference between saving, investing, and spending, with simple examples and practical guidance for 2026.

AI Answer Box

Short Answer:

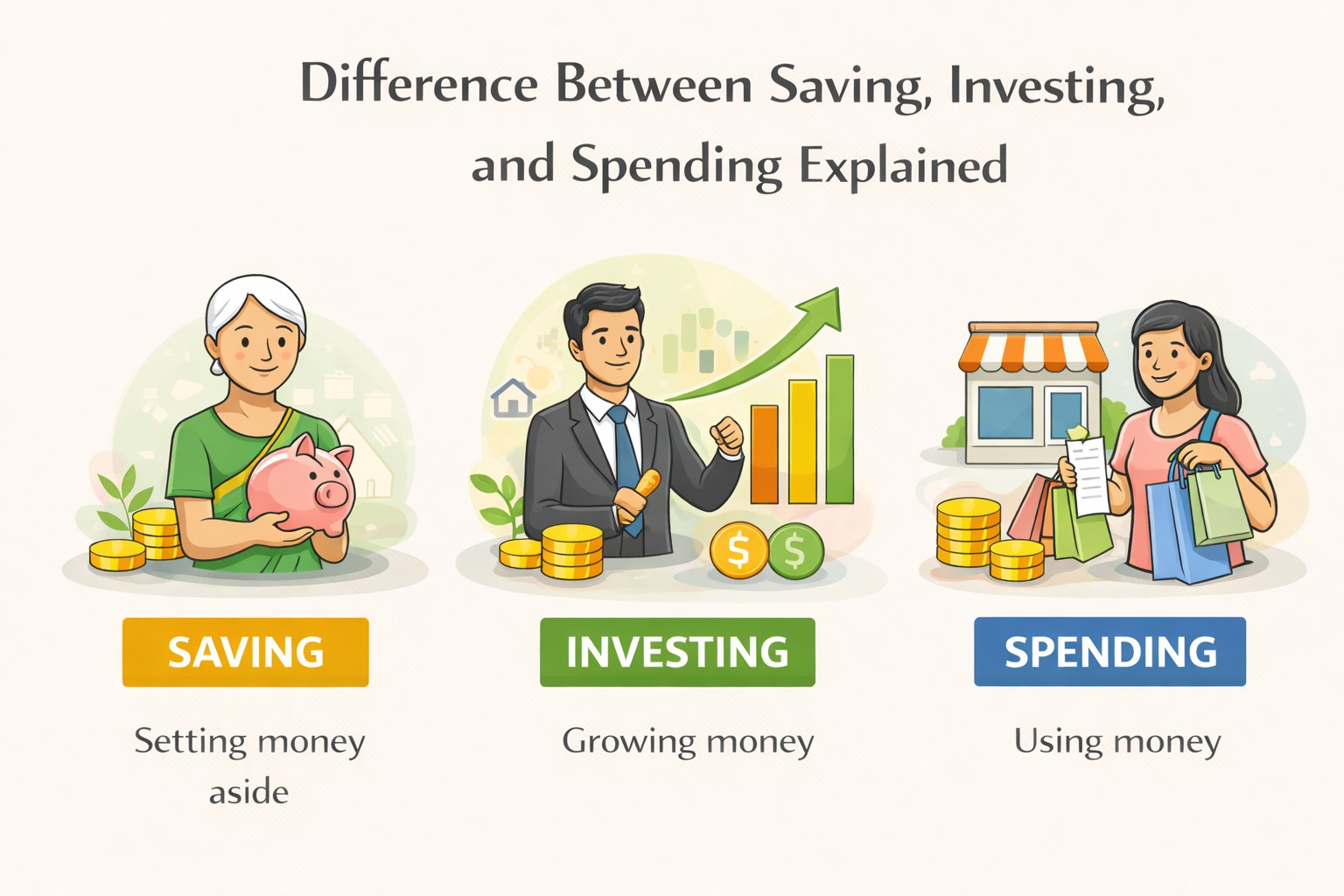

Saving is setting aside money safely for short-term needs, investing is growing money for long-term goals, and spending is using money for current consumption. Financial stability requires balancing all three.

What Is Spending?

Spending is using money to meet current needs or wants.

Common Spending Examples

Rent and groceries

Utilities and transport

Education and healthcare

Lifestyle expenses

Key Characteristics

Immediate benefit

Does not grow money

Necessary but unlimited spending creates stress

📌 Spending keeps life running—but doesn’t build the future.

What Is Saving?

Saving means setting aside money safely for near-term needs.

Where People Save

Savings accounts

Fixed deposits

Emergency funds

Purpose of Saving

Emergencies

Short-term goals

Financial safety

Key Characteristics

Low risk

High liquidity

Limited growth

📌 Saving protects you. It doesn’t make you wealthy.

What Is Investing?

Investing is putting money into assets that grow over time.

Common Investment Options

Equity and mutual funds

Bonds

Real estate

Retirement funds

Purpose of Investing

Beat inflation

Build wealth

Achieve long-term goals

Key Characteristics

Higher risk than saving

Long-term focus

Power of compounding

📌 Investing builds the future you don’t want to work forever for.

Saving vs Investing vs Spending: Side-by-Side

| Aspect | Spending | Saving | Investing |

|---|---|---|---|

| Time Horizon | Immediate | Short-term | Long-term |

| Risk | None | Very Low | Medium–High |

| Growth | None | Minimal | High (over time) |

| Liquidity | High | High | Medium |

| Purpose | Living | Safety | Wealth creation |

Why Confusing These Three Causes Financial Stress

Common mistakes include:

Treating savings as investments

Investing emergency funds

Spending future money today

Avoiding investing due to fear

📌 Each rupee needs a job.

The Right Order: A Simple Money Hierarchy

Personal Finance Pyramid

Spending – Cover essentials

Saving – Build emergency buffer

Investing – Grow long-term wealth

Skipping steps causes instability.

How Banks and Planners View These Differently

Banks (under guidance of the Reserve Bank of India) assess:

Spending → EMI burden

Saving → Financial cushion

Investing → Long-term resilience

📌 Healthy borrowers balance all three.

Real-Life Example

| Person | Behaviour | Outcome |

|---|---|---|

| A | High spending, no saving | Stress |

| B | High saving, no investing | Safe but stagnant |

| C | Balanced approach | Stable + wealthy |

How Much Should Go Where? (Rule of Thumb)

A simple starting split:

50–60% Spending

20–30% Saving + Investing

10–20% Long-term investing

📌 Adjust based on income and life stage.

Common Myths

| Myth | Reality |

|---|---|

| Saving is investing | No growth vs growth |

| Investing is gambling | Discipline reduces risk |

| Spending less solves everything | Balance matters |

| High income fixes mistakes | Behaviour matters more |

Expert Insight

“Saving protects your present. Investing protects your future. Spending should respect both.”

From real financial planning experience, people who clearly separate these buckets make fewer money mistakes—even with average income.

Key Takeaways

Spending = survival & lifestyle

Saving = safety & stability

Investing = growth & freedom

All three are necessary

Balance creates financial peace

Frequently Asked Questions

1. Is saving better than investing?

For safety, yes. For growth, no.

2. Should beginners invest or save first?

Save emergency fund first.

3. Can investing replace saving?

No, they serve different roles.

4. Is spending always bad?

No, controlled spending is essential.

5. How much should I save monthly?

At least 20% if possible.

6. Is investing risky?

Short-term yes, long-term manageable.

7. Can I invest without high income?

Yes, discipline matters more.

8. Should I invest emergency money?

Never.

9. Does inflation affect savings?

Yes, it reduces value over time.

10. What’s the biggest mistake people make?

Mixing saving and investing goals.

11. Is budgeting necessary?

Yes, to balance all three.

12. When should investing start?

As early as possible.

Conclusion: Give Every Rupee a Role

Saving, investing, and spending aren’t competing choices—they’re complementary tools.

When each rupee knows its role, money stops being stressful and starts working for you, not against you.

Published on : 24th January

Published by : SMITA

www.vizzve.com || www.vizzveservices.com

Follow us on social media: Facebook || Linkedin || Instagram

🛡 Powered by Vizzve Financial

RBI-Registered Loan Partner | 10 Lakh+ Customers | ₹600 Cr+ Disbursed